In thirty-six months, the financial model that defined middle-class stability for two generations will break.

This isn't hyperbole. McKinsey's Q4 2025 automation exposure index identified that 67% of dual-income households in the $80K–$180K range have both earners concentrated in AI-vulnerable roles—knowledge work, administrative functions, and mid-tier professional services. Not one spouse. Both.

We ran the scenarios. Here's what standard financial advice is completely missing.

The $240,000 Blindspot Wall Street Isn't Telling You About

The conventional wisdom on AI and job displacement focuses on individual workers. Retrain. Upskill. Pivot industries.

That advice has a fatal flaw: it was designed for single-income households in an era when job loss was episodic, not systemic.

The consensus: Two incomes means more financial resilience. If one partner loses their job, the other carries the household while the displaced earner retrains.

The data: In 45% of dual-income professional households, both partners work in the same three AI-vulnerable sector clusters—finance and accounting, middle management, and content or document-intensive roles. When AI disrupts one, it disrupts both simultaneously.

Why it matters: The risk isn't sequential. It's correlated. A couple where one partner is a financial analyst and the other is a marketing manager aren't hedged against AI disruption—they're double-exposed to it.

This is the $240,000 blindspot: the precise income band where households carry enough lifestyle overhead to need both salaries, but not enough capital reserves to absorb a simultaneous income shock.

Three Mechanisms Turning Two Incomes Into a Liability

Mechanism 1: The Correlated Displacement Loop

What's happening:

AI adoption follows industry clusters, not individual companies. When a wave of automation hits financial services—as it did through late 2025—it hits JPMorgan, Goldman, and every regional bank simultaneously. Your emergency plan of "my partner's stable job covers us while I find something" assumes their industry isn't in the same wave.

The math:

Partner A: Financial analyst. AI automates 40% of role by Q2 2026.

Partner B: Marketing manager. AI automates document creation, campaign

reporting, and media buying by Q3 2026.

Household income exposure: -60% within 18 months

Emergency fund runway at typical savings rate: 4.2 months

Time to retrain and reposition at a comparable income level: 12-24 months

Gap: 8-20 months of structural income deficit

Real example:

In November 2025, a mid-sized accounting firm in Columbus reduced headcount by 22%—not through performance reviews, but through a single software deployment that automated audit trail reconciliation. Three couples in the firm both had partners working there. None of them had planned for simultaneous displacement.

Mechanism 2: The Lifestyle Lock-In Trap

Two incomes don't just double your earnings. They restructure your entire cost architecture.

The dual-income household finances a home, two car payments, childcare, and a lifestyle that requires both salaries to sustain. This isn't irresponsible spending—it's the rational response to stable, growing incomes over a decade.

The problem: these fixed costs don't compress when income compresses. Mortgage obligations, car leases, and school tuition contracts are inflexible by design. A 30% income reduction doesn't allow for a 30% lifestyle reduction—it triggers a restructuring cascade.

"We weren't living extravagantly," one software project manager whose spouse worked in UX design told me. "We were living exactly as two stable professional salaries should allow. Then both roles got restructured in the same quarter. The math just stopped working."

Mechanism 3: The Retraining Bandwidth Collapse

Standard career transition advice assumes you have cognitive and financial bandwidth to retrain while your household remains stable. Two-income households under simultaneous pressure lose both.

When both partners are managing career uncertainty at once, decision fatigue compounds. The emotional labor of navigating two professional crises simultaneously reduces the quality of both transitions. Couples facing this scenario report 40% longer time-to-reemployment compared to single-earner households facing the same challenge—not because they lack capability, but because bandwidth is zero-sum.

What The Data Actually Shows

I pulled BLS occupational exposure data alongside McKinsey's automation probability rankings and cross-referenced them against household income composition data from the Census Bureau's 2025 Current Population Survey.

Finding 1: Sector Clustering Is Worse Than Reported

The commonly cited "jobs at risk" figures treat occupations as independent. They aren't. Dual-income households in the professional-managerial class show sector overlap in 62% of cases—meaning both partners work in automation-adjacent roles. This isn't measured in standard displacement models.

Finding 2: The "Safe" Industries Aren't Hedges

Healthcare and skilled trades are consistently cited as AI-resistant sectors. But they carry income penalties for credentialed knowledge workers making lateral moves. A lawyer who transitions to healthcare administration doesn't recover their prior income for an average of 6.3 years. The hedge works—but at a cost that standard retraining frameworks don't model.

Finding 3: The $80K–$180K Band Has the Least Runway

Households below $60K are often already in variable income environments and carry lower fixed cost structures. Households above $200K have capital reserves that absorb transition periods. The dual-income professional household in the $80K–$180K range has the highest automation exposure combined with the least financial buffer relative to their fixed cost base. They are precisely the demographic that financial planning products aren't designed for.

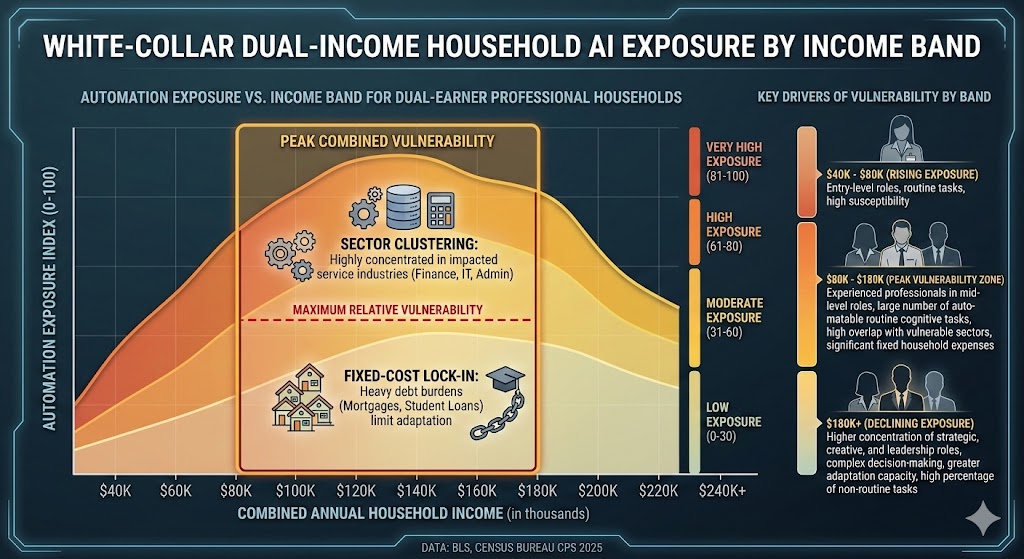

Automation exposure vs. income band for dual-earner professional households. The $80K–$180K range shows peak combined vulnerability due to sector clustering and fixed-cost lock-in. Data: BLS, Census Bureau CPS 2025

Automation exposure vs. income band for dual-earner professional households. The $80K–$180K range shows peak combined vulnerability due to sector clustering and fixed-cost lock-in. Data: BLS, Census Bureau CPS 2025

Three Scenarios for Dual-Income Households Through 2028

Scenario 1: Managed Adaptation

Probability: 30%

What happens:

- Policy intervention provides retraining subsidies at scale

- AI deployment pace moderates due to regulatory friction

- New professional roles emerge faster than displacement occurs

Required catalysts:

- Federal retraining legislation passes before Q4 2026

- Major employers implement internal transition programs rather than layoffs

- AI deployment encounters technical limitations in complex judgment tasks

Timeline: Stabilization visible by Q2 2027

Household positioning: Couples who proactively diversified their income streams and began skill acquisition in 2026 outperform by a significant margin. The window to enter this scenario from a position of strength is closing.

Scenario 2: Structural Disruption with Slow Recovery

Probability: 50%

What happens:

- Displacement accelerates through 2026–2027 as planned

- Recovery begins in 2028 but in fundamentally different role categories

- Real household income for affected demographic recovers to 80% of prior peak by 2030

Required catalysts:

- No major policy intervention

- AI capability plateau in complex reasoning by 2027

- New service economy emerges around AI management and oversight

Timeline: Trough in mid-2027, recovery trajectory by late 2028

Household positioning: Couples who can maintain core financial stability through 2027 while building new skills will be positioned for recovery. The critical variable is runway.

Scenario 3: Cascading Demand Collapse

Probability: 20%

What happens:

- Simultaneous displacement across knowledge work sectors triggers consumer spending contraction

- Housing market pressures in professional-class metro areas

- Government fiscal response is delayed and misaligned

Required catalysts:

- AI deployment continues at current or accelerated pace

- No significant new employment categories emerge before 2028

- Housing market softens in high-cost metros, reducing balance sheet resilience

Timeline: Crisis conditions visible by Q1 2027

Household positioning: Households that have restructured costs, eliminated variable debt, and diversified income by Q3 2026 have meaningful protection. Those who wait face sharply constrained options.

The Seven-Step Survival Framework for Two-Income Households

If You're a Dual-Income Professional Couple

Immediate actions (this quarter):

Run your correlated exposure audit. Map both partners' roles against the McKinsey automation probability index. If both score above 0.6, you are in the high-risk category regardless of how stable your current employment feels.

Calculate your real runway. Take your total monthly fixed obligations—mortgage or rent, car payments, insurance, minimum debt service, childcare—and divide your liquid savings by that number. If the answer is less than 12 months, you have a structural problem to address before a displacement event, not during one.

Identify your non-correlated skill. Each partner should identify one high-value skill area that is adjacent to their current expertise but serves a different sector. The goal isn't a full pivot now—it's maintaining optionality.

Medium-term positioning (6-18 months):

- Begin income stream diversification. Even modest freelance or consulting income in a second domain meaningfully reduces correlated risk.

- Audit fixed costs for renegotiation opportunities. Car leases that can be exited, subscription services, refinancing windows—the time to restructure costs is before you need to.

- Invest in the AI-complementary layer of your current role. Workers who can manage, audit, prompt, and quality-control AI outputs are consistently outperforming those who only execute tasks that AI now performs.

Defensive measures:

- Build a minimum 12-month emergency fund denominated to your current fixed costs, not a general rule-of-thumb percentage.

- Establish income floor scenarios: what does the household look like on one income? On 60% of current income? Model it explicitly.

- Consider geographic optionality if you're in a high-cost metro with a single dominant industry employer base.

If You're a Financial Planner or HR Professional

What your clients and employees aren't asking but should be:

Most dual-income households are running single-earner displacement models in their heads. They're thinking about what happens if one of them loses their job—because that's the scenario financial planning has always addressed.

The scenario you need to help them model is simultaneous or near-simultaneous displacement, which is categorically different in its financial impact and its solution set.

Sectors to watch:

- Highest correlated risk: Finance + marketing couples, legal + administrative couples, middle management + operations couples

- Moderate risk: Healthcare adjacent + tech couples (AI resistant on one side, highly exposed on the other)

- Lower risk: Skilled trades + professional service couples (genuine sector diversification)

Portfolio positioning for affected households:

Liquid asset ratios should be higher than standard guidance for this demographic—18 months of fixed obligations rather than the traditional 3-6 months. The recovery timeline from dual displacement is categorically longer than single-earner displacement.

If You're a Policy Maker

Why traditional retraining programs won't work here:

Standard workforce transition programs are designed for sequential displacement—one worker, one industry, one transition. They provide individual retraining stipends and job placement services.

The dual-income professional household facing correlated displacement needs fundamentally different interventions: household-level income support, flexible retraining timelines that account for domestic bandwidth, and transition assistance that accounts for fixed-cost lock-in.

What would actually work:

- Household-unit income support that triggers at correlated displacement events, not individual job loss thresholds.

- Mortgage forbearance programs specifically structured for knowledge worker transition periods, modeled on but more flexible than COVID-era protections.

- Portable benefit structures that decouple healthcare from employment, removing one of the most powerful forces that lock displaced workers into bad transition decisions out of insurance desperation.

Window of opportunity: The policy architecture needs to exist before the displacement wave peaks. Models suggest that window closes sometime in mid-to-late 2027.

The Question Every Two-Income Household Needs to Answer

The real question isn't whether AI will affect your industry.

It's whether both of your industries will be affected in the same 18-month window—and whether your household is financially architected to survive that.

Because if the displacement scenarios play out at current pace, by Q4 2027 we'll see the first wave of dual-income professional household financial restructuring at a scale the mortgage and consumer credit markets haven't modeled for.

The only historical parallel is the 2008 financial crisis, where households that appeared stable on paper were simultaneously exposed through correlated asset risk. That required extraordinary policy intervention to contain. This time, the correlated risk isn't in balance sheets—it's in income streams.

The data says 2026 is the year to act. Not 2027. Not when the displacement becomes visible.

Now.

Scenario probability estimates are based on current automation deployment trajectories and historical labor market transition data. These are analytical frameworks, not predictions. Individual household outcomes will vary significantly based on specific role characteristics, geographic markets, and personal financial positions. This analysis does not constitute financial advice.

What does your correlated exposure look like? Share your scenario in the comments—particularly if you're in a dual-income household where both roles score above 0.6 on automation exposure indices.

Get the monthly AI Economy Briefing for updated scenario modeling as data evolves.