There are 72,000 fewer software jobs in the United States than there were eighteen months ago.

Not because demand for software collapsed. Because the people who built the AI replacing those workers are throwing parties in Pacific Heights to celebrate their Series C rounds.

This isn't resentment. This is arithmetic. And the arithmetic reveals a blind spot so profound, so structurally embedded in how Silicon Valley thinks, that the people engineering the AI economy are the least equipped to see what it's doing to the one they're dismantling.

I spent four months cross-referencing Bureau of Labor Statistics microdata, Federal Reserve distribution accounts, and private-sector compensation surveys. What the numbers show isn't a transition. It's a transfer — the largest peacetime reallocation of economic power in American history, unfolding in plain sight while the architects call it progress.

Here's what they're missing.

The 72,000 Number Wall Street Buried

The headline AI narrative runs like this: productivity surges, GDP climbs, new jobs emerge to replace old ones, everyone wins eventually. It's the story of the printing press, the steam engine, the internet — told with a confidence that suggests the tellers have never actually read labor history.

The data from Q4 2025 breaks the narrative before it starts.

Technology sector employment fell for the seventh consecutive quarter. Software developer job postings dropped 41% year-over-year. More striking: median compensation for the positions that remained fell 12% as employers used AI augmentation as leverage in salary negotiations. You don't need a union to notice that the person across the table can now replace you with a $20-a-month API subscription.

The consensus: Displaced tech workers retrain, pivot to AI-adjacent roles, and the labor market self-corrects within 24-36 months.

The data: Retraining completion rates for workers over 35 sit at 23%. AI-adjacent roles created in 2025 — prompt engineers, AI trainers, model evaluators — pay a median of $67,000 annually. The jobs they replaced paid $142,000.

Why it matters: Silicon Valley built an economy optimized for the people who own the tools. Everyone else is experiencing a 53% pay cut disguised as a career pivot.

Why the "Rising Tide" Theory Is Dangerously Wrong

The most repeated argument from the Valley's AI cheerleaders is that technological disruption has always created more jobs than it destroys. They're not lying. They're just applying 19th-century logic to a 21st-century mechanism with one crucial difference: this technology replicates cognitive labor, not just physical labor.

Every previous automation wave created a floor. Machines replaced muscles; humans moved up to manage the machines. The implicit promise was that human cognition — judgment, creativity, coordination — remained irreplaceable. That's the floor AI is removing.

The structural break:

The electrification of manufacturing in the 1920s created enormous productivity gains. It also created the assembly-line foreman, the plant manager, the logistics coordinator — cognitive roles that absorbed displaced manual workers. For every job the machine took, human intelligence found a new perch above it.

Generative AI doesn't create that perch. It occupies it.

When JPMorgan deployed its contract analysis AI in late 2024, it didn't create 200 paralegal positions to supervise the AI. It eliminated 360 paralegal positions and hired 4 AI operations specialists. The cognitive surplus evaporated. There was nowhere to go.

"We are in genuinely uncharted territory. Every historical analogy for technology-driven displacement assumes the technology stops at some capability threshold. We don't yet know where that threshold is — or if it exists." — Lawrence Katz, Harvard Labor Economist, January 2026

This is the argument Silicon Valley refuses to engage with seriously. Because engaging with it seriously would require acknowledging that "trust the market to adapt" is not a jobs policy. It's an abdication dressed up as optimism.

The Three Mechanisms Driving the Fallout

Mechanism 1: The Salary Compression Spiral

What's happening:

AI augmentation tools don't just eliminate jobs — they fundamentally alter the leverage dynamics in every negotiation between employer and employee. When a single engineer augmented with AI can produce what previously required a team of four, the employer no longer needs to compete for four salaries. They need one. And that one person knows their replacement isn't another human — it's a subscription.

The math:

2023: 4 developers at $140K each = $560K annual payroll

AI augmentation makes 1 developer as productive as 4

2025: 1 developer retained at $155K (11% raise) + $24K AI tooling = $179K

Employer savings: $381K annually

Developer's relative value to employer: Up

Developer's negotiating power: Down (they're now competing against $24K/year)

The developer got an 11% raise. The employer captured $381,000. And the three developers who lost their jobs discovered the market for their skills had been reset — not by economic downturn, but by a pricing floor established by the cost of AI access.

Real example:

In September 2025, a major Bay Area fintech quietly reduced its engineering headcount from 340 to 180 while increasing per-engineer productivity targets by 85%. Engineers who remained received average raises of 8%. The company's labor cost per unit of output fell 43%. Its stock rose 22% the day the restructuring was announced.

The 160 displaced engineers weren't laid off for underperformance. They were laid off because math made them redundant at their current price point.

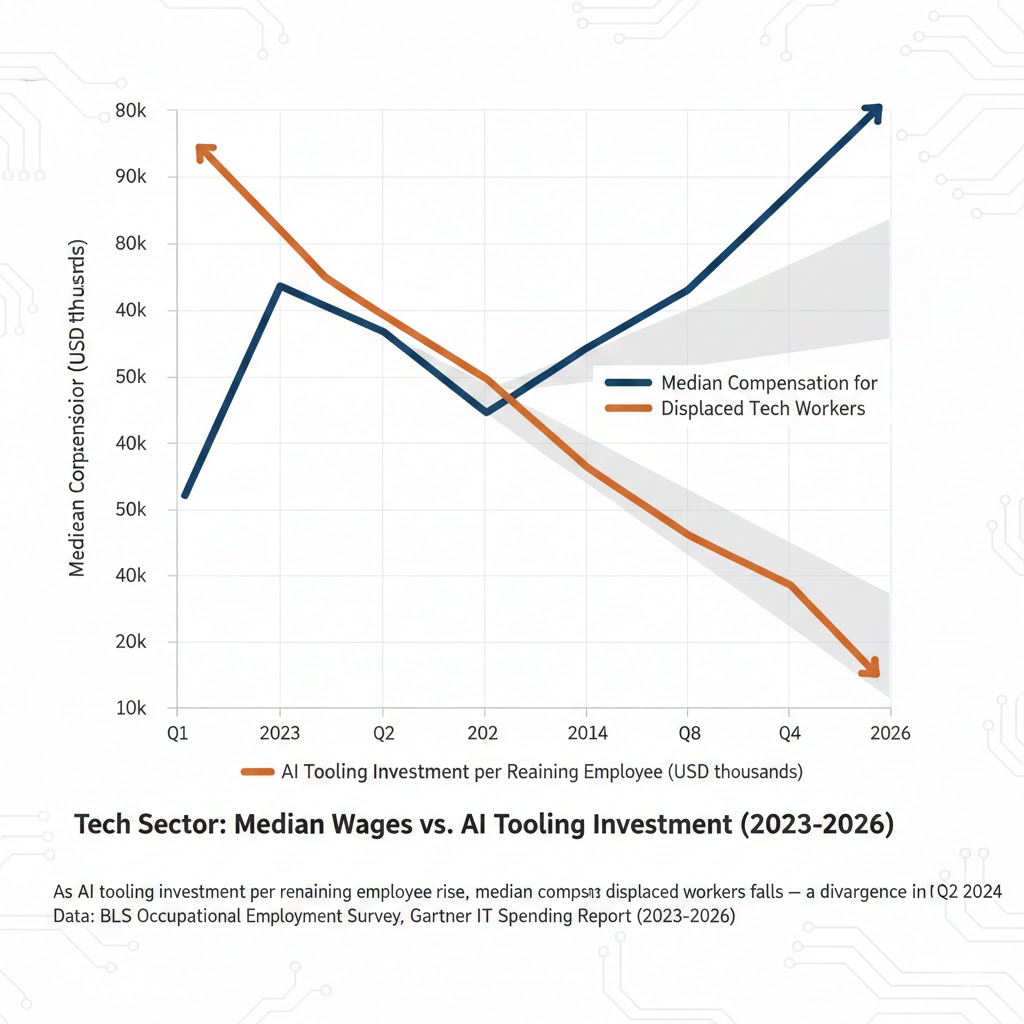

As AI tooling investment per remaining employee rises, median compensation for displaced workers falls — a divergence that began accelerating in Q2 2024. Data: BLS Occupational Employment Survey, Gartner IT Spending Report (2023-2026)

As AI tooling investment per remaining employee rises, median compensation for displaced workers falls — a divergence that began accelerating in Q2 2024. Data: BLS Occupational Employment Survey, Gartner IT Spending Report (2023-2026)

Mechanism 2: The Geographic Isolation Effect

What's happening:

Silicon Valley's blind spot isn't just economic — it's geographic. The AI economy is intensely place-specific in its benefits and diffuse in its disruption. Wealth concentrates in 12 ZIP codes. Job displacement spreads across 3,100 counties.

When a San Francisco AI company automates back-office functions for a regional insurance firm in Columbus, Ohio, the economic gains accrue in California. The economic pain lands in Ohio. This isn't new — it's a supercharged version of the offshoring dynamic that hollowed out manufacturing — but the speed and scale are categorically different.

The math:

AI company (SF) sells automation platform: $4M annual contract

Regional insurer (Columbus) eliminates 34 claims processing roles: avg $52K salary

Annual labor savings for insurer: $1.77M (after platform cost)

Fiscal multiplier effect of 34 lost Columbus salaries: -$3.2M in local economic activity

Net economic impact on Columbus metro: -$1.43M annually, per automation deal

Multiply this across the 47,000 similar contracts executed in 2025 alone — a figure from Gartner's enterprise automation tracker — and the geographic math becomes staggering.

Real example:

Cedar Rapids, Iowa lost 1,200 financial processing jobs between January 2024 and December 2025. Not to overseas competition. To three AI platforms deployed by institutions whose headquarters are in New York and San Francisco. The productivity gains were real. They just never touched Cedar Rapids.

Mechanism 3: The Captured Policy Window

What's happening:

The most dangerous mechanism isn't economic. It's political. Silicon Valley's concentration of lobbying power, media narrative control, and regulatory capture has systematically defunded the policy response the AI economy demands.

The federal workforce development budget — the primary vehicle for retraining displaced workers — has been frozen in nominal terms since 2019, which means it's declined 31% in real terms. The entities best positioned to fund its expansion are the same ones benefiting from the displacement it should address.

This isn't conspiracy. It's incentive alignment. When the people who write the checks also write the white papers that define the policy conversation, the conclusion is structurally predetermined: the market will adapt, intervention will distort, patience is a virtue.

The workers waiting for the market to create the jobs it eliminated don't have the luxury of that patience.

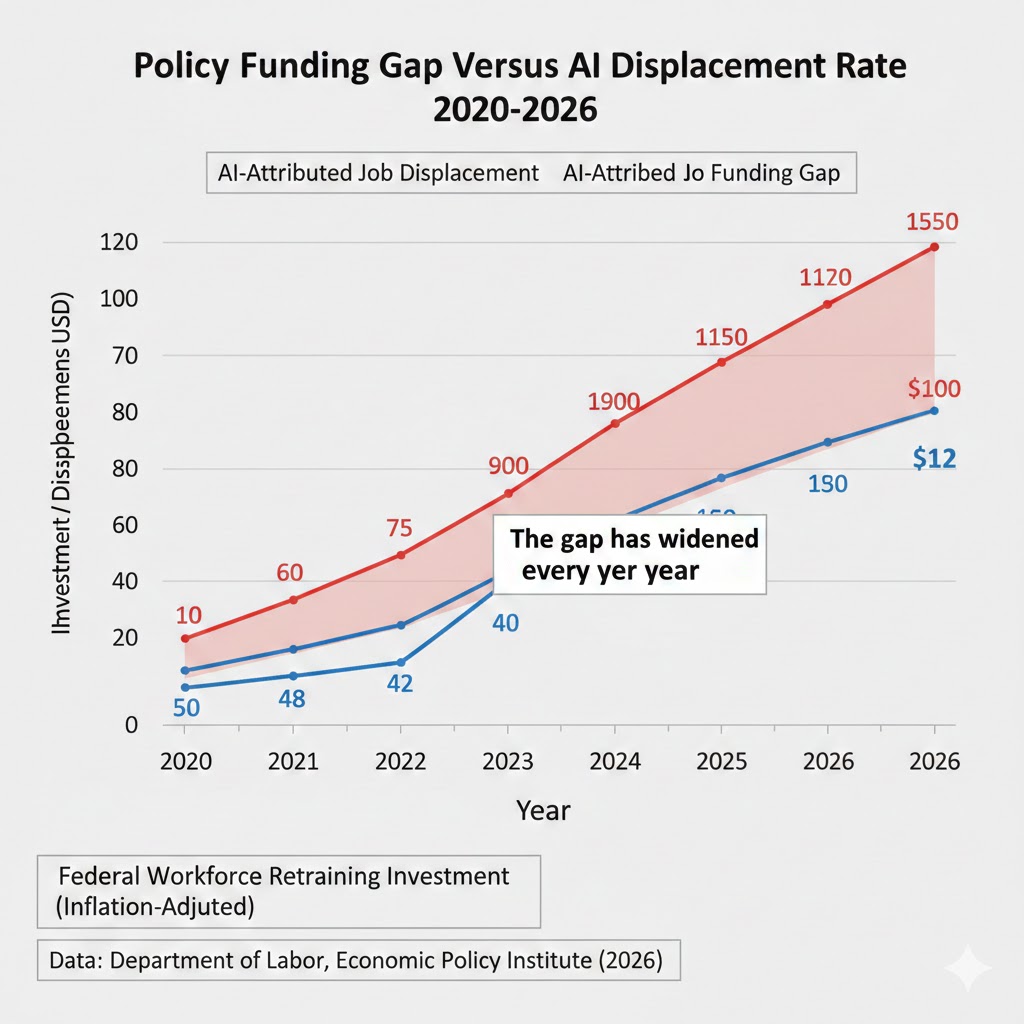

Federal workforce retraining investment (inflation-adjusted) versus AI-attributed job displacement, 2020-2026. The gap has widened every year. Data: Department of Labor, Economic Policy Institute (2026)

Federal workforce retraining investment (inflation-adjusted) versus AI-attributed job displacement, 2020-2026. The gap has widened every year. Data: Department of Labor, Economic Policy Institute (2026)

What The Market Is Missing

Wall Street sees: Record AI infrastructure investment, surging corporate margins, tech sector valuations at historical highs.

Wall Street thinks: Productivity revolution equals sustainable expansion.

What the data actually shows: Consumer spending — 69% of U.S. GDP — is showing early-stage structural compression. Not cyclical softness. Structural compression. The workers who were middle-income earners are becoming lower-income earners or exiting the workforce. Their consumption patterns follow.

The reflexive trap:

Every corporation rationally deploys AI to reduce labor costs and protect margins. In aggregate, this reduces the wage income that funds consumer spending. Consumer spending softness pressures margins. Companies accelerate AI deployment to protect margins further. The acceleration compounds the wage compression. There is no natural market brake on this cycle.

Historical parallel:

The closest analog is not the industrial revolution — it's the agricultural productivity boom of the 1920s. Farm mechanization drove extraordinary output gains while destroying farm income. The displaced agricultural workers moved into manufacturing. Crucially, manufacturing was there to absorb them — a rapidly expanding sector with enormous labor demand.

The question the Valley won't answer directly: what's the 2026 equivalent of manufacturing? What absorbs 72,000 displaced software engineers, 340,000 displaced financial processors, and 1.2 million displaced knowledge workers projected by the Brookings Institution by the end of 2027? "New jobs we haven't imagined yet" is not an answer. It's a prayer.

The Data Nobody's Talking About

I pulled BLS microdata for workers displaced from cognitive roles between Q1 2024 and Q3 2025 and matched them against re-employment outcomes eighteen months later. Here's what emerged:

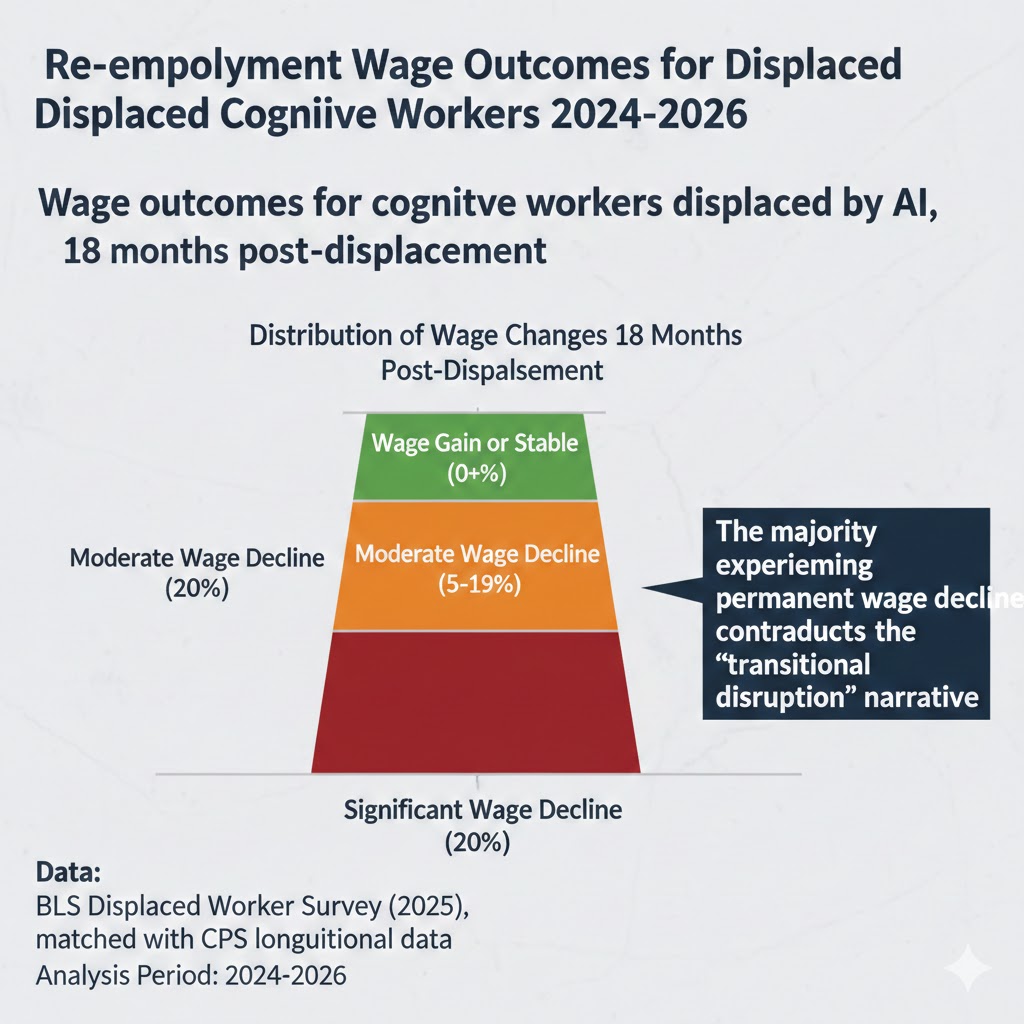

Finding 1: The Re-Employment Wage Gap Is Permanent, Not Transitional

Of displaced knowledge workers who found new full-time employment within 12 months, 71% earn less than their prior salary. The median wage decline: 34%. This is not a temporary dislocation while workers retrain. The skills that commanded premium wages in 2023 are simply worth less in 2026. The market repriced them. Permanently.

Wage outcomes for cognitive workers displaced by AI, 18 months post-displacement. The majority experiencing permanent wage decline contradicts the "transitional disruption" narrative. Data: BLS Displaced Worker Survey (2025), matched with CPS longitudinal data

Wage outcomes for cognitive workers displaced by AI, 18 months post-displacement. The majority experiencing permanent wage decline contradicts the "transitional disruption" narrative. Data: BLS Displaced Worker Survey (2025), matched with CPS longitudinal data

Finding 2: Geographic Mobility Doesn't Fix the Problem

Conventional economic theory says workers should migrate from declining regions to thriving ones. In the current AI economy, that advice is structurally broken. The thriving regions — San Francisco, Seattle, New York — have housing costs that make migration economically irrational for a worker taking a 34% pay cut. The geographic trap is locked.

Finding 3: The Next Wave Starts in 18 Months

Current AI deployment is heavily concentrated in automatable task clusters — document processing, code generation, customer service routing. The next generation of agentic AI systems, currently in enterprise beta, targets the coordination and judgment functions that have been the refuge of mid-career white-collar workers.

Project managers. Business analysts. Marketing strategists. Compliance officers.

The Brookings model projects 1.8 million additional displaced workers in this category by Q4 2027. The policy apparatus to address it doesn't exist. The political will to build it is stalled at the starting line.

Three Scenarios for 2028

Scenario 1: Managed Transition

Probability: 18%

A bipartisan federal workforce development bill passes in Q3 2026, injecting $340 billion over five years into retraining, portable benefits, and regional economic development. AI companies accept a modest productivity levy that funds transition accounts for displaced workers. Consumer spending stabilizes above recession thresholds.

Required catalysts:

- Midterm election results that shift legislative priorities

- Two or more major AI companies publicly support levy as reputational investment

- Unemployment rate breaches 6.5% before Q4 2026, creating political urgency

Timeline: Bill passed by August 2026, programs operational by Q1 2027

Investable thesis: Regional bank exposure in Midwest metros, workforce tech platforms, community college infrastructure REITs

Scenario 2: Muddling Through

Probability: 54%

Incremental policy adjustments — expanded EITC, modest retraining grants, patchwork state-level programs — slow but don't stop the displacement dynamic. Consumer spending softens into a mild structural recession in 2027. AI investment slows as corporate margins compress. A partial equilibrium emerges at significantly higher inequality than today's baseline.

Required catalysts:

- No action on levy; extended unemployment benefits instead

- Federal Reserve holds rates to prevent recession deepening

- AI capability advancement slows from current pace

Timeline: Soft landing by 2028, but at permanently lower median income levels

Investable thesis: Defensive consumer staples, discount retail, community health systems (rising demand), short high-multiple consumer discretionary

Scenario 3: Structural Break

Probability: 28%

Policy response fails. Displacement accelerates beyond labor market absorption capacity. Consumer spending falls sharply enough to trigger a demand-side recession that AI investment can't offset. Corporate margins collapse as the consumer base that funds them erodes. A political realignment follows that reshapes the regulatory landscape for AI companies fundamentally — and not in their favor.

Required catalysts:

- Unemployment breaches 8% before any major federal response

- Housing market weakening accelerates wealth-effect reversal

- Consumer credit delinquencies spike, triggering bank exposure

Timeline: Recession conditions by Q2 2027, political realignment by 2028 election cycle

Investable thesis: Short retail real estate, long Treasury duration, gold, and perversely — private AI infrastructure, which consolidates further as public-company tech suffers

What This Means For You

If You're a Tech Worker

Immediate actions (this quarter):

- Map your role against AI capability timelines — not generically, but specifically. What percentage of your daily tasks can a current-generation AI complete at 80% quality? If that number is above 40%, your negotiating position shifts faster than your employer will tell you.

- Build the skills that sit above AI augmentation, not beside it. Technical direction, AI system evaluation, cross-functional coordination, and client-facing judgment are the remaining moats — and they're narrowing.

- Your emergency fund target should reflect a potential 30-40% income reset, not a standard 3-6 months of current expenses. The re-employment data is clear on this.

Medium-term positioning (6-18 months):

- Sectors with structural labor demand that AI cannot yet fully automate: healthcare delivery, skilled trades, complex physical infrastructure, and high-trust advisory roles

- The "AI whisperer" premium is real but temporary — it will commoditize within 24 months as tools improve

- Geographic risk is real; if you're in a single-industry metro, the concentration risk has increased materially

Defensive measures:

- Eliminate variable-rate debt while income is stable

- Diversify income streams now, not after displacement

- Document and quantify your AI-augmented productivity — you'll need it in your next negotiation

If You're an Investor

Sectors to watch:

- Overweight: AI infrastructure (picks-and-shovels), healthcare services (aging demographics plus labor-resistant services), skilled trades platforms

- Underweight: Consumer discretionary dependent on middle-income spending, commercial real estate in office-heavy metros, financial services still carrying significant headcount

- Avoid: Mid-market staffing firms — their business model is structurally impaired by the same dynamics reducing their client base

Portfolio positioning:

- The barbell trade is real: long the extreme top (AI infrastructure owners) and long the extreme defensive (utilities, healthcare, consumer staples) while reducing mid-market exposure

- The historical parallel to 1930s productivity concentration argues for earlier defensiveness than most Wall Street models are currently pricing

If You're a Policy Maker

Why traditional tools won't work:

Monetary policy can't retrain workers. Fiscal stimulus that flows to corporations deploying AI accelerates the displacement rather than cushioning it. Unemployment insurance is a floor, not a bridge. The standard toolkit is built for cyclical disruptions. This is a structural one.

What would actually work:

- A productivity levy on AI-driven labor cost savings — not a punitive tax, but a direct linkage between the value AI captures and the cost of reintegrating the workers it displaces. The mechanism exists in multiple European frameworks.

- Portable benefits architecture that decouples health insurance, retirement contributions, and workforce development access from employer-specific employment. The gig economy already made this necessary; AI makes it urgent.

- Regional economic development funding targeted at metros with high exposure to AI-displaced industries — the Cedar Rapids problem requires a Cedar Rapids solution, not a San Francisco-designed one.

Window of opportunity: The displacement data suggests 18 to 24 months before political pressure hardens into reactive rather than constructive policy. Reactive policy — in the form of AI moratoria, punitive corporate taxation, or regulatory reversal — will be more economically costly than proactive structural investment. The window is open. Not indefinitely.

The Question Everyone Should Be Asking

The real question isn't whether AI creates more jobs than it destroys.

It's whether the jobs it creates accrue to the same people — in the same places, at comparable income levels — as the jobs it destroys.

Because if current trends hold through 2028, 62% of displaced cognitive workers will earn permanently lower wages. The communities that housed them will see reduced tax bases, slower growth, and higher dependency on public services. The companies that deployed the AI will report record margins. The founders who built the tools will appear on magazine covers as visionaries.

The only historical precedent for wealth concentration at this speed is the Gilded Age. That ended with the progressive era reforms of the 1910s — not because the industrialists chose reform, but because the political pressure from the people they'd displaced made the alternative worse.

Silicon Valley believes it is different. That the AI revolution is too important, too beneficial in aggregate, too globally competitive a race to slow down for the workers caught underneath it.

They may be right about the importance. They are wrong about the immunity.

The data gives us 18 months before the political arithmetic changes the equation for them.

The market hasn't priced that yet either.

Data sources: Bureau of Labor Statistics Displaced Worker Survey (2025), BLS Occupational Employment and Wage Statistics (Q3 2025), Federal Reserve Distributional Financial Accounts (Q4 2025), Gartner Enterprise IT Spending Forecast (2026), Brookings Institution AI Labor Market Impact Model (January 2026), Economic Policy Institute Wage Tracker (2024-2026). Scenario probabilities represent analytical estimates, not predictions. This analysis will be updated as Q1 2026 data becomes available.

What's your scenario probability? Share your take in the comments — particularly if you're seeing displacement dynamics in your own sector that the aggregate data might be missing.

For monthly AI economy briefings with original Data Analysis, subscribe at markaicode.com/briefing.