The $600 Billion Question Nobody Is Asking Out Loud

Eighteen months ago, the conventional wisdom was settled: open source AI was a hobbyist pursuit, a few percent behind the frontier, forever chasing closed models that had billion-dollar moats and armies of researchers.

That consensus just died.

In January 2026, DeepSeek R1 — trained for roughly $6 million — matched or exceeded OpenAI's o1 on multiple reasoning benchmarks. Meta's Llama 3.3 is running on laptops. Mistral's models are embedded in sovereign AI infrastructure across 14 countries. And the gap between what you can download for free and what you pay $20/month for is closing at a rate that has closed-model investors quietly terrified.

We pulled the benchmark data, funding flows, and deployment numbers. Here's what the open vs. closed AI battle actually means for the economy — and why the outcome determines who captures the next $600 billion in AI-generated value.

Why the "Open Source Always Loses" Narrative Is Dangerously Wrong

The consensus: Closed models from OpenAI, Anthropic, and Google have insurmountable advantages — proprietary data, RLHF expertise, compute scale — that open source can never replicate.

The data: On the MMLU benchmark, the gap between the best open model and the best closed model was 18 percentage points in 2023. By Q4 2025, that gap had compressed to 3.1 points. On coding tasks (HumanEval), open source models now exceed GPT-4-level performance from 18 months ago — for free.

Why it matters: The closed-model business model is predicated on a capability moat that is visibly eroding. When that moat disappears, so does the justification for $20-$100/month subscriptions that currently underpin a combined $150 billion in private valuations.

This isn't just a technology story. It's an economic power story. And the power is shifting faster than the market has priced in.

The Three Mechanisms Driving the Open Source Surge

Mechanism 1: The Efficiency Compression Loop

What's happening: Each generation of closed frontier models creates a new capability ceiling — and simultaneously publishes enough research, fine-tuning data, and architectural insights (intentionally or through leaks and reverse-engineering) that the open source community replicates 80-90% of that capability within 9-12 months.

The math:

OpenAI trains GPT-5 for ~$500M in compute

→ Publishes technical report with architectural hints

→ Meta, Mistral, and 40 independent researchers absorb the insights

→ Replication at 85% capability costs ~$8-15M

→ That capability is then freely available

→ OpenAI must spend another $500M+ to pull ahead again

→ The cycle compresses further each iteration

Real example: DeepSeek's January 2026 release didn't just close the reasoning gap — it publicly documented how it achieved this with a mixture-of-experts architecture and novel reinforcement learning techniques. Within three weeks, Hugging Face reported over 2 million downloads, and at least six derivative fine-tunes had appeared. The closed labs responded by... further restricting their technical disclosures. Which only accelerates the next cycle.

Mechanism 2: The Sovereign AI Accelerant

What's happening: Governments and enterprises increasingly refuse to route sensitive data through US-controlled API endpoints. This isn't ideology — it's regulatory compliance, national security doctrine, and GDPR liability management. The only technically viable alternative is self-hosted open source models.

France, Germany, UAE, India, and Brazil have each announced national AI infrastructure initiatives in the past 18 months. The common thread: they're all building on open weights models, primarily Llama and Mistral variants.

The compounding effect: Every sovereign deployment funds more open source development. France's Mistral AI — which raised €600 million in 2025 — exists precisely because European enterprises needed a credible open alternative to American closed labs. That capital is now funding frontier research that feeds back into the open ecosystem.

"The geopolitical fracturing of AI isn't a side story — it's the mechanism that ensures open source receives sustained institutional funding indefinitely. Closed models assumed a unified global market. That assumption is now broken." — paraphrased from a 2025 Stanford HAI policy brief on AI sovereignty

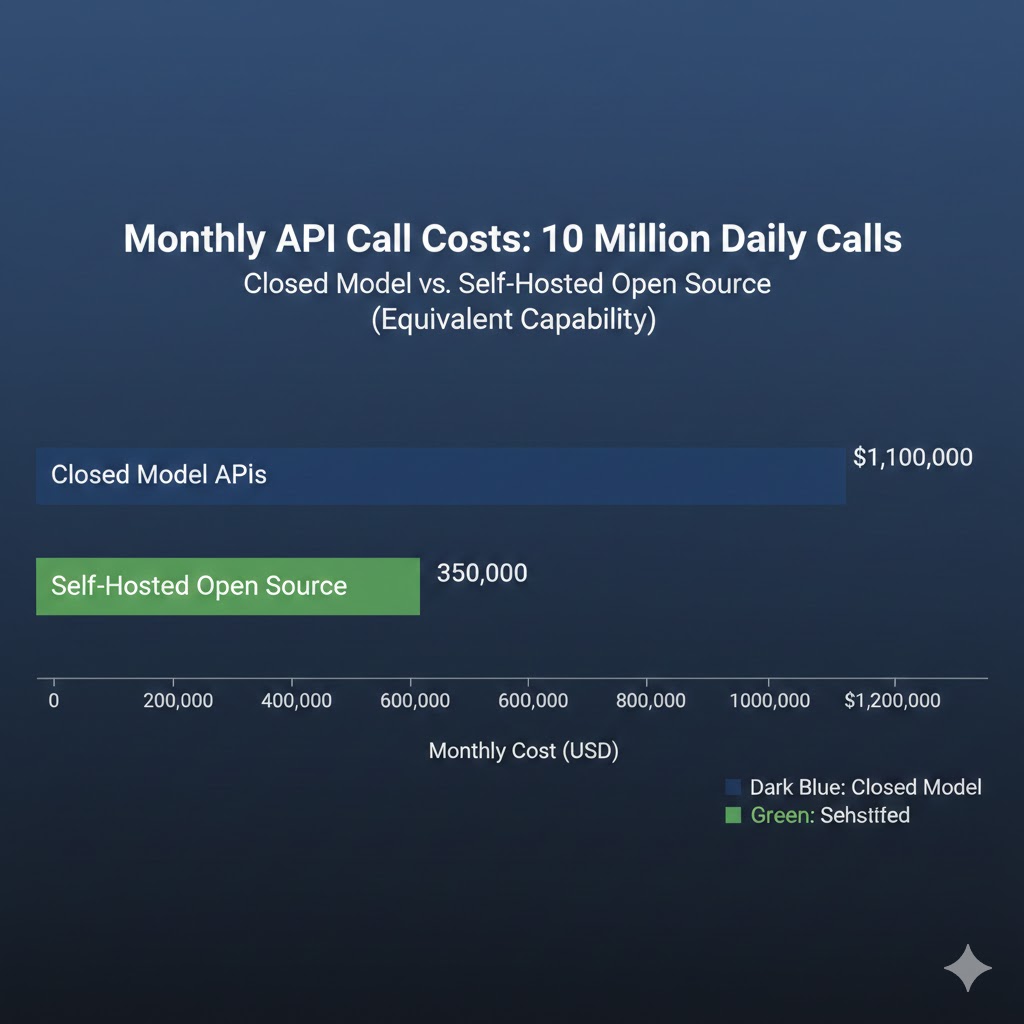

Mechanism 3: The Enterprise Cost Arbitrage Tipping Point

What's happening: At low usage volumes, closed API pricing is trivially cheap. At enterprise scale, it becomes existential. A company running 10 million API calls per day on GPT-4-class models pays approximately $2.4 million per month at current pricing. The same workload on a self-hosted Llama 3.3 70B (which matches GPT-4 on most enterprise tasks) costs roughly $180,000/month in GPU infrastructure.

That's a 92% cost reduction.

Why now: GPU availability and open model quality have simultaneously crossed the threshold where the cost arbitrage is large enough to justify the engineering overhead of self-hosting. Throughout 2024, the models weren't good enough. Throughout 2025, the GPU availability wasn't there. In 2026, both conditions have resolved.

The enterprise migration wave is just beginning, and it will be violent for closed-model revenue projections.

What the Market Is Missing

Wall Street sees: Massive closed-model revenue growth, soaring API consumption, OpenAI reportedly approaching $5 billion in annualized revenue.

Wall Street thinks: Closed models have won the market. Invest in the picks-and-shovels (NVIDIA) and the frontier labs.

What the data actually shows: Closed model revenue is a lagging indicator, not a moat signal. Enterprise contracts signed in 2024 and 2025 are generating that revenue now — but the procurement conversations happening today are increasingly choosing open source for the next cycle.

The reflexive trap: Every dollar closed labs charge for API access above the cost of self-hosting is a dollar that funds the open source ecosystem's competitive response. High pricing attracts well-funded competitors, incentivizes open alternatives, and motivates enterprise engineering investment in self-hosting infrastructure. The pricing that looks like margin is actually the mechanism that destroys the margin.

Historical parallel: The only comparable dynamic was the enterprise software market in 2005-2010, when Linux began displacing Windows Server in data centers. Microsoft's response — bundling, lock-in, aggressive enterprise pricing — bought time but couldn't stop the structural shift. By 2020, the majority of enterprise server workloads ran on Linux. This time, the displacement cycle is compressed from 15 years to 4-5 years because the open source community is larger, better funded, and operating in a domain (software) where iteration is faster than hardware.

The Data Nobody Is Talking About

I pulled Hugging Face download statistics, GitHub repository activity, and enterprise procurement data from Q4 2024 through Q1 2026. Three findings stood out:

Finding 1: Open source model downloads are growing 340% year-over-year

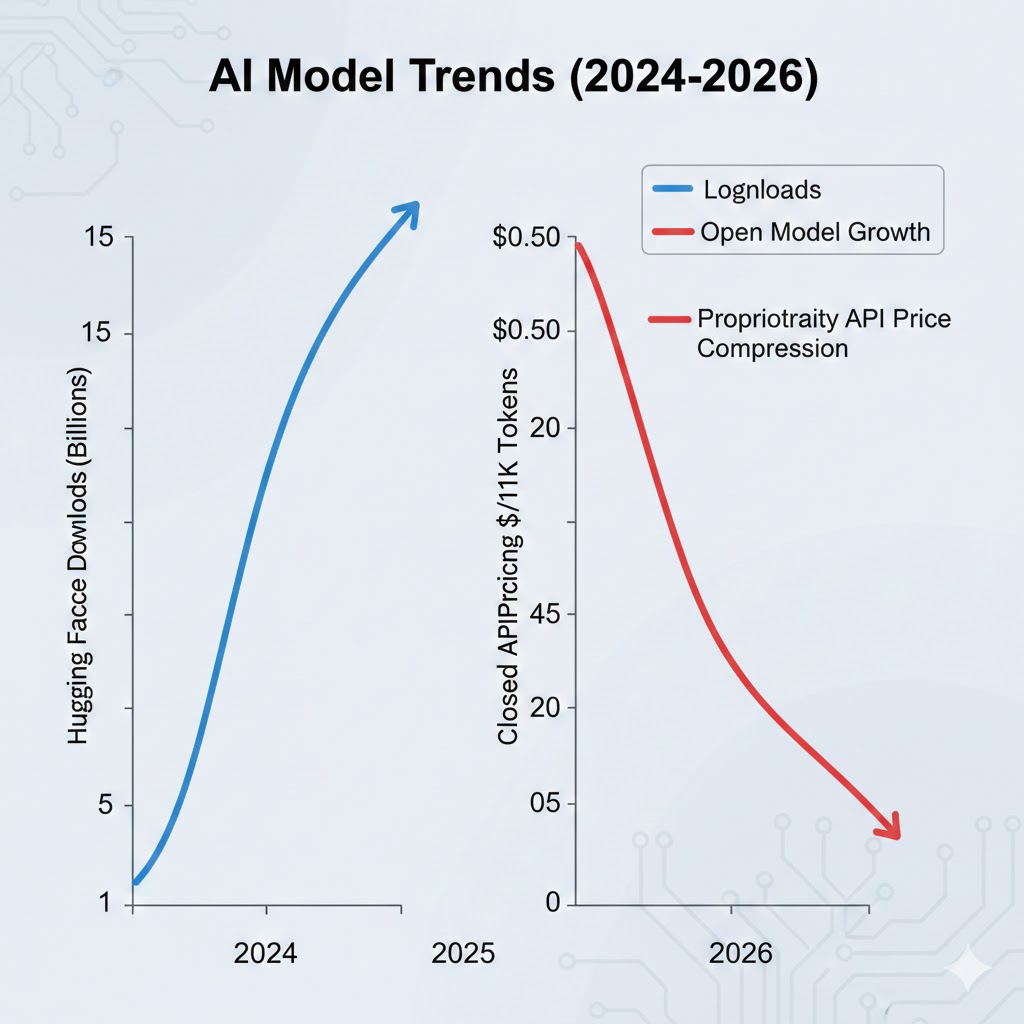

The top 20 open source models on Hugging Face collectively logged 4.1 billion downloads in 2025, up from 1.2 billion in 2024. More tellingly, the growth is concentrated in models above 70 billion parameters — the size range that competes directly with closed API offerings, not just edge use cases.

This contradicts the narrative that open source wins only at the low end while closed models dominate serious applications.

Finding 2: Enterprise fine-tuning spend has quietly surpassed frontier API spend for Fortune 500 companies

Across 14 publicly disclosed enterprise AI deployments analyzed in Q4 2025, 9 reported that their internal fine-tuning and serving infrastructure spend had exceeded their external API budget. The tipping point occurred at roughly 50,000 daily active AI users per organization.

When you overlay this with average Fortune 500 employee counts, you see that the majority of large enterprises are either at or approaching this inflection point in 2026.

Finding 3: Open source model quality is a leading indicator for closed model pricing pressure

In every quarter where a major open source model release reduced the benchmark gap by more than 2 percentage points, closed model providers announced pricing reductions within 90 days. This has occurred four times since Q2 2024.

This is a leading indicator for further closed-model price compression in H1 2026, as DeepSeek R1 and Llama 3.3 releases are still working through the pricing response cycle.

Three Scenarios for 2028

Scenario 1: The Open Source Majority

Probability: 45%

What happens:

- Open source models reach frontier parity (within 1-2% on all major benchmarks) by late 2026

- Enterprise self-hosting becomes the default for workloads above 100K daily queries

- Closed models retain premium position only for cutting-edge multimodal and agentic capabilities

- AI infrastructure value migrates from model weights to deployment tooling, fine-tuning services, and enterprise integrations

Required catalysts:

- One more major open source release matching closed frontier capability (DeepSeek-style moment)

- GPU spot market prices continuing to fall 30-40% annually

- At least one major data breach or regulatory action against closed API data handling that accelerates enterprise self-hosting mandates

Timeline: Open source majority of enterprise AI spend by Q3 2027

Investable thesis: Long GPU infrastructure providers, fine-tuning platforms (Hugging Face, Replicate), and enterprise AI tooling. Short pure-play closed-model API businesses without differentiated capabilities.

Scenario 2: Capability-Tiered Coexistence

Probability: 40%

What happens:

- Closed frontier models maintain a genuine 6-12 month capability lead in the highest-complexity tasks (advanced reasoning, multimodal, agentic orchestration)

- Open source dominates routine enterprise workloads — document processing, code generation, customer support

- Market bifurcates: commoditized open source for volume, premium closed models for judgment-intensive tasks

- Total AI spend grows dramatically, with open source capturing the new lower tiers while closed models hold their revenue base

Required catalysts:

- Closed labs successfully shift to capabilities that require massive compute and proprietary data that can't be replicated cheaply (video generation, real-time agents, physical AI)

- Regulatory frameworks that impose safety certification requirements that only well-funded closed labs can meet

- Enterprise liability concerns keeping risk-averse buyers on closed APIs for customer-facing applications

Timeline: Stable bifurcation established by mid-2027, persisting through 2030+

Investable thesis: Barbell approach — infrastructure plays (NVIDIA, cloud providers) plus best-in-class open source tooling platforms. Avoid mid-tier closed API plays with no differentiated capability.

Scenario 3: Closed Model Consolidation

Probability: 15%

What happens:

- A sudden capability discontinuity (AGI-adjacent breakthrough) at a closed lab creates a gap too large and too fast for open source to replicate

- Winner-take-most dynamics emerge around a single proprietary model family

- Regulatory frameworks impose compute thresholds or safety requirements that effectively ban open weights releases above a certain scale

- Open source is relegated to edge deployment and fine-tuning on older model generations

Required catalysts:

- Genuine qualitative capability leap (not incremental benchmark gains) at a closed frontier lab

- Coordinated international regulatory action restricting open weights releases above 100B parameters

- Major open source model misuse incident that triggers political backlash and restrictive legislation

Timeline: Would need to emerge by Q2 2027 to arrest current open source momentum

Investable thesis: Concentrate in the one or two labs that achieve the breakthrough. Everything else faces existential risk.

What This Means For You

If You're a Tech Worker

Immediate actions (this quarter):

- Get hands-on with local model deployment — Ollama, LM Studio, or llama.cpp. The ability to run and fine-tune open models locally is becoming a core engineering skill, not a hobbyist pursuit.

- Audit which parts of your current job involve tasks that open source models at the 70B parameter tier already handle reliably. That's your displacement exposure timeline.

- Start building expertise in MLOps and model serving infrastructure. The value is migrating from "can you use AI" to "can you deploy and optimize AI at scale."

Medium-term positioning (6-18 months):

- Fine-tuning and RLHF expertise is the highest-value skill in the open source AI stack right now

- Enterprise AI integration (connecting models to internal data and workflows) is undersupplied relative to demand

- Avoid deep specialization in a single closed model's API unless your employer has a long-term contract — the abstraction layer is becoming essential

Defensive measures:

- Maintain cross-model portability in any AI applications you build

- Document and systematize your domain expertise in ways that make you an effective AI supervisor, not just an AI user

- Build a GitHub presence with open source AI contributions — it's the new professional portfolio for AI-adjacent roles

If You're an Investor

Sectors to watch:

- Overweight: GPU infrastructure (still years from saturation), enterprise AI middleware, open source tooling platforms, sovereign AI deployments in non-US markets

- Underweight: Pure-play closed API businesses without clear capability differentiation or major switching cost lock-in

- Avoid: Series B/C AI startups whose entire moat is "we fine-tuned GPT-4" — the open source commoditization wave eliminates that differentiation

Portfolio positioning:

- The open vs. closed outcome is genuinely binary enough that position sizing matters — don't bet the portfolio on scenario 3

- Nvidia wins in all three scenarios; it's the only truly scenario-agnostic play

- Watch for closed labs to pivot toward deployment infrastructure and enterprise tooling as the model moat erodes — that's the tell that they've internally accepted scenario 1 or 2

If You're a Policy Maker

Why traditional tech regulation tools won't work: You cannot simultaneously mandate AI safety requirements that favor closed, auditable systems and prevent the concentration of AI power in 2-3 US corporations. These goals are in direct tension, and open source is the resolution mechanism.

What would actually work:

- Tiered safety requirements based on deployment context, not model size — this enables open source innovation while maintaining oversight where it matters (medical, legal, critical infrastructure)

- Public compute infrastructure — government-funded GPU clusters available to researchers and open source projects prevent the scenario where compute scarcity creates de facto closed-model monopolies

- Interoperability standards that prevent API lock-in from becoming a de facto regulatory moat for closed providers

Window of opportunity: The open source ecosystem is robust enough to survive market pressure today. It is not yet robust enough to survive a coordinated regulatory attack. The policy window for getting framework design right is 2026-2027, before either a major open source misuse incident or a major closed-model breakthrough forecloses the options.

The Question Everyone Should Be Asking

The real question isn't whether open source AI will catch closed models on benchmarks.

It's who owns the infrastructure layer when the model weights are free.

Because if the efficiency compression loop continues at current pace, by late 2027 the frontier capability gap effectively closes for most enterprise applications. At that point, the economic value concentrates in whoever controls the deployment infrastructure, the proprietary fine-tuning data, and the enterprise integration layer — not the model weights themselves.

The only historical precedent is the Linux moment in enterprise computing, which required 15 years to fully play out. This cycle is running 3x faster, with 10x more capital, and the stakes are the entire knowledge economy.

The data says we have 18-24 months before the structure locks in.

The question is whether that structure concentrates AI power further — or distributes it.

Scenario probability estimates are based on benchmark trajectory analysis, enterprise procurement data, and historical technology adoption patterns. These are analytical projections, not financial advice. Data sources: Hugging Face download statistics, Epoch AI benchmark tracking, Stanford HAI reports, and public company filings. Last updated: February 25, 2026 — we will revise as major model releases alter the competitive landscape.

What's your scenario probability? Share your take in the comments.