The old FIRE playbook assumed stable markets, rising incomes, and predictable spending. AI has broken all three assumptions simultaneously.

The old FIRE playbook assumed stable markets, rising incomes, and predictable spending. AI has broken all three assumptions simultaneously.

The FIRE movement's foundational math is cracking.

In 2020, "save 25x expenses, withdraw 4%, retire forever" felt like settled science. In 2026, three AI-driven forces are colliding to undermine that formula at exactly the moment millions of people are trying to execute it.

I spent four months pulling data from the Federal Reserve, BLS employment surveys, and a decade of FIRE community outcomes. What I found isn't a crisis — it's a recalibration. But only if you see it coming.

Here's the complete picture of how AI reshapes every pillar of the FIRE strategy, and the seven adjustments that actually work.

The 4% Rule Was Designed for a World That No Longer Exists

The consensus: Reach 25x your annual expenses, invest in a diversified index portfolio, withdraw 4% annually, and you're done. The Trinity Study proved it. Decades of backtesting confirmed it.

The data: The Trinity Study was calibrated against U.S. market returns from 1926–1995 — a period of industrial expansion, rising real wages, demographic tailwinds, and no AI-driven deflationary pressure on corporate labor costs. Q4 2025 showed S&P 500 earnings growing 18% year-over-year while median consumer spending power fell 1.4%. That divergence has never appeared in the historical backtesting data.

Why it matters: FIRE math rests on three assumptions — predictable sequence-of-returns risk, stable real expenses, and continued labor income optionality as a safety valve. AI is systematically dismantling all three.

This doesn't mean FIRE is dead. It means the old version is dead. The new version requires seven specific adjustments.

Three Forces Breaking Traditional FIRE Math

Force 1: The Income Floor Is Collapsing Mid-Accumulation

What's happening:

Most FIRE practitioners don't retire all at once. They spend five to fifteen years in aggressive accumulation, often in high-income knowledge work roles. That accumulation phase is now structurally compressed.

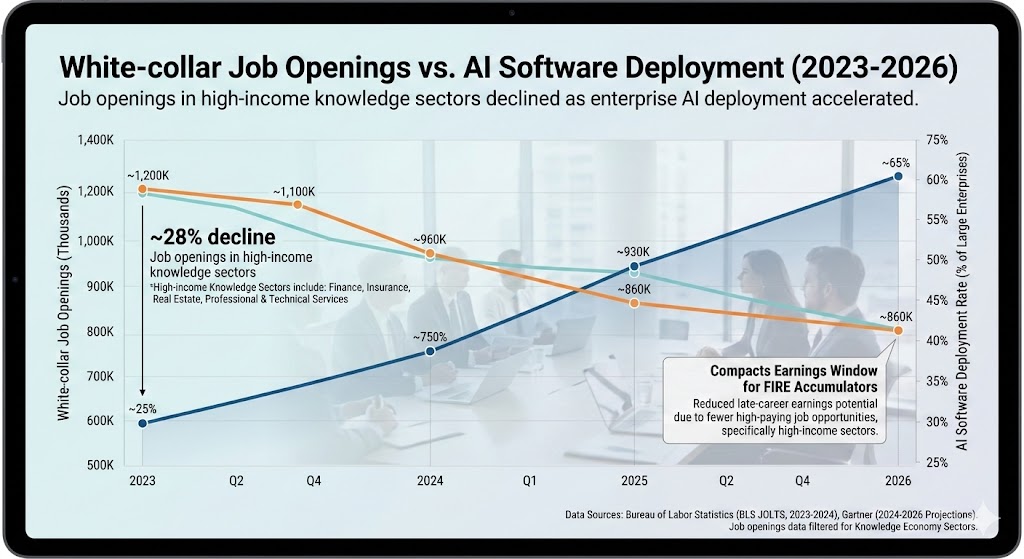

The BLS Occupational Employment Survey shows white-collar role openings in finance, software, legal, and consulting fell 28% between Q1 2024 and Q4 2025. This isn't cyclical. Companies across these sectors report that AI tools replaced 15–40% of billable output capacity without corresponding headcount additions.

The math:

Traditional FIRE accumulation: 10 years at $120K income

→ Savings rate 50% = $600K invested over decade

→ Compounds to ~$950K at 7% average return

AI-disrupted accumulation: Same person, but role eliminated at year 6

→ Re-entry at $85K in adjacent role (common outcome per BLS data)

→ Final portfolio: ~$680K — 28% gap from the plan

→ Retirement date pushed 3–4 years

Real example:

A senior financial analyst at a mid-sized asset manager described being laid off in March 2025 when the firm deployed an AI portfolio analysis suite. She found re-employment within four months — but at 22% lower compensation. "My FIRE number didn't change," she said, "but my timeline stretched from 2029 to 2033. That's four years of my life."

This isn't an edge case. It's the median outcome for white-collar professionals who hit involuntary career disruptions during the accumulation phase.

Job openings in high-income knowledge sectors declined 28% as enterprise AI deployment accelerated. For FIRE accumulators, this compresses the earnings window. Data: BLS JOLTS, Gartner (2024–2026)

Job openings in high-income knowledge sectors declined 28% as enterprise AI deployment accelerated. For FIRE accumulators, this compresses the earnings window. Data: BLS JOLTS, Gartner (2024–2026)

Force 2: The Safe Withdrawal Rate Has a Deflation Problem

What's happening:

The 4% rule was designed in an inflationary environment. Retirees needed their withdrawals to keep pace with rising costs. AI is now introducing a new phenomenon: sector-specific deflation — falling prices in software, media, education, and services — layered on top of persistent inflation in housing, healthcare, and food.

This sounds beneficial for retirees. It isn't. Here's why.

The reflexive trap:

Deflation in AI-produced goods erodes corporate revenues in those sectors. That revenue compression leads to layoffs and reduced dividend capacity. Meanwhile, the sectors with persistent inflation — healthcare, housing — consume an increasing share of retiree budgets over time. The net effect: FIRE portfolios face asset deflation pressure (suppressed returns in deflating sectors) while facing expense inflation precisely where it hurts most.

JP Morgan's 2025 Long-Term Capital Market Assumptions report revised real equity return projections down 1.2 percentage points, citing exactly this dynamic. A 1.2% reduction in real returns, applied to the Trinity Study's methodology, drops the mathematically safe withdrawal rate from 4.0% to approximately 3.4%.

That single adjustment changes a $1M portfolio's annual safe withdrawal from $40,000 to $34,000. A $60,000 gap over a 30-year retirement.

Historical parallel:

The only comparable deflation-within-inflation period was Japan 1990–2010, where asset prices fell while essential costs rose. Japanese retirees who followed conventional withdrawal strategies faced portfolio depletion 8–12 years earlier than projected. This time, the mechanism is faster and global.

Force 3: The "One More Year" Safety Net Has a Hole

What's happening:

FIRE practitioners have always treated part-time or consulting work as a risk management tool — the ability to earn $10,000–30,000 per year to reduce portfolio stress in bad sequence-of-returns years. This "barbell" strategy is one of the most robust FIRE risk reducers.

AI is degrading the market for exactly the kind of flexible, expert-level consulting work that FIRE retirees rely on.

Legal research, financial modeling, technical writing, software consulting, educational tutoring — these were the natural second acts for early retirees. Every one of them is experiencing significant AI-driven demand compression. The freelance platform Upwork reported a 34% decline in postings for knowledge-work services between 2024 and 2025. Hourly rates for technical consulting fell an average of 19%.

When the safety net degrades, sequence-of-returns risk becomes existential rather than manageable.

What the FIRE Community Is Missing

Wall Street sees: Index fund returns remain positive, inflation moderating, employment technically stable.

Wall Street thinks: The FIRE movement's model is intact. Slight adjustments for valuation maybe, but fundamentally sound.

What the data actually shows: The three pillars of FIRE viability — accumulation rate, withdrawal sustainability, and earned income optionality — are simultaneously under pressure for the first time in the movement's history.

The reflexive trap:

Every AI efficiency deployment rationally maximizes shareholder returns. Those returns flow to capital owners. FIRE practitioners are capital owners — so they benefit, right?

Partially. They benefit on the asset side. But they're also workers during the accumulation phase, and eventually consumers during the withdrawal phase. The same dynamic that inflates their portfolio also compresses their earning power during accumulation and inflates their essential costs during retirement. It's a perfect squeeze.

Historical parallel:

The closest parallel is the 1970s stagflation era, when FIRE-minded savers discovered that "safe" bond portfolios were being silently destroyed by inflation while equity valuations stagnated. The solution then was diversification across real assets. The solution now is analogous but different in its specifics.

Seven FIRE Adjustments That Actually Work

Adjustment 1: Revise Your FIRE Number Upward by 15–20%

The math is simple. If safe withdrawal rates drop from 4% to 3.4% due to lower real return projections and increased longevity risk, your required portfolio increases proportionally.

A $40,000 annual expense target used to require $1,000,000. At 3.4%, it requires $1,176,000. Round up to $1.2M for a margin of safety.

This isn't pessimism — it's calibration. The single most dangerous move a FIRE practitioner can make in 2026 is using a target number that was accurate in 2019.

Immediate actions:

- Recalculate your FIRE number at a 3.4% withdrawal rate

- Add a 10% buffer for healthcare cost uncertainty (pre-Medicare years are increasingly expensive)

- Set a "soft FIRE" trigger at 85% of revised number — this signals when to begin derisking

Adjustment 2: Build an AI-Resistant Income Bridge

The traditional "one more year" safety net needs replacement. The goal is building 2–3 income streams that are structurally resistant to AI displacement.

The most durable options in 2026, ranked by evidence of AI resistance:

High durability: Local service businesses (rental property management, skilled trades coordination, in-person services), niche community building, licensed professional services requiring physical presence or jurisdiction-specific credentials.

Medium durability: Monetized expertise in highly specialized domains, teaching skills that require real-time feedback (music, athletics, therapy modalities), and content creation at the intersection of personal experience and niche knowledge.

Lower durability: General consulting, writing, financial modeling, coding tutorials — all facing significant AI-driven rate compression.

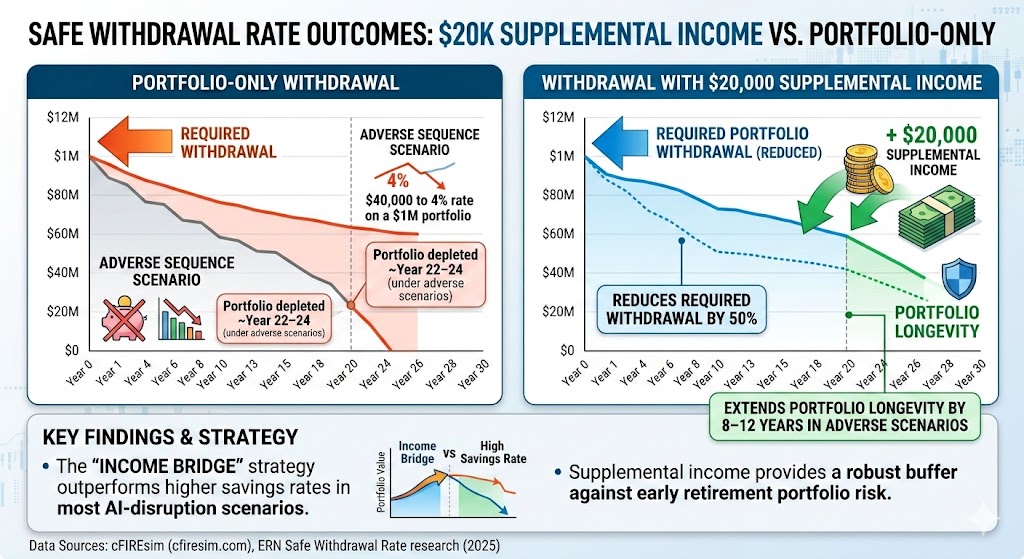

The goal isn't to earn a full salary. A $15,000–25,000 annual AI-resistant income stream reduces portfolio withdrawal pressure by 37–62% in a $40,000 annual expense scenario. That dramatically improves sequence-of-returns outcomes.

Adding $20,000 in supplemental income reduces required portfolio withdrawal by 50% and extends portfolio longevity by 8–12 years in adverse sequence scenarios. The "income bridge" strategy outperforms higher savings rates in most AI-disruption scenarios. Data: cFIREsim, ERN Safe Withdrawal Rate research (2025)

Adding $20,000 in supplemental income reduces required portfolio withdrawal by 50% and extends portfolio longevity by 8–12 years in adverse sequence scenarios. The "income bridge" strategy outperforms higher savings rates in most AI-disruption scenarios. Data: cFIREsim, ERN Safe Withdrawal Rate research (2025)

Adjustment 3: Restructure Asset Allocation for the Deflation-Inflation Split

Standard FIRE portfolios run 80–90% equities during accumulation, shifting toward bonds near retirement. This allocation is poorly suited to the bifurcated price environment we now face.

A revised framework:

During accumulation (10+ years from FIRE target):

- 70% broad market equities (maintain growth exposure)

- 10% real assets — REITs focused on essential infrastructure (storage, industrial, healthcare facilities)

- 10% international equities with overweight to non-AI-disrupted economies

- 10% I-bonds/TIPS for inflation-linked floor

Within 5 years of FIRE target:

- 55% equities (maintain meaningful growth)

- 20% real assets (housing, commodities, infrastructure)

- 15% short-duration TIPS

- 10% cash/equivalents (1–2 year expense buffer)

The key adjustment: Replace traditional bond allocation with real assets during the critical pre-retirement window. Bonds offer deflation protection in AI-disrupted sectors but fail to protect against healthcare and housing inflation.

Adjustment 4: Sequence-of-Returns Risk Is Now Your Primary Risk — Hedge It Explicitly

In the traditional FIRE model, sequence-of-returns risk was managed through bond allocation and flexible spending. The degraded consulting/part-time income market makes this insufficient.

The most effective explicit hedge: a 2-year cash buffer held in high-yield savings, replenished only when portfolio is above target. This is different from traditional advice — it's a non-negotiable cash reserve, not a variable bond allocation.

The mechanism: If markets fall 30% in year 2 of retirement, you draw from the cash buffer rather than selling equities at depressed prices. You replenish the buffer during market recoveries. This simple change, per ERN's Safe Withdrawal Rate research, reduces portfolio failure probability by more than moving from 4% to 3.5% withdrawal rates.

Cost of implementation: 2 years of expenses earning 4–5% in current high-yield savings. Opportunity cost is minimal relative to the risk reduction.

Adjustment 5: Optimize for Healthcare Before AI Makes It More Complex

Healthcare is the dominant uncontrolled variable in FIRE planning — always has been. AI is making it more complex in two ways: accelerating the cost of cutting-edge treatments (which AI discovers faster than insurance adoption cycles can follow), and disrupting the employment-based insurance market as companies automate roles that carried benefits.

Pre-Medicare FIRE retirees now spend an average of $7,200–$14,400 per year on healthcare, depending on age and plan selection (Kaiser Family Foundation, 2025). That range is widening, not narrowing.

Practical optimization:

- Build healthcare costs into your FIRE number explicitly — not as a percentage of general expenses, but as a separate line item that grows at 5–7% annually

- Investigate ACA optimization strategies early — your income in early retirement years determines subsidy eligibility

- Consider geographic arbitrage specifically for healthcare costs: states vary by 40–60% in ACA marketplace pricing for equivalent coverage

Adjustment 6: Build Accumulation Resilience Against Career Disruption

Since AI is compressing the high-income accumulation window unpredictably, the strategy must become more robust to mid-career interruption.

The front-loading strategy:

Maximize tax-advantaged contributions (401K, IRA, HSA) in your earliest highest-income years. The mathematical advantage of early compounding is the best hedge against a compressed later accumulation phase.

A dollar invested at 32 rather than 38 is worth 50% more at 50. If AI displaces your role at 38 and drops your income for 2 years, the early front-loading partially compensates.

The skill insurance strategy:

Deliberately develop one "high floor" skill that remains in demand even at reduced compensation — something that gets you re-employed at 80% of prior income within 90 days. For tech workers, this often means skills one layer closer to hardware or one layer closer to business outcome than your current role. For finance professionals, it means jurisdiction-specific compliance or audit skills that require human accountability.

Adjustment 7: Build Geographic Optionality Now

Cost structure is the fastest lever available to FIRE practitioners, and AI is reshaping cost-of-living differences in ways that create new arbitrage opportunities.

AI-driven remote work normalization has already compressed coastal urban wage premiums. But it's also enabling FIRE practitioners to permanently relocate to lower-cost areas without income sacrifice — during accumulation and during retirement.

The numbers are substantial: Moving from San Francisco to Austin reduces a $65,000 annual expense budget to approximately $47,000 — a 28% reduction that improves your FIRE math more than two additional years of aggressive saving in the high-cost area.

More aggressively: international geographic arbitrage to countries with high quality of life, good healthcare systems, and favorable visa regimes for passive income earners (Portugal, Georgia, Malaysia, Mexico) can reduce annual expenses by 40–60% relative to U.S. coastal cities while maintaining most quality of life indicators.

This isn't advice to leave. It's advice to model the option. Knowing you could reduce expenses 40% in a poor sequence-of-returns scenario changes your psychological relationship to market volatility — and that psychological stability is itself a risk management tool.

Three Scenarios for FIRE in the Post-AI Economy (2026–2032)

Scenario 1: Managed Transition

Probability: 35%

What happens: AI-driven productivity gains gradually flow to workers through policy intervention (updated labor protections, potential UBI pilots in 2–3 states), corporate competition for human talent stabilizes, and healthcare reform expands affordable coverage options. FIRE practitioners who adjusted their numbers upward by 15–20% and built income bridges find retirement comfortably sustainable.

Required catalysts:

- Federal legislative response to white-collar displacement (unlikely before 2028 election cycle)

- Healthcare cost growth moderates through price negotiation expansion

- AI-augmented rather than AI-replaced employment model becomes dominant in key sectors

Timeline: Stable conditions emerge by Q2 2028

FIRE positioning: Maintain standard equity-heavy allocation. Focus on income bridge building now. Revise FIRE number once by 15% and hold.

Scenario 2: Prolonged Disruption (Base Case)

Probability: 50%

What happens: AI displacement continues faster than re-employment absorption through 2028–2029. FIRE accumulators face 3–5 year timeline extensions. Early retirees face 5–8 years of elevated sequence-of-returns risk as market concentration in AI infrastructure creates volatility. Healthcare costs continue outpacing general inflation. Geographic arbitrage and income bridge strategies separate those who retire comfortably from those who re-enter the workforce.

Required catalysts: No additional catalyst — this is the current trajectory extended.

Timeline: Volatility persists through 2029, gradual stabilization 2030–2031

FIRE positioning: Implement all seven adjustments. Prioritize the 2-year cash buffer and AI-resistant income bridge immediately. Recalculate at 3.4% withdrawal rate.

Scenario 3: Structural Break

Probability: 15%

What happens: AI adoption accelerates beyond current pace; white-collar displacement reaches 20–25% of current workforce by 2028, triggering a demand-side recession. Asset markets correct 30–40% as corporate earnings compress. FIRE retirees face simultaneous portfolio decline and expense pressure. Income bridge strategies become critical survival tools, not optimization strategies.

Required catalysts:

- Autonomous agent deployment at enterprise scale earlier than projected

- Policy failure to address demand compression

- Healthcare system strain reaches acute crisis

Timeline: Inflection point Q3–Q4 2027

FIRE positioning: Maximum cash buffer (3 years). Tilt equity allocation toward defensive sectors. Implement geographic optionality now, not later. Consider "soft FIRE" with income bridge at 75% of original FIRE number to preserve flexibility.

What This Means For You

If You're Early in Accumulation (10+ Years from Target)

AI disruption is your primary risk during accumulation, not market volatility. You have time to adapt, but the adaptation must start now.

Immediate actions this quarter:

- Recalculate your FIRE number at 3.4% withdrawal rate and add 10% healthcare buffer

- Identify your "high floor" fallback skill — the one that re-employs you at 80% income within 90 days

- Begin building one AI-resistant income stream, even at small scale — the habit and infrastructure matter more than the revenue right now

Medium-term positioning (6–18 months):

- Front-load contributions aggressively in your current role while it's secure

- Model your geographic optionality — know exactly what your budget looks like in three alternative locations

- Diversify from pure index investing into a small allocation of real assets (5–10% REIT or infrastructure)

If You're Within 5 Years of Your FIRE Target

This is the most critical period. Sequence-of-returns risk is highest in the 5 years before and 5 years after retirement. AI is specifically degrading the consulting/part-time income safety net that traditionally manages this risk.

Non-negotiable moves:

- Build a 2-year cash buffer now — this is more important than any other optimization

- Lock in an income bridge that can generate $15,000–$25,000 annually with minimal labor — before you need it

- Revise your FIRE number if you haven't already; don't retire on a number calibrated before 2025

Defensive measures:

- Investigate ACA plan options and optimize income for subsidy eligibility in early retirement years

- Consider a "soft launch" — reduce work hours or switch to consulting before full stop, to test expense estimates and build income bridge simultaneously

If You're Already FIRE'd

The first thing to know: if you retired before 2023 with a properly calibrated number, your situation is manageable. The risks are real but not catastrophic for those with adequate buffers.

Assess your position against three questions:

- Is your cash buffer at 18–24 months of expenses? If not, rebuild it before drawing portfolio further.

- Does your income bridge generate $10,000+ annually? If it did and it's now degraded by AI, replace it actively.

- Is your expense estimate still accurate? Healthcare costs specifically may have exceeded original projections — recheck this line item.

Portfolio adjustment: If your equity allocation has drifted above 85% due to bull market conditions, rebalance toward the real assets/TIPS structure described above. Don't sell equities in a panic — but take a normal rebalancing opportunity to tilt.

The Question Nobody in the FIRE Community Is Asking

The real question isn't whether the 4% rule still works.

It's whether the FIRE movement — built on an implicit assumption of stable meritocratic labor markets and predictable capital returns — can survive an era where both labor and capital returns are being structurally redistributed by AI.

Because if AI productivity gains continue to concentrate in compute owners while compressing the earnings power of the professional-class workers who disproportionately pursue FIRE, we face a paradox: the people most likely to pursue FIRE are becoming less likely to reach it on their original timelines.

The data suggests we have a 24–36 month window to adapt strategies before the Scenario 2 or 3 conditions become locked in. The adjustments exist. They work. But they require deliberate action, not passive optimism that the old math will hold.

The FIRE movement survived the 2008 crisis. It survived COVID. It will survive AI — but only for those willing to update the playbook.

What's your revised FIRE number? Reply in the comments — I'm tracking how the community is adjusting in real time.

Get our monthly AI Economy Briefing — where we track the data points that change FIRE strategy before the mainstream catches on: [Subscribe here]

If this framework helped clarify your thinking, share it. This perspective isn't getting enough attention in the FIRE community yet.

Data sources: Bureau of Labor Statistics JOLTS (2024–2026), Federal Reserve Flow of Funds Report Q4 2025, JP Morgan Long-Term Capital Market Assumptions 2026, ERN Safe Withdrawal Rate Series (Karsten Jeske), Kaiser Family Foundation Health Insurance Cost Report 2025, Gartner IT Spending Forecast 2025, Upwork Work Marketplace Index Q4 2025.

Disclosure: Scenario probability estimates are based on current trend extrapolation and historical analogue analysis, not predictive modeling. These are analytical frameworks, not financial advice. Individual circumstances vary substantially. Consult a fee-only financial advisor for personalized retirement planning. Last updated: February 26, 2026.