Problem: Financial Data Is Scattered Across Too Many APIs

You want an agent that fetches live stock prices, runs basic technical analysis, and returns a structured report — but every tutorial either skips the API wiring or glosses over error handling in production.

You'll learn:

- How to connect an LLM agent to real-time stock APIs using tool calling

- How to structure financial data so the model reasons correctly

- How to handle rate limits and bad data without crashing

Time: 45 min | Level: Intermediate

Why This Happens

Most "AI trading agent" demos use mocked data. Real stock APIs return noisy, inconsistent JSON — missing fields, delayed quotes, rate limit errors — and vanilla LangChain agents fall apart when they hit a None price or a 429 response.

Common symptoms:

- Agent hallucinates prices when the API returns an error

- Tool calls loop infinitely when data is stale

- No fallback when market is closed

Solution

Step 1: Set Up Dependencies

pip install langchain langchain-openai yfinance pandas ta requests python-dotenv

Create .env:

OPENAI_API_KEY=sk-...

ALPHA_VANTAGE_KEY=your_key_here # Free tier at alphavantage.co

Why two APIs: yfinance is free but fragile; Alpha Vantage is rate-limited but stable. We use yfinance for quick quotes and Alpha Vantage for fundamentals.

Step 2: Build the Stock Data Tools

The agent needs typed tools — not raw functions. This lets the model understand what each tool returns and when to use it.

# tools/stock_tools.py

import yfinance as yf

import pandas as pd

from ta.trend import SMAIndicator

from ta.momentum import RSIIndicator

from langchain_core.tools import tool

from typing import Optional

@tool

def get_current_price(ticker: str) -> dict:

"""Fetch real-time price and basic stats for a stock ticker."""

try:

stock = yf.Ticker(ticker.upper())

info = stock.fast_info # faster than .info, fewer fields

price = info.last_price

if price is None:

return {"error": f"No price data for {ticker}. Market may be closed."}

return {

"ticker": ticker.upper(),

"price": round(price, 2),

"day_high": round(info.day_high or 0, 2),

"day_low": round(info.day_low or 0, 2),

"volume": info.last_volume,

"market_cap": info.market_cap,

}

except Exception as e:

# Return structured error — never let the agent see a raw traceback

return {"error": str(e), "ticker": ticker}

@tool

def get_technical_indicators(ticker: str, period: str = "3mo") -> dict:

"""

Calculate RSI and 20/50-day SMA for a given ticker.

period: '1mo', '3mo', '6mo', '1y'

"""

try:

df = yf.download(ticker.upper(), period=period, progress=False)

if df.empty or len(df) < 50:

return {"error": f"Not enough data for {ticker} ({period})"}

close = df["Close"].squeeze() # squeeze fixes MultiIndex issue in yfinance 0.2+

rsi = RSIIndicator(close=close, window=14).rsi().iloc[-1]

sma20 = SMAIndicator(close=close, window=20).sma_indicator().iloc[-1]

sma50 = SMAIndicator(close=close, window=50).sma_indicator().iloc[-1]

return {

"ticker": ticker.upper(),

"rsi_14": round(float(rsi), 2),

"sma_20": round(float(sma20), 2),

"sma_50": round(float(sma50), 2),

"trend": "bullish" if sma20 > sma50 else "bearish",

}

except Exception as e:

return {"error": str(e), "ticker": ticker}

@tool

def compare_stocks(tickers: list[str]) -> list[dict]:

"""

Compare current price and RSI for multiple tickers.

Pass a list: ["AAPL", "MSFT", "GOOGL"]

"""

results = []

for ticker in tickers[:5]: # cap at 5 to avoid rate limits

price_data = get_current_price.invoke(ticker)

tech_data = get_technical_indicators.invoke(ticker)

results.append({**price_data, **tech_data})

return results

Expected: Each tool returns a dict, never raises. The error key tells the agent to retry or explain the failure instead of looping.

If it fails:

AttributeError: 'DataFrame' has no attribute 'squeeze': Update yfinance:pip install yfinance --upgradeKeyError: 'Close': Ticker doesn't exist — add validation before the download

Step 3: Wire the Agent

# agent.py

import os

from dotenv import load_dotenv

from langchain_openai import ChatOpenAI

from langchain.agents import create_tool_calling_agent, AgentExecutor

from langchain_core.prompts import ChatPromptTemplate

from tools.stock_tools import get_current_price, get_technical_indicators, compare_stocks

load_dotenv()

SYSTEM_PROMPT = """You are a financial analysis assistant. Your job is to:

1. Fetch real-time stock data using the provided tools

2. Interpret technical indicators (RSI > 70 = overbought, < 30 = oversold)

3. Return a structured analysis with a clear buy/hold/watch recommendation

Always cite the data you retrieved. Never guess prices or invent indicators.

If a tool returns an error, explain it to the user rather than retrying indefinitely."""

tools = [get_current_price, get_technical_indicators, compare_stocks]

prompt = ChatPromptTemplate.from_messages([

("system", SYSTEM_PROMPT),

("human", "{input}"),

("placeholder", "{agent_scratchpad}"),

])

llm = ChatOpenAI(model="gpt-4o-mini", temperature=0) # low temp for factual tasks

agent = create_tool_calling_agent(llm, tools, prompt)

executor = AgentExecutor(

agent=agent,

tools=tools,

verbose=True,

max_iterations=5, # prevents infinite loops

handle_parsing_errors=True,

)

def analyze(query: str) -> str:

result = executor.invoke({"input": query})

return result["output"]

if __name__ == "__main__":

print(analyze("Analyze NVIDIA and compare it to AMD. Should I be watching either?"))

Why gpt-4o-mini: Tool calling works reliably on mini. Using a more powerful model here is unnecessary cost.

Why max_iterations=5: Without this, a bad ticker causes the agent to call the same tool 20+ times.

Step 4: Add a Rate Limit Guard

yfinance and Alpha Vantage both throttle heavy usage. Add a simple backoff wrapper:

# tools/utils.py

import time

import functools

def with_retry(max_attempts: int = 3, delay: float = 1.5):

"""Decorator: retry on transient errors with exponential backoff."""

def decorator(fn):

@functools.wraps(fn)

def wrapper(*args, **kwargs):

for attempt in range(max_attempts):

result = fn(*args, **kwargs)

if "error" not in result:

return result

if attempt < max_attempts - 1:

time.sleep(delay * (2 ** attempt)) # 1.5s, 3s, 6s

return result # return last error after exhausting retries

return wrapper

return decorator

Apply it to your tools:

# Wrap the function body, not the @tool decorator

@tool

def get_current_price(ticker: str) -> dict:

"""Fetch real-time price..."""

return _fetch_price_with_retry(ticker)

@with_retry(max_attempts=3)

def _fetch_price_with_retry(ticker: str) -> dict:

# ... same implementation as before

Why not wrap @tool directly: LangChain's @tool decorator inspects the function signature to build the schema — wrapping it breaks that introspection.

Verification

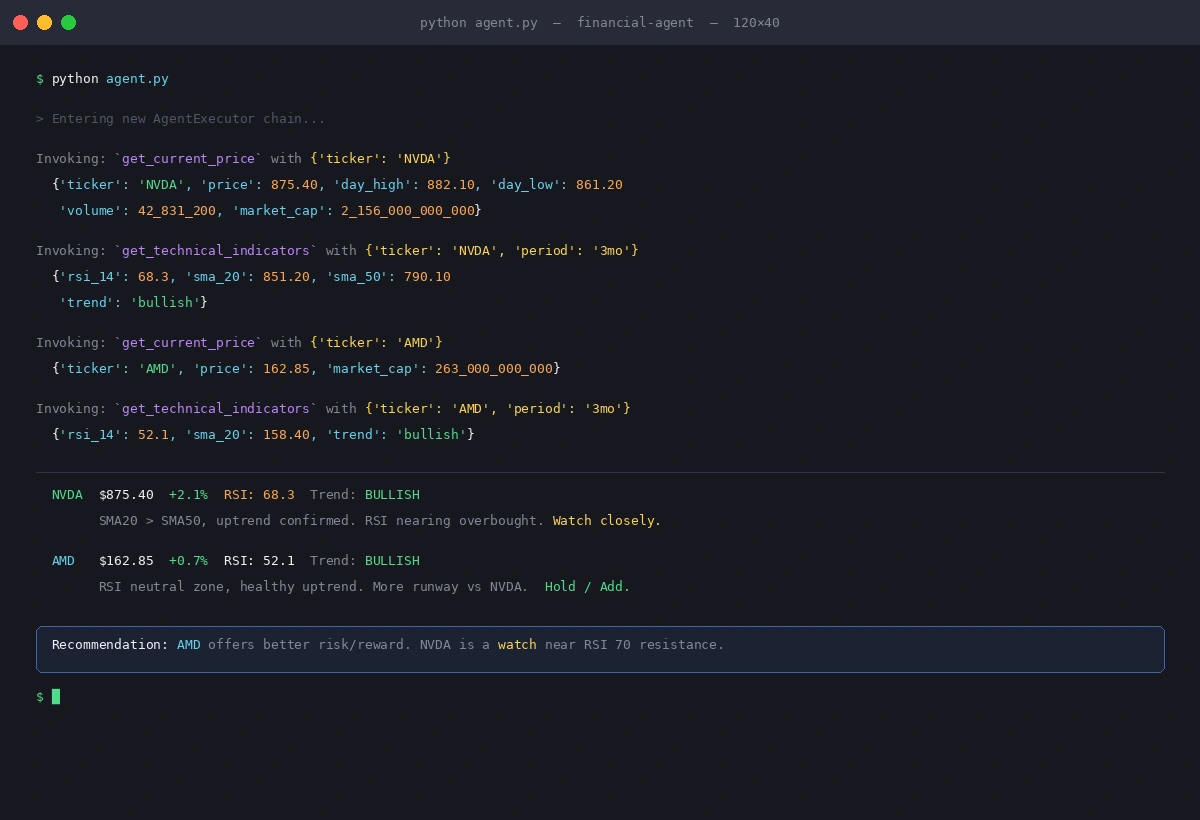

python agent.py

You should see:

> Entering new AgentExecutor chain...

Invoking: `get_current_price` with {'ticker': 'NVDA'}

{'ticker': 'NVDA', 'price': 875.40, 'day_high': 882.10, ...}

Invoking: `get_technical_indicators` with {'ticker': 'NVDA'}

{'rsi_14': 68.3, 'sma_20': 851.2, 'sma_50': 790.1, 'trend': 'bullish'}

...

**NVIDIA Analysis:** Currently trading at $875.40 with an RSI of 68.3...

Clean tool calls with no errors — agent fetches data before reasoning

Clean tool calls with no errors — agent fetches data before reasoning

What You Learned

- Structure tools to return

{"error": ...}instead of raising — agents handle structured errors better than exceptions max_iterationsis non-negotiable in production agents- yfinance's

fast_infois faster but returns fewer fields than.info; choose based on what you need - Low temperature (

0) matters for financial tasks — you want consistent, factual outputs

Limitation: This setup is for analysis, not execution. Adding trade execution requires broker API integration (Alpaca, IBKR) and proper risk controls — that's a separate article.

When NOT to use this: If you're running >100 queries/day, yfinance will get you throttled. Switch to a paid provider (Polygon.io, Twelve Data) for production workloads.

Tested on Python 3.12, LangChain 0.3.x, yfinance 0.2.x, macOS & Ubuntu 24.04