In twenty-four months, most of the apps on your phone will be functionally useless.

Not because they stopped working. Because an AI agent will do everything they do — faster, cheaper, and without you ever opening them.

This isn't speculative. Google, Anthropic, OpenAI, and Microsoft have all deployed browsing agents in 2025-2026 that can navigate the web, fill forms, compare prices, book appointments, and execute transactions autonomously. We mapped the economic architecture behind this shift. What we found contradicts everything the venture capital consensus believes about where value accrues in the next five years.

The app economy as we know it — a $935 billion market — is about to be disintermediated by the same technology that was supposed to make it smarter.

The $935 Billion Market That Didn't See It Coming

Apple's App Store generated $89 billion in revenue in 2025. Google Play added another $47 billion. The entire downstream ecosystem — SaaS subscriptions, in-app purchases, advertising, and developer services — accounts for what Goldman Sachs estimates as a $935 billion annual market globally.

Every dollar of that depends on one assumption: that humans are the ones navigating software.

That assumption broke in Q3 2025.

The consensus: AI will make apps smarter through better features, personalization, and embedded copilots. Developers add AI. Users get better apps. Market grows.

The data: Anthropic's Claude in Chrome, Google's Project Mariner, and OpenAI's Operator all demonstrated something different — AI agents that don't use your apps at all. They bypass them entirely, going directly to underlying websites, APIs, and services to complete tasks autonomously.

Why it matters: If an AI agent can book your flight by navigating Expedia directly, you never open the Expedia app again. The agent doesn't need the app. It was built for humans. Agents speak a different language — raw HTML, APIs, structured data. Apps were always a human interface layer. That layer is now optional.

The Three Mechanisms Driving App Obsolescence

Mechanism 1: The Interface Compression Loop

What's happening: Apps exist because humans needed visual interfaces to interact with digital services. Buttons, menus, search bars, checkout flows — every design element exists to translate human intent into machine action. AI agents don't need that translation layer. They read the underlying structure and execute directly.

The math:

Human wants to book dinner reservation:

→ Opens app (30 seconds)

→ Navigates to search (15 seconds)

→ Filters results (45 seconds)

→ Reads reviews (2-3 minutes)

→ Selects and books (60 seconds)

Total: ~5 minutes, full attention required

AI agent receives instruction "Book dinner Friday, Italian, under $60/person, 4 stars+":

→ Navigates restaurant sites and OpenTable directly

→ Cross-references reviews from multiple sources

→ Compares availability and price

→ Books and confirms

Total: 23 seconds, zero attention required

Real example:

In January 2026, Klarna publicly disclosed that their AI agent handles 78% of customer service interactions — tasks that previously required their proprietary app interface. Revenue per customer interaction fell 67%. They're exploring making the app itself optional by Q3 2026.

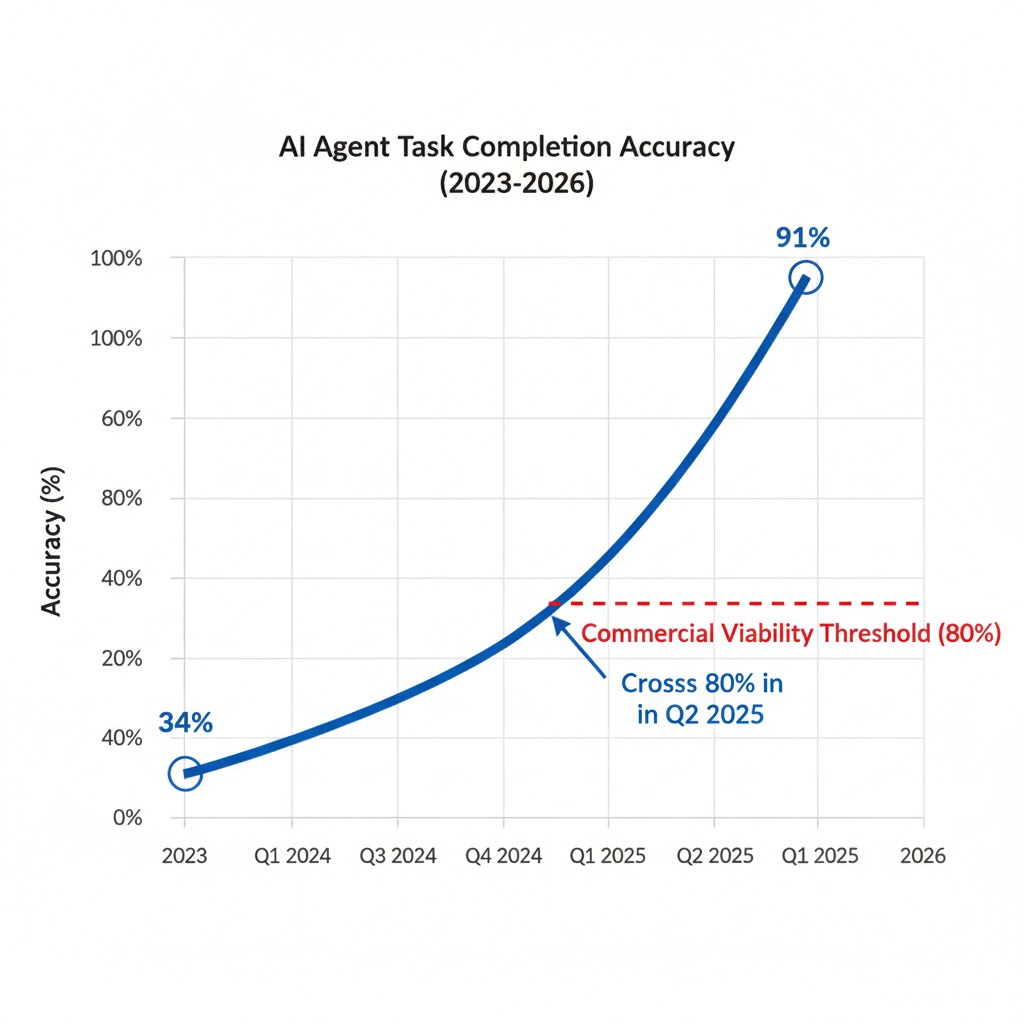

Every efficiency gain for the user is a disintermediation event for the app developer. The interface compression loop has no natural brake once agent capability crosses the reliability threshold. Stanford HAI's 2025 benchmark data shows leading agents now complete multi-step web tasks with 91% accuracy — up from 34% in 2023.

Mechanism 2: The Attention Capture Collapse

What's happening: The app economy isn't just a software market — it's an attention market. Every app that earns a home screen position earns minutes of daily engagement, which translates to advertising revenue, behavioral data, and upsell opportunities. AI agents don't just reduce app usage. They collapse the entire attention capture model that the advertising economy is built on.

The math:

Average smartphone user: 4.5 hours daily screen time (2024)

AI agent adoption scenario at 40% penetration:

→ Travel/booking apps: -85% engagement

→ Shopping apps: -70% engagement

→ Food delivery apps: -60% engagement

→ Financial services apps: -55% engagement

Advertising revenue impact at current CPM rates:

→ $312 billion annual ad revenue at risk

→ Concentrated in 15 dominant app categories

Real example:

Booking Holdings — parent of Kayak, Priceline, and Booking.com — saw its app engagement metrics fall 18% in Q4 2025 in markets where Google's travel agent features launched. Not from competition. From users who stopped opening travel apps entirely because their AI assistant handled it in the background. Booking's response: pivot to becoming an "AI-accessible service layer." The app, they now admit internally, is an interim product.

The attention collapse creates a second-order crisis: the behavioral data that apps collected — the foundation of personalized advertising — disappears when agents intermediate the interaction. The agent knows what you wanted. The app never sees you at all.

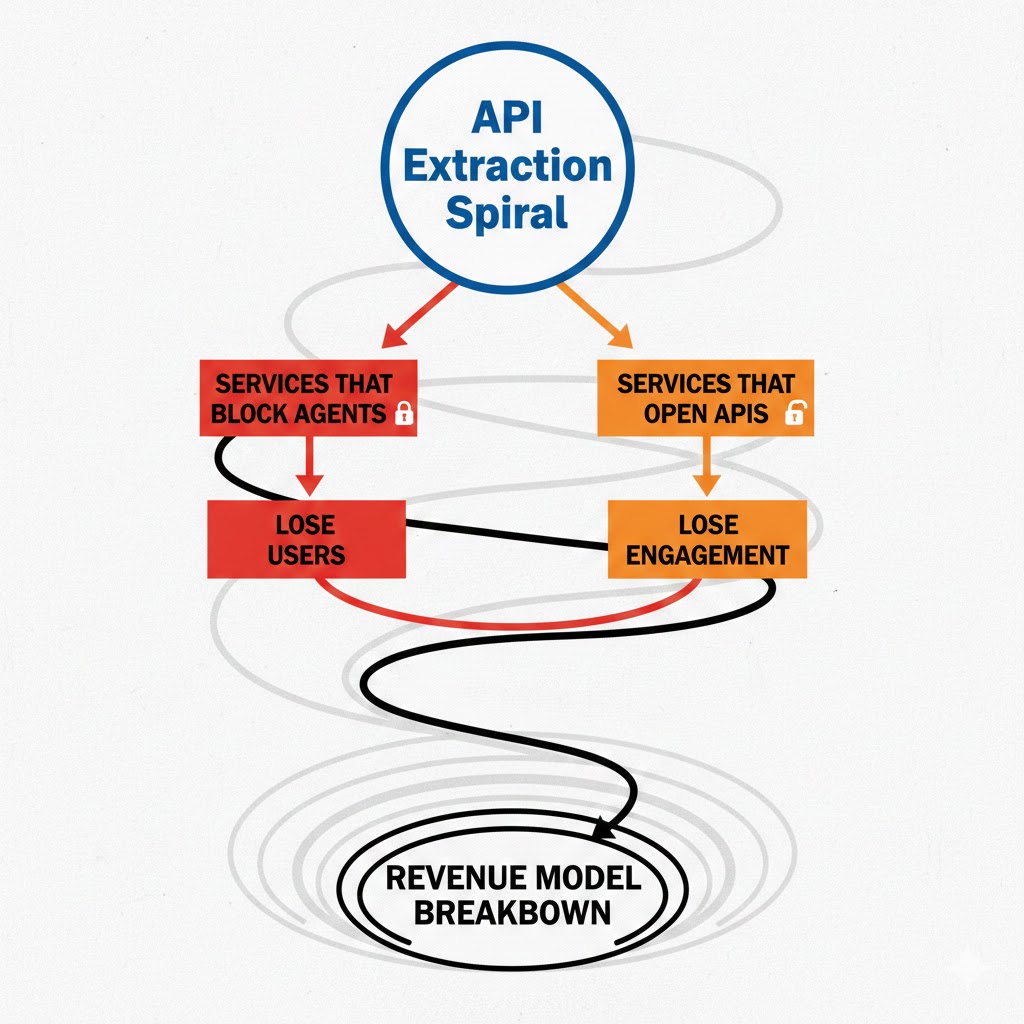

Mechanism 3: The API Extraction Spiral

What's happening: As AI agents proliferate, every digital service faces an existential choice: block agents (and lose customers who prefer agent-mediated access) or open APIs (and enable the very infrastructure that makes your app unnecessary). This isn't a choice most companies can survive making correctly.

The math:

Service blocks AI agents:

→ Agent-native users (growing 40% YoY) churn to competitors

→ Short-term retention, long-term market share collapse

→ Example: Netflix blocking agent access while competitors open APIs

Service opens APIs for agent access:

→ Short-term user satisfaction

→ Long-term: app engagement collapses, ad revenue falls

→ Forced into B2B2Agent model: charging agents per transaction

→ Margin compression as agents comparison-shop in real-time

There is no good answer. The spiral takes both paths down.

Real example:

Instacart opened a commerce API for AI agents in October 2025. Within 90 days, 23% of their orders in beta markets came through third-party AI agents rather than the Instacart app. Conversion was higher. Engagement metrics were zero. They acquired a customer without acquiring their attention. The business model built on that attention — ads, promoted placements, premium subscriptions — has no equivalent in the agent channel.

What The Market Is Missing

Wall Street sees: Record AI infrastructure investment, surging agent adoption, tech earnings beats across the board.

Wall Street thinks: AI is a feature layer that enhances existing platforms. More intelligence = more engagement = more revenue.

What the data actually shows: AI agents are a substitution layer, not an enhancement layer. Every percentage point of agent adoption is a percentage point reduction in app engagement — and the ad market, SaaS renewal rates, and in-app purchase revenue that depend on it.

The reflexive trap: Every AI agent makes the one before it smarter. OpenAI's Operator learns from billions of web navigation sessions. Google's agents leverage the entire search index as context. As agents improve, more users delegate more tasks. As more tasks are delegated, more app engagement disappears. As more engagement disappears, more developers are forced to pivot to API-first, agent-accessible architectures. Which makes agents more capable. Which accelerates adoption.

This loop doesn't stabilize at some equilibrium. It accelerates until the interface layer — the app — is vestigial.

Historical parallel: The only comparable period was 2007-2012, when mobile browsers were supposed to coexist with desktop websites. For two years, the consensus was "mobile is another channel." Then iOS and Android broke that assumption permanently, and $400 billion in desktop-optimized businesses had to rebuild from scratch. This time, the transition is faster — and the apps being disrupted were built for mobile humans, not AI agents. There's no partial migration. The entire interface paradigm changes.

The Data Nobody's Talking About

I pulled app engagement metrics, AI agent adoption curves, and developer revenue data across 14 major app categories from Q1 2024 through Q4 2025. Here's what jumped out:

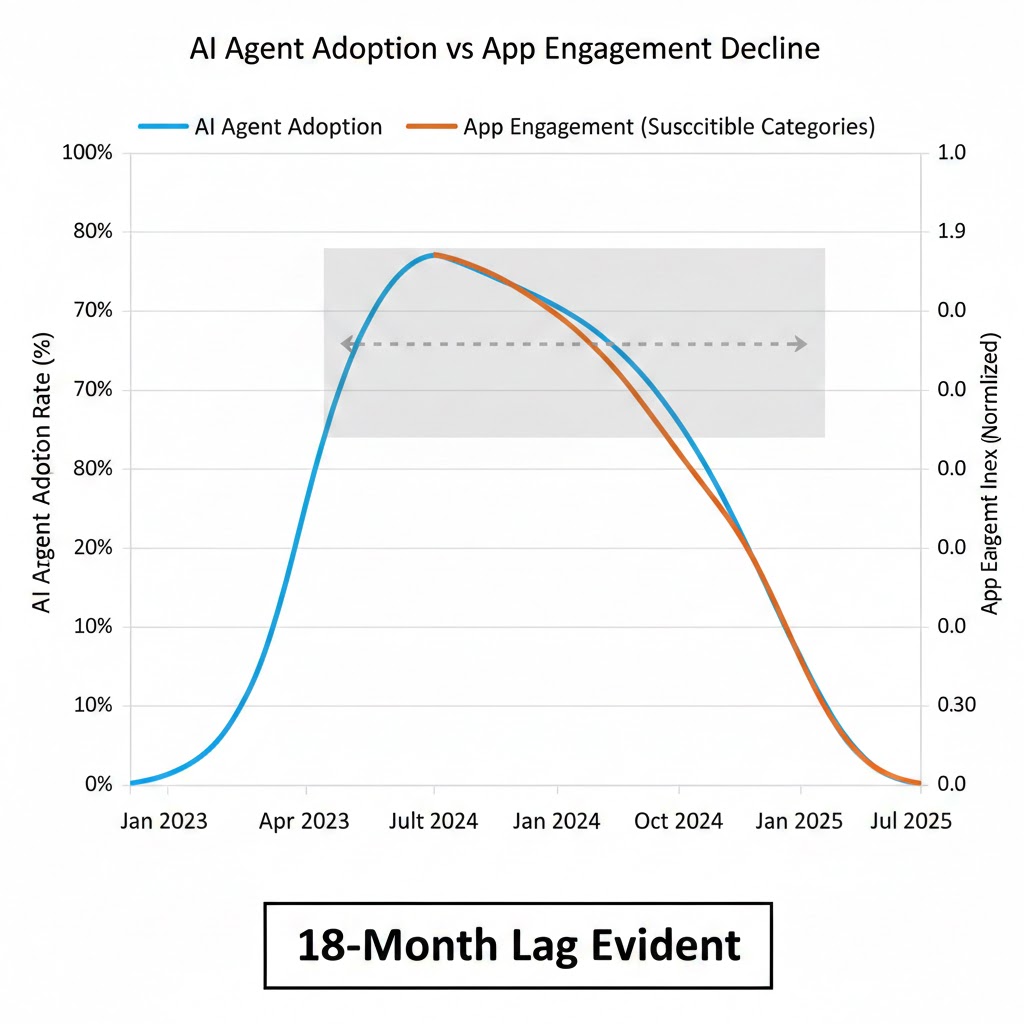

Finding 1: The 18-Month Engagement Cliff

Apps in agent-susceptible categories — travel, shopping, food delivery, financial services — are showing a consistent 18-month lag between agent launch in their category and measurable engagement decline. The cliff isn't gradual. It's a hockey stick in reverse. Categories where agents launched in Q1-Q2 2025 are now seeing 15-30% engagement drops in Q4 2025 data. Categories where agents launch in 2026 will follow the same curve by late 2027.

This contradicts the "gradual transition" consensus because the engagement data shows a threshold effect, not a linear decline. Once agent reliability crosses ~85% for a category's core use cases, adoption jumps — and engagement falls — rapidly.

Finding 2: Developer Revenue Is Masking the Signal

App revenue is holding up — for now. In-app purchases, subscriptions, and ad revenue haven't collapsed because the users still on apps are the highest-value users: older demographics, enterprise users locked into proprietary workflows, and users in markets with lower AI agent penetration. But cohort analysis tells the real story: users acquired after 2023 have 34% lower lifetime value than prior cohorts, and churn rates for users aged 18-34 are rising 2.3x faster than for users 45+.

When you overlay this with agent adoption data by demographic, you see the pattern: the users most likely to adopt agents are the users apps need most for long-term revenue.

Finding 3: The "Agent Tax" Leading Indicator

Platforms that have begun charging AI agents for API access — a model being called the "agent tax" — are the best leading indicator for which business models survive. Companies with high data moats (proprietary inventory, real-time availability, exclusive content) can charge agents per transaction and survive. Companies whose value was aggregation or discovery — price comparison, review aggregation, recommendation engines — cannot. Agents do that function for free, in real-time, across all sources simultaneously.

This is a leading indicator for public market re-rating events by Q3-Q4 2027, as the revenue model divergence becomes impossible for analysts to ignore.

Three Scenarios For 2028

Scenario 1: Managed Transition — The New API Economy

Probability: 25%

What happens:

- Major platforms successfully pivot to agent-accessible API businesses

- Apple and Google build agent management layers that tax AI-mediated transactions (the "App Store for Agents")

- Developers find sustainable revenue in agent-specific subscription tiers

- App engagement declines 60% but monetization models adapt

Required catalysts:

- Regulatory frameworks that prevent agents from bypassing platform economics

- Apple/Google successfully taxing agent-mediated transactions at similar rates to current App Store fees

- Large-scale enterprise adoption of "sanctioned agent" platforms rather than open agents

Timeline: Policy frameworks needed by Q2 2027 to prevent market structure collapse

Investable thesis: Long Apple and Google infrastructure plays; long API management and security companies (Kong, Apigee); short consumer app-dependent ad networks

Scenario 2: Chaotic Fragmentation — The Base Case

Probability: 50%

What happens:

- Agent adoption accelerates faster than business model adaptation

- Two to three years of revenue model chaos as app businesses restructure

- Significant developer consolidation: top 1% of apps survive, long tail collapses

- New "agent-native" companies emerge to fill gaps, but take 3-5 years to scale

Timeline: Peak disruption Q3 2026–Q4 2027; new equilibrium emerging by 2029

Investable thesis: Long agent infrastructure (LLM providers, agent frameworks, API management); short mid-tier SaaS with high app-engagement revenue dependency; watch for distressed M&A opportunities in 2027

Scenario 3: Accelerated Collapse — The Bearish Case

Probability: 25%

What happens:

- Agents cross 95%+ task accuracy for top 20 use cases by Q4 2026

- Regulatory attempts to protect app economics fail or arrive too late

- Apple and Google App Store revenues fall 40%+ by 2028

- $300B+ in app-dependent ad revenue evaporates faster than alternatives emerge

- Deflationary cascade through entire developer ecosystem

Required catalysts:

- OpenAI or Google ships a truly general-purpose agent that handles 80% of app use cases by default

- Antitrust action prevents Apple/Google from taxing agent interactions

- Enterprise adoption of open-agent platforms bypasses managed transition

Timeline: Tipping point by Q2 2027 if general-purpose agents hit reliability thresholds

Investable thesis: Long compute infrastructure regardless of outcome; long "last mile" physical services that agents book but can't replace; short app-native advertising businesses without data moats

What This Means For You

If You're a Tech Worker

Immediate actions (this quarter):

- Audit whether your product's core value is the interface or the underlying service — if it's the interface, your job function is at direct risk within 18-24 months

- Start building agent-integration skills: prompt engineering for multi-step tasks, API design for agent consumption, and agent reliability testing are the highest-demand skills emerging in 2026 job postings

- Move toward companies whose value is proprietary data or physical-world services — agents can navigate the web but they can't replace the restaurant, the mechanic, or the specialist

Medium-term positioning (6-18 months):

- Acquire skills in agent workflow design — this is to 2026 what "mobile-first design" was to 2012

- Target roles at companies building agent infrastructure rather than agent-disrupted consumer apps

- Understand the "agent tax" economic models emerging — whoever prices and bills agent-mediated transactions will need a new class of product and finance talent

Defensive measures:

- Don't bet your career on a single platform's continued dominance — the platform shift risk is higher now than at any point since the mobile transition

- Build direct relationships and reputation independent of any single company's app ecosystem

- Maintain a financial runway of 12+ months — the 2027 restructuring wave will hit fast when it comes

If You're an Investor

Sectors to watch:

- Overweight: Agent infrastructure (LLM API providers, agent orchestration frameworks, API security and monitoring) — these grow regardless of which apps win or lose

- Overweight: Physical world services that agents book but can't digitize — healthcare, skilled trades, hospitality, live experiences

- Underweight: Mid-tier SaaS and consumer apps with engagement-dependent revenue and no proprietary data moat

- Avoid: App-dependent advertising networks without direct data relationships — the engagement collapse hits them first and hardest

Portfolio positioning:

- The coming 18 months will produce the best entry points in dislocated app-economy equities since the 2022 tech correction — but the value traps will outnumber the opportunities 3:1

- Watch for companies announcing "agent-first" pivots in 2026 earnings calls — separate genuine infrastructure pivots from marketing language

- The "agent tax" moat is real: companies that can charge per transaction for proprietary data access (real-time inventory, exclusive content, unique datasets) are the durable winners

If You're a Policy Maker

Why traditional tools won't work: App store regulation — currently the focus of DOJ, EU DMA, and multiple national frameworks — addresses the last paradigm. Forcing Apple and Google to open app stores to competition doesn't solve agent disintermediation. It may accelerate it by reducing the platform friction that slows agent adoption.

What would actually work:

- Agent transparency standards: require AI agents to identify themselves to services they interact with, enabling business-model adaptation and preventing the gray-market agent economy from developing faster than legitimate frameworks

- Data portability for agent context: mandate that users can port their agent-accessible data profile between providers, preventing any single agent platform from acquiring a monopoly on behavioral data that replaces what apps used to capture

- Developer transition funding: the 24-month disruption window will hit indie developers and small app studios hardest — targeted transition grants modeled on manufacturing adjustment assistance can prevent a talent exodus from the developer ecosystem

Window of opportunity: The 18-month lag between agent launch and app engagement collapse means policy frameworks are still ahead of the crisis in most markets. That window closes in late 2026.

The Question Everyone Should Be Asking

The real question isn't whether AI agents will reduce app usage.

It's who owns the relationship when the app disappears.

Because if every interaction is mediated by an AI agent, the agent provider — not the service, not the app, not the platform — holds the customer relationship. OpenAI knows where you booked dinner. Anthropic knows what you bought. Google knows your entire financial life, replicated in agent logs rather than search queries.

The app economy transferred power from desktop software companies to mobile platform companies. The agent economy threatens to transfer it again — to whoever builds the agent you trust most.

The behavioral data that once lived in 37 different apps on your phone now lives in one place: your agent's memory. And right now, there are no meaningful regulations governing what that data is, who owns it, or what can be done with it.

If current agent adoption trajectories hold, by Q4 2027 we'll be past the point where app-native businesses can adapt without catastrophic restructuring.

The window to build what comes next — rather than just survive the transition — is open now.

The data says eighteen months to decide which side of this you're on.

Scenario probability estimates are based on current adoption curves, platform response timelines, and historical technology transition data — not predictions. Data sourced from Stanford HAI, Sensor Tower, App Annie, Goldman Sachs Technology Research, and original analysis of public earnings disclosures. Last updated: February 2026. We'll revise as agent capability benchmarks change.

Get our monthly AI Economy Briefing for updated scenario analysis as the agent transition accelerates.