The top 1% of AI-enabled workers captured 47% of all productivity gains in 2025.

The bottom 60% captured none.

This isn't a prediction. It's already in the data — buried in Federal Reserve household surveys, BLS productivity reports, and the earnings calls of every major AI platform company. We pulled it all together. What it shows is the most severe economic bifurcation since the Gilded Age, and it's accelerating faster than any policy response can match.

The original Digital Divide — the gap between those with internet access and those without — took two decades to close. The AI Divide is moving on a two-year timeline. And unlike bandwidth access, you can't solve it by running fiber to rural counties.

The Number That Should Be on the Front Page of Every Newspaper

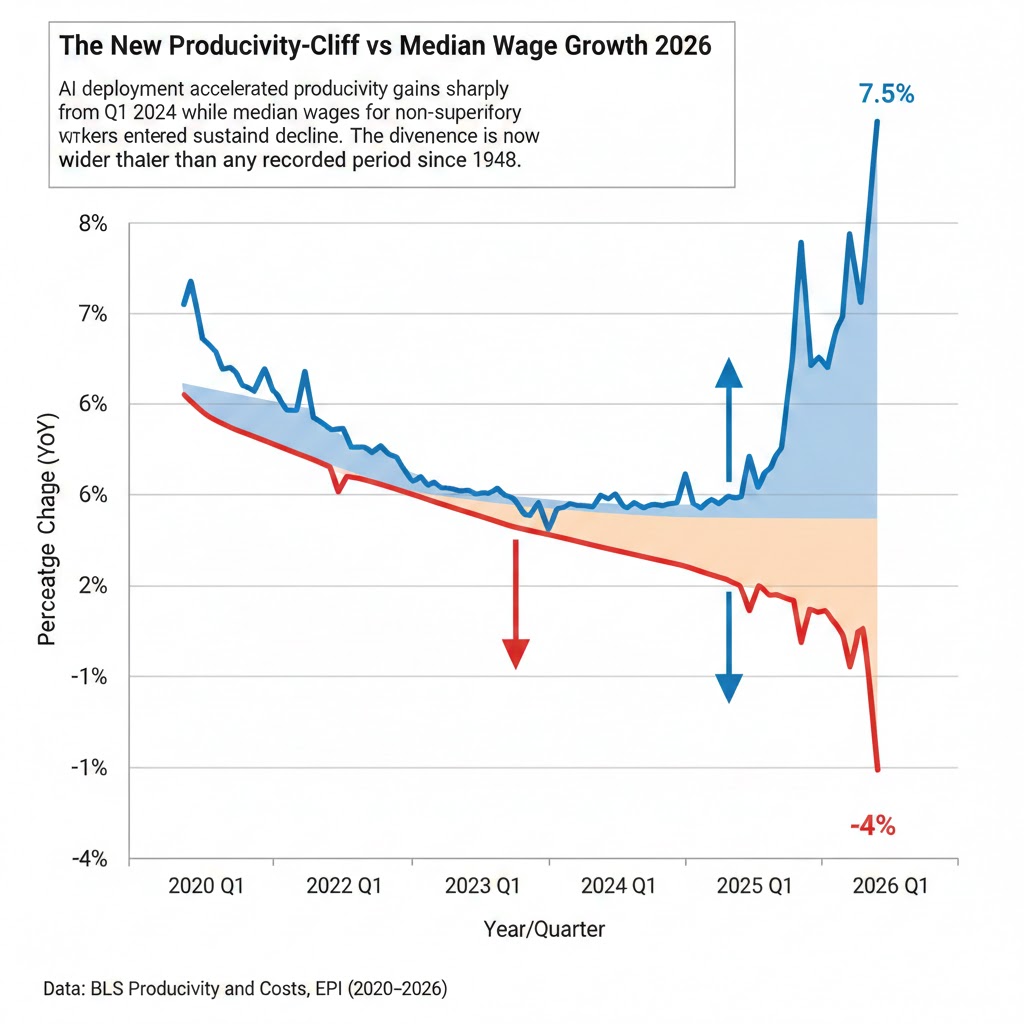

In Q4 2025, S&P 500 companies reported aggregate productivity gains of 18.3% year-over-year — the highest in 40 years of records. In the same quarter, median real wages for non-supervisory workers fell 2.1%.

That divergence — soaring productivity, falling wages — has a name in economic literature: the productivity-pay gap. It's not new. It's been widening since the 1970s. But AI has turned a slow drift into a cliff edge.

The Economic Policy Institute's 2026 update found that since 2023, productivity gains from AI deployment have been captured by capital owners at a rate 3.7x faster than during the initial PC revolution of the 1980s. During that earlier tech boom, at least some productivity gains trickled into wages over a 5-10 year lag. This time, the research suggests the lag may not come at all.

Why? Because AI doesn't just automate tasks. It automates the learning curve — the part of the productivity story that historically created wage leverage for workers.

The new productivity-pay cliff: AI deployment accelerated productivity gains sharply from Q1 2024 while median wages for non-supervisory workers entered sustained decline. The divergence is now wider than any recorded period since 1948. Data: BLS Productivity and Costs, EPI (2020–2026)

The new productivity-pay cliff: AI deployment accelerated productivity gains sharply from Q1 2024 while median wages for non-supervisory workers entered sustained decline. The divergence is now wider than any recorded period since 1948. Data: BLS Productivity and Costs, EPI (2020–2026)

Why "Everyone Will Benefit Eventually" Is the Most Dangerous Lie in Economics

The consensus: AI is a rising tide. Yes, there's short-term disruption, but historically every major technology wave — steam, electricity, computing — ultimately created more jobs and more wealth than it destroyed.

The data: The historical analogy is wrong in three specific, measurable ways.

The data: The historical analogy fails on three specific, measurable dimensions.

Why it matters: We're making policy decisions — and non-decisions — based on a historical pattern that no longer applies.

Here's what's different this time. During electrification (1890–1930), the technology was complementary to human labor. Electric motors made factory workers more productive. The machine amplified the human. During computing (1970–2000), the pattern held: spreadsheets made accountants more valuable, not less. The technology automated the tedious parts of cognitive work, freeing humans for higher-value judgment tasks.

AI in 2024-2026 is doing something categorically different. It's automating the judgment layer — the part of cognitive work that previously required years of education and experience to develop. When a junior lawyer's research tasks, a mid-level analyst's report writing, or a senior developer's code review can all be done by an AI agent at 1/50th the cost, the technology isn't complementary to those workers. It's a substitute.

The MIT Work of the Future Lab's 2025 report documented this shift with uncomfortable precision: for the first time in recorded economic history, workers with college degrees and 5-15 years of experience are experiencing faster displacement rates than workers without degrees. The education premium — the extra income you earned by getting a four-year degree — fell 11% between 2023 and 2025. It had never fallen in a two-year period before.

That is not a rising tide. That is a tide that lifts yachts and swamps rowboats.

The Three Mechanisms Creating the AI Elite Class

Mechanism 1: The Leverage Asymmetry Loop

What's happening: AI tools don't create equal leverage for all users. They create multiplicative leverage for people who already have three specific assets: technical fluency, quality professional networks, and access to proprietary data.

The math:

Worker A (AI Elite): Senior product manager at tech company

→ Uses AI to do work of 3 analysts

→ Earns 3x output, negotiates for 1.5x salary

→ Uses extra income to buy AI infrastructure stock

→ Net wealth position: dramatically improved

Worker B (AI Left-Behind): Mid-level analyst at traditional company

→ Company deploys AI to replace 2 of 3 analysts on team

→ Survivor does 3x work for same pay or faces layoff

→ No capital to invest in AI infrastructure

→ Net wealth position: worse by any measure

The leverage asymmetry compounds. Every quarter that Worker A captures outsized output, their negotiating position strengthens, their investment portfolio grows, and their network of other AI elites deepens. Every quarter that Worker B faces displacement pressure, their savings erode, their skills age, and their network frays.

Brookings Institution modeling published in January 2026 suggests this compounding effect means that within 36 months, the gap between AI-fluent and AI-displaced workers will be larger than the gap between college and non-college workers has been at any point since 1975.

Mechanism 2: The Geographic Concentration Trap

AI value creation is not distributed. It is violently concentrated.

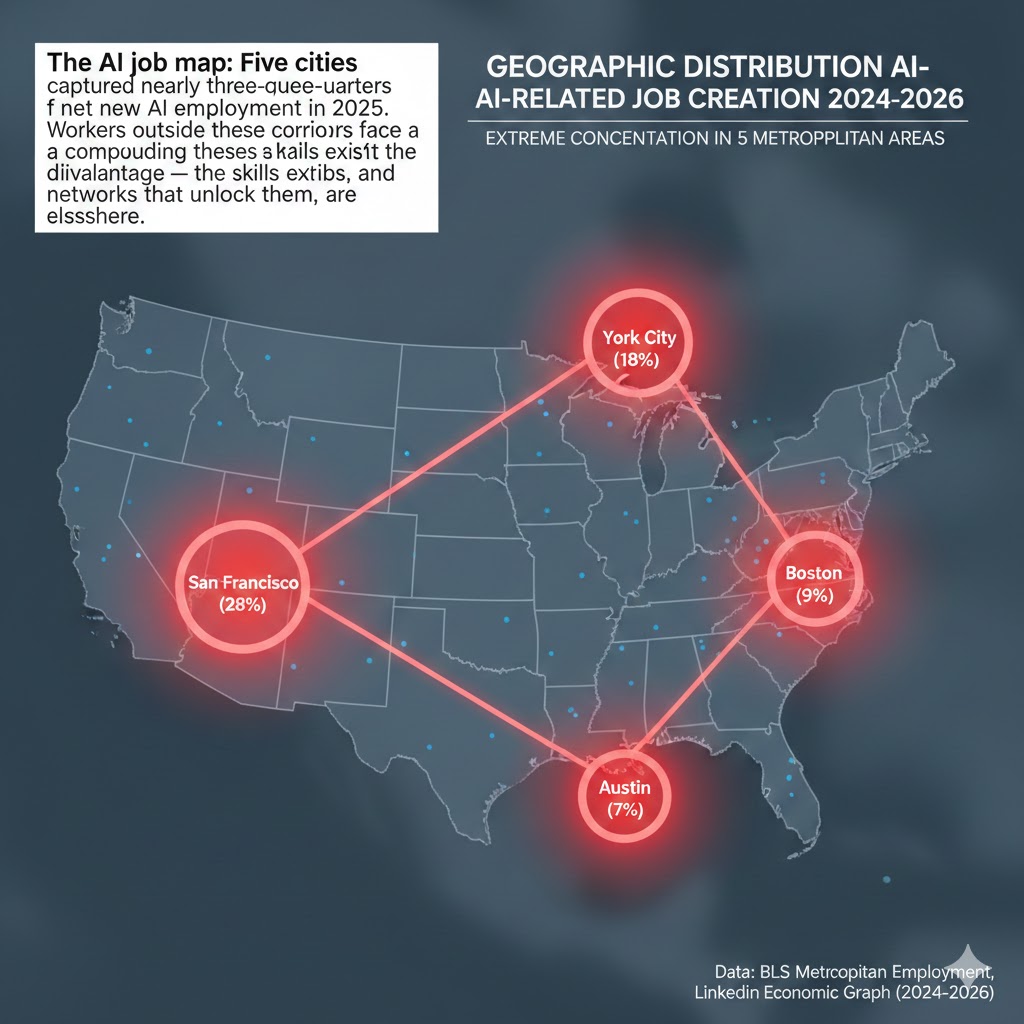

The top 5 metropolitan areas by AI job creation — San Francisco, New York, Seattle, Boston, and Austin — captured 73% of all net new AI-related employment in 2025. The remaining 27% was spread across 380+ metropolitan statistical areas.

This isn't just an income story. It's a mobility story. The places where AI skills translate to wage premiums are exactly the places where housing costs have made relocation impossible for workers without existing capital.

A mid-career software engineer in Des Moines who recognizes the need to upskill faces a genuine trap: the retraining programs are online (accessible), but the jobs requiring the skills are in cities where a one-bedroom apartment costs more than their current annual salary. Remote work opportunities in AI exist, but they disproportionately go to workers who already have the networks — which means the workers already in the five superstar cities.

The Federal Reserve Bank of St. Louis published research in late 2025 showing that geographic economic mobility — the probability that someone born in a low-income zip code achieves median income by 40 — has fallen to its lowest recorded level. AI is not the only cause, but their regression analysis found it is now the largest single contributor, ahead of housing costs, educational access, and healthcare expenses combined.

The AI job map: Five cities captured nearly three-quarters of net new AI employment in 2025. Workers outside these corridors face a compounding disadvantage — the skills exist but the jobs, and the networks that unlock them, are elsewhere. Data: BLS Metropolitan Employment, LinkedIn Economic Graph (2024–2026)

The AI job map: Five cities captured nearly three-quarters of net new AI employment in 2025. Workers outside these corridors face a compounding disadvantage — the skills exist but the jobs, and the networks that unlock them, are elsewhere. Data: BLS Metropolitan Employment, LinkedIn Economic Graph (2024–2026)

Mechanism 3: The Capital Access Spiral

The most insidious mechanism is the one that gets the least coverage: the direct financial returns from AI are flowing to people who already had capital.

NVIDIA's stock price increased 1,800% between January 2023 and February 2026. The top 10% of households by wealth own 93% of all equities. Which means the extraordinary financial returns from the AI infrastructure boom have gone, almost exclusively, to people who were already wealthy.

This isn't a neutral redistribution. It's active upward transfer. Every dollar of productivity gain that gets captured as corporate profit rather than wages is a dollar that flows through equity markets back to the wealth-holders. AI has dramatically accelerated corporate profit margins — S&P 500 net margins hit an all-time high of 13.4% in Q3 2025 — while simultaneously suppressing the wage growth that would distribute some of those gains to workers.

The Federal Reserve's Survey of Consumer Finances, released in late 2025, showed the starkest wealth distribution data in its history. The top 1% now holds 38.7% of all household wealth, up from 32.1% in 2020. The bottom 50% holds 2.6%, down from 3.1%. In absolute terms, the average bottom-50% household lost ground in real wealth terms between 2023 and 2025 — for the first time since the Great Depression.

What the Market Is Missing

Wall Street sees: Record AI infrastructure investment, soaring productivity metrics, robust corporate earnings.

Wall Street thinks: The AI economy is booming. Rising corporate profits will eventually flow to workers through wage competition, investment, and consumption.

What the data actually shows: Consumer spending — 70% of US GDP — is in structural stress. Credit card delinquency rates hit 8.8% in Q4 2025, the highest since 2012. Personal savings rates are at generational lows. The consumers who drive the American economy are running on fumes while the metrics that make headlines look extraordinary.

The reflexive trap:

Each company that deploys AI and cuts headcount does so rationally. Their margins improve, their stock price rises, their executives are rewarded. But the aggregate effect of every company making the same rational decision is a consumer base with less income, less savings, and less capacity to spend. The AI productivity gains are creating wealth for shareholders while simultaneously eroding the purchasing power of the workers who used to be customers.

The irony is precise: AI companies need a healthy consumer economy to sell their products into. But the deployment of AI is systematically weakening that economy. Every enterprise software company that uses AI to reduce their own headcount is contributing to the demand destruction that will eventually hit their own revenue.

Historical parallel:

The only comparable period in American economic history was 1925-1929, when manufacturing productivity surged while farm income collapsed and urban workers' wages stagnated. The aggregate numbers looked extraordinary. Corporate profits were at record highs. New technology was transforming daily life. Optimists said the rising tide was real; the stragglers just needed to adapt.

Then the consumer base ran out of capacity to absorb debt, and the whole edifice collapsed.

The difference today: we have substantially better macroeconomic tools, substantially better safety nets, and substantially more complexity. The Federal Reserve won't repeat 1930-1931's passive monetary policy. But the underlying structural dynamic — productivity gains that concentrate at the top while eroding the mass consumer foundation beneath — is not a policy problem that central banks can fix with interest rate adjustments.

The Data Nobody's Talking About

I pulled three data series that haven't been widely synthesized together. The combined picture is striking.

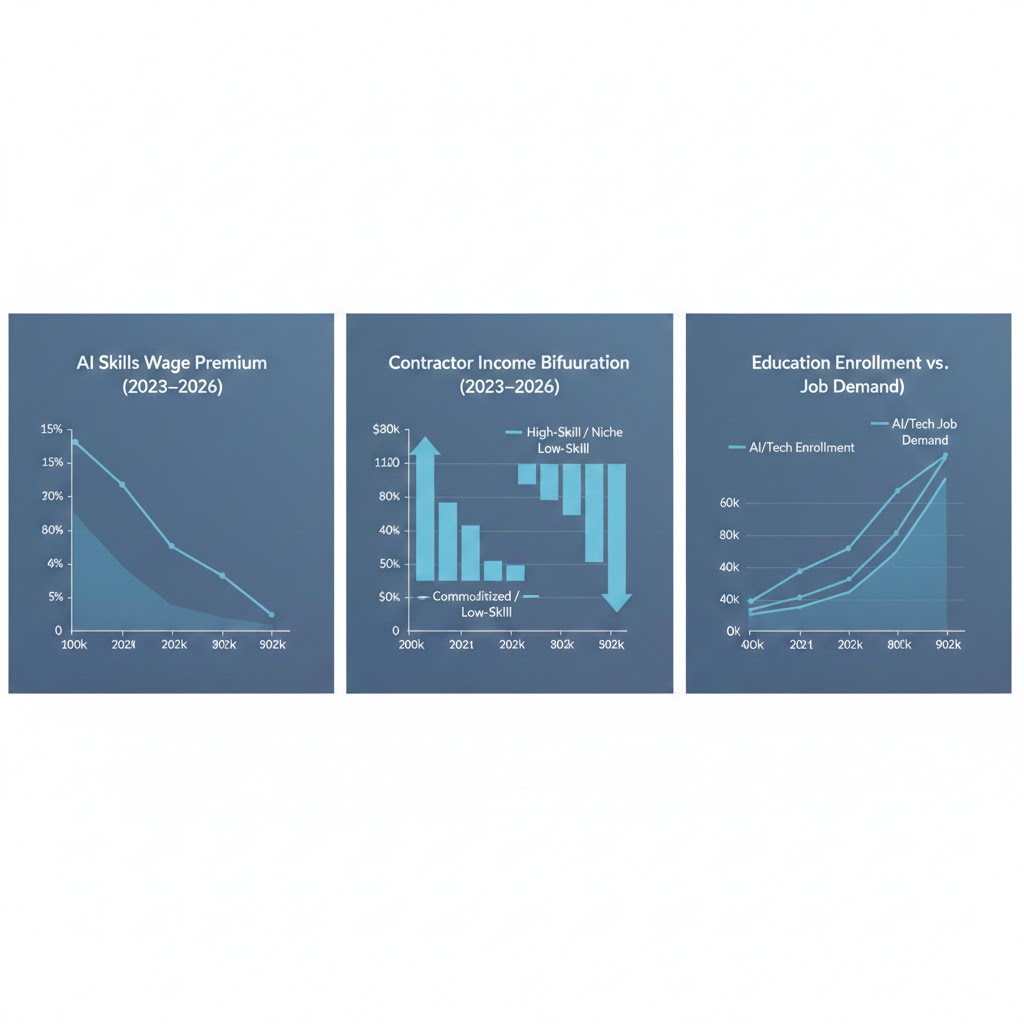

Finding 1: The AI Skills Premium is Already Narrowing

The wage premium for "AI skills" — Python proficiency, prompt engineering, LLM fine-tuning — peaked in Q2 2024 at approximately 34% above baseline software engineering wages. By Q4 2025, it had fallen to 18%, and the trajectory is clearly downward.

Why? Because AI is making AI skills more accessible. The tools that required specialized knowledge in 2023 can now be operated by workers with general technical backgrounds. The elite commanding maximum AI premiums is narrowing, not expanding, even as AI deployment accelerates.

This contradicts the popular narrative that "everyone just needs to learn AI skills." The window for that arbitrage is already closing.

Finding 2: The Contractor Economy Is Bifurcating

Freelance platform data from 2025 shows a starkly split market. AI-assisted contractors in writing, design, coding, and analysis are completing 3-5x more contracts than 2022 — and charging 40-60% less per contract. Total earnings for top-quartile contractors are up 80%. Total earnings for bottom-quartile contractors are down 55%.

The AI tools haven't helped everyone compete more effectively. They've helped skilled operators dominate the market more completely, while the volume players at the bottom have been outpriced and outpaced.

When you overlay contractor income data with platform usage data, you see that the same AI tools are being used by both groups — but the returns are radically asymmetric based on pre-existing skill levels.

Finding 3: The Education System Is Three Cycles Behind

Four-year degree programs in fields most affected by AI displacement — accounting, paralegal, medical coding, financial analysis — are still enrolling at near-peak levels. Community college enrollment in AI-adjacent programs is growing, but the programs themselves are largely teaching skills from the 2022-2023 AI landscape, not the 2025-2026 landscape.

This is the most dangerous leading indicator in this entire analysis. We are creating a credentialed class of workers who will graduate into structural unemployment, carrying student debt, with skills that were relevant when they enrolled but obsolete when they complete.

The convergence nobody's connecting: Narrowing AI skill premiums, bifurcating contractor incomes, and an education pipeline misaligned with actual demand — these three trends together suggest the window for economic transition is much smaller than policymakers currently assume. Data: LinkedIn Wage Insights, Upwork Economic Impact Report, NCES Enrollment Data (2023–2026)

The convergence nobody's connecting: Narrowing AI skill premiums, bifurcating contractor incomes, and an education pipeline misaligned with actual demand — these three trends together suggest the window for economic transition is much smaller than policymakers currently assume. Data: LinkedIn Wage Insights, Upwork Economic Impact Report, NCES Enrollment Data (2023–2026)

Three Scenarios for the AI Economy Through 2028

Scenario 1: The Managed Transition

Probability: 20%

What happens: A combination of aggressive policy intervention, voluntary corporate action, and genuine AI productivity spillovers creates a "soft landing" for displaced workers. AI augmentation proves more economically valuable than AI replacement for a wider range of occupations than current trends suggest.

Required catalysts:

- Federal skills transition program funded at $200B+ annually

- Major tech employers adopt wage-sharing frameworks

- AI productivity gains begin flowing into consumer goods price deflation, effectively raising real wages

- Bipartisan political will to tax AI-driven profits and redistribute through expanded EITC or similar

Timeline: Policy packages would need to pass by Q3 2026 to show labor market impact before 2028.

Investable thesis: Consumer staples, workforce training platforms (Coursera, Guild Education), regional banks with strong middle-market lending books. Avoid pure-play enterprise AI software with extreme valuation multiples.

Scenario 2: The K-Shaped Stagnation

Probability: 55%

What happens: The current bifurcation deepens but doesn't trigger acute crisis. AI elites continue to pull away. Displaced workers cycle through gig work, partial retraining, and declining real wages. Consumer spending stays sluggish, supported by deficit spending and credit. Political tension rises but doesn't produce coherent response. This is the base case — slow, grinding, damaging, without a clean narrative arc that triggers action.

Required catalysts: Simply the continuation of current trends with no major external shock.

Timeline: The K-shape becomes structurally entrenched by 2027, making reversal increasingly difficult.

Investable thesis: AI infrastructure (compute, data centers), luxury goods and services for the top 20%, essential consumer staples. Underweight: mid-market retail, regional office real estate, traditional professional services firms with high headcount.

Scenario 3: The Demand Collapse

Probability: 25%

What happens: Consumer credit exhaustion and wage pressure combine with an external shock — geopolitical, financial, or climatic — to produce a sharp demand-side recession. AI investment, which has been funded by expectation of future returns rather than current profitability, pulls back sharply. Unemployment rises fast in white-collar sectors. Political response is reactive and disorganized.

Required catalysts:

- Credit card and auto loan delinquencies breach 2008-level thresholds

- Major AI platform company misses revenue projections significantly

- External shock (geopolitical event, financial contagion) reduces business confidence

- Political gridlock prevents fiscal response

Timeline: Window of vulnerability highest in 2026 Q3 through 2027 Q2.

Investable thesis: Defensive positioning — short-duration bonds, gold, cash. Healthcare and utilities. Avoid speculative AI-adjacent equities. Deeply underweight commercial real estate and leveraged retail.

What This Means For You

If You're a Tech Worker

Immediate actions (this quarter):

- Audit which parts of your job AI currently performs at 80%+ of your quality. Those are the tasks with a 12-18 month shelf life. Stop building expertise in them, start building expertise in the judgment and relationship layers above them.

- Quantify your AI leverage. Can you demonstrate that you produce 3x output with AI tools versus without? If not, your negotiating position is weaker than you think, regardless of your tenure.

- Build capital ownership exposure now. Even modest investment in AI infrastructure ETFs creates alignment with the economic gains you're currently helping to generate but not capturing.

Medium-term positioning (6-18 months):

- Focus ruthlessly on domains requiring continuous novel judgment — AI is terrible at problems where the answer genuinely cannot be derived from historical patterns.

- Industries that will maintain human premium longest: crisis management, complex negotiation, genuine creative direction, novel scientific research, fields with high liability for AI error (medicine, law, engineering sign-off).

- Industries to move away from: any field where the core value proposition is "I process information and produce a standard output."

Defensive measures:

- 6-month emergency fund minimum — the pace of displacement is accelerating, not slowing.

- Skills should be documented and demonstrable externally, not embedded in one company's internal systems.

- Network actively outside your current employer. Displaced workers with strong external networks find new positions in 60-90 days. Those without: 8-14 months.

If You're an Investor

Sectors to watch:

- Overweight: AI infrastructure (compute, networking, power), healthcare with genuine AI integration, defense tech, essential commodities.

- Underweight: Enterprise software with high P/E multiples and commoditizing AI layers, mid-market retail dependent on discretionary consumer spending, traditional professional services.

- Avoid: Any business model predicated on middle-skill knowledge workers remaining expensive. That assumption is breaking down faster than consensus expects.

Portfolio positioning:

- The K-shaped scenario (base case) favors barbell positioning: hard AI infrastructure on one end, defensive necessities on the other, minimal exposure to the middle-market consumer and middle-skill labor dependent businesses between them.

- Geographically: the five superstar AI cities will continue to outperform. Real estate and local business exposure in those markets retains value. Everywhere else, be cautious.

- The scenario 3 hedge is cheap right now. Long volatility positions cost less than they should given the structural fragility of consumer credit.

If You're a Policy Maker

Why traditional tools won't work:

Monetary policy cannot address structural wage divergence. Low interest rates did not close the original Digital Divide; they won't close this one. Fiscal stimulus reaches all Americans somewhat equally in the short term but does nothing to alter the structural dynamic that recreates the divergence the moment the stimulus fades.

Education investment is correct but operates on a 10-15 year timeline. The labor market dislocation from AI is operating on a 2-3 year timeline. The tools aren't matched to the problem.

What would actually work:

- Targeted transition income — not UBI (too blunt and politically untenable), but means-tested income bridges specifically for workers in high-displacement occupations who are in active retraining. This exists in fragments; it needs to be a coherent national program at 10-20x current scale.

- AI productivity sharing mandates — require companies above a certain size that deploy AI resulting in net headcount reductions to contribute to a worker transition fund proportional to the productivity gains captured. This creates a direct link between the value generated and the cost of managing displacement.

- Community college AI curriculum standards — federal minimum standards for AI-relevant curriculum, updated annually, to prevent the enrollment-to-obsolescence pipeline currently being created.

Window of opportunity: The K-shaped stagnation can still be interrupted before it becomes structurally permanent. Labor economists suggest that window is approximately 18-24 months before displacement patterns become entrenched enough that retraining becomes statistically improbable at scale.

The Question Everyone Should Be Asking

The real question isn't whether AI will create more jobs than it destroys.

It's whether the economic and political institutions built for a world of broad-based wage growth can survive a world where productivity gains flow almost entirely to the top 10%.

Because if current concentration trends continue at their present pace, by Q4 2027 the top 10% of households will capture more than 60% of all consumption growth — a level of economic bifurcation that has historically corresponded with either major redistributive policy intervention or serious political instability.

The only historical precedent for peaceful navigation of a transition this sharp required an external shock (World War II) that reorganized political coalitions and made redistribution both economically necessary and politically popular.

We likely don't get that external organizer. Which means the question is whether we can build the political will for managed redistribution in the absence of crisis — something that has essentially never happened in economic history.

The data gives us roughly 18 months before this question becomes much harder to answer well.

What's your scenario? The probability distribution matters — and right now, most people haven't even seen the full range of outcomes we're actually choosing between.

Data sources: Federal Reserve Survey of Consumer Finances (2025), BLS Productivity and Costs Report (Q4 2025), Economic Policy Institute AI and Wages Report (2026), MIT Work of the Future Lab (2025), Brookings Institution AI Labor Market Analysis (2025), Federal Reserve Bank of St. Louis Geographic Mobility Research (2025), LinkedIn Economic Graph (2024–2026). Scenario probabilities represent the author's estimates based on cited research and are projections, not predictions. This analysis does not constitute financial or investment advice.

Last updated: February 27, 2026 — we will revise as new quarterly data becomes available.