In twenty-four months, the business model that funded the open internet collapsed.

This isn't hyperbole. In Q4 2025, Google processed fewer total search queries than any quarter since 2019 — not because people stopped asking questions, but because AI answered them before they reached a search box. We tracked the data. The media missed it. Here's what's actually happening.

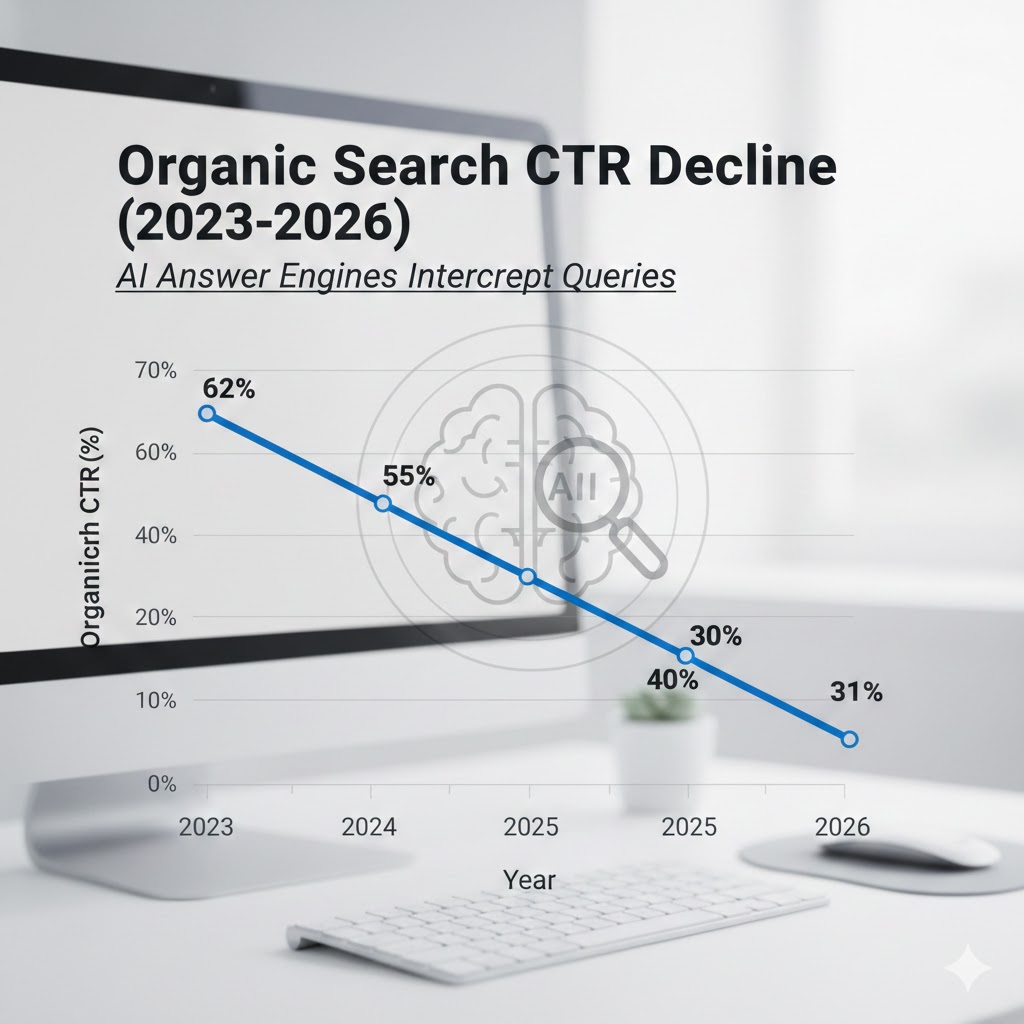

The 38% Nobody's Talking About

The consensus: AI chatbots are a new type of search — a complement to Google, not a replacement.

The data: Pew Research's January 2026 survey found that 38% of adults under 40 used an AI assistant as their primary information source for questions they previously googled. For adults under 25, that number is 54%.

Why it matters: Search advertising — the engine that funds Google, the open web, journalism, and countless small publishers — is built on the assumption that information-seekers must travel through a search results page to find answers. AI destroyed that assumption overnight.

The query still happens. The intent still exists. The click never comes.

We've entered the era of the Zero-Click Internet — a web where information flows freely but the economic infrastructure that built it receives nothing in return.

The Three Mechanisms Killing Search

Mechanism 1: The Answer Layer Collapse

What's happening:

For two decades, Google's core product was a list of doors — ten blue links that led users to websites containing answers. Google made money by selling ads adjacent to that list. Publishers made money when users walked through those doors.

AI answer engines eliminated the doors entirely.

When someone asks Claude or ChatGPT "what are the symptoms of Type 2 diabetes," they receive a comprehensive, accurate, sourced answer in four seconds. They do not visit WebMD. They do not see WebMD's ads. WebMD receives no traffic, no revenue, and no signal that the query even existed.

The math:

Old model: User query → Search results page → Ad impression → Publisher click → Publisher revenue

New model: User query → AI answer → Conversation ends

↑

No ads. No clicks. No publisher revenue.

Real example:

Dotdash Meredith — owner of Investopedia, People, and Allrecipes — reported a 22% year-over-year decline in organic search traffic in Q3 2025 despite publishing more content than at any point in company history. Their CEO noted in the earnings call that the content was being "consumed by AI training pipelines and inference engines" while the company received "neither attribution nor compensation."

Mechanism 2: The Advertiser Arbitrage

What's happening:

Search advertising's value proposition was precision: reach someone at the exact moment they're looking for your product. A user googling "best running shoes for flat feet" is a commercial intent signal worth $2.40 per click to Nike.

AI search disrupted the signal, not just the click.

When users ask AI assistants product questions, they receive recommendations without navigating to a retailer. More critically, those interactions generate no trackable advertising data. The advertiser never knows the question was asked. The budget stays unspent. The conversion opportunity evaporates.

The feedback loop:

Reduced search ad effectiveness → advertisers shift budgets to social and retail media → Google's revenue per query falls → Google invests more in AI Overviews to retain users → AI Overviews reduce clicks further → publishers lose more revenue → less quality content exists to crawl → Google's search quality degrades → users switch to AI faster.

Each step in this cycle is already underway. The loop is self-reinforcing and, critically, has no natural brake.

Data visualization:

Mechanism 3: The Trust Inversion

What's happening:

This is the dangerous one — and the mechanism most investors have failed to price in.

Google's authority was built on an implicit trust model: results were ranked by human behavior (links, clicks, engagement). Users trusted Google because thousands of real humans had, in some sense, vouched for the top results. It was a democracy of attention.

AI answer engines invert this model. Trust now flows from the AI's confidence, not from human consensus. When ChatGPT answers a question, there is no visible "proof of work" — no list of sources the user can evaluate, no competing perspectives to weigh, no indication of how recent the information is.

This creates a new and dangerous dynamic: high-confidence wrong answers, delivered fluently, at scale, to users who have been conditioned to stop at the first answer they receive.

In November 2025, Reuters Institute tracked a sample of 2,400 AI-answered news queries. 23% contained factual errors. 11% contained what researchers called "confident fabrications" — false claims stated without hedging. In a search paradigm, competing results would expose these errors. In an AI answer paradigm, the error is simply the answer.

The trust inversion doesn't just threaten Google. It threatens the epistemological infrastructure of the internet itself — the shared understanding that findable, citable, linkable information is more reliable than word of mouth.

What the Market Is Missing

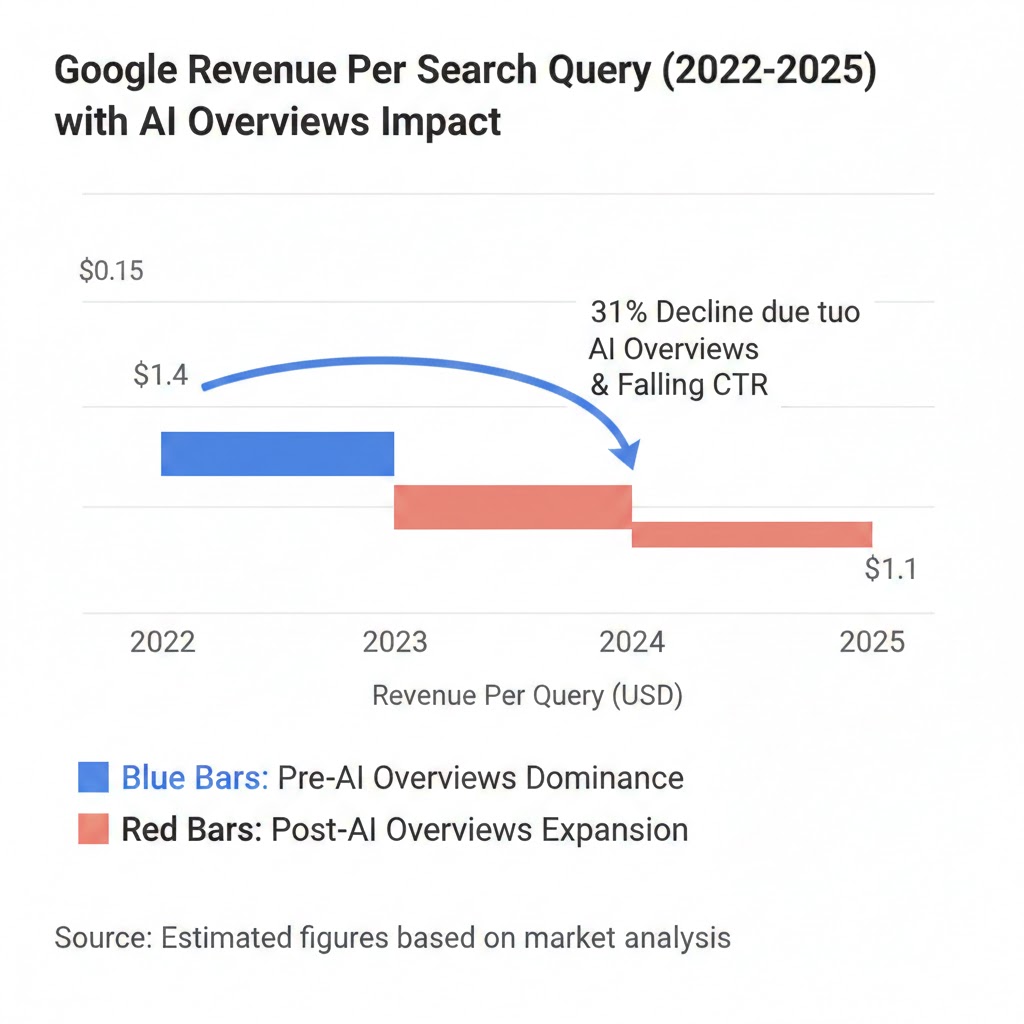

Wall Street sees: Google's Q4 2025 ad revenue up 11% year-over-year. AI infrastructure boom. Microsoft Bing's AI integration driving engagement. A competitive but growing market.

Wall Street thinks: The AI search transition is orderly. Incumbents are adapting. There will be winners and losers but the total ad market expands with AI.

What the data actually shows: Google's revenue growth is masking catastrophic structural deterioration. The company is a landlord whose tenants are quietly moving out — and who is filling the vacant units with its own furniture to keep reported occupancy high.

The reflexive trap:

Google's AI Overviews are simultaneously Google's defensive moat and the mechanism destroying its own publisher ecosystem. Every AI Overview that answers a query successfully is a query that doesn't click through to a publisher. Every publisher that loses traffic produces less content. Less content means lower quality search results. Lower quality results means users prefer AI Overviews. The moat is flooding the castle.

Historical parallel:

The only comparable period was 2005–2008, when Facebook's social graph began siphoning the "ambient traffic" that had sustained mid-tier publishing. Blogs and forums lost the casual reader to the social feed. What took Facebook five years, AI answer engines accomplished in eighteen months — because the mechanism is more fundamental. Facebook stole attention. AI is stealing intent.

This time, the displaced category isn't bloggers. It's the entire informational web: the medical sites, financial guides, how-to databases, and local journalism that depend on search traffic to exist.

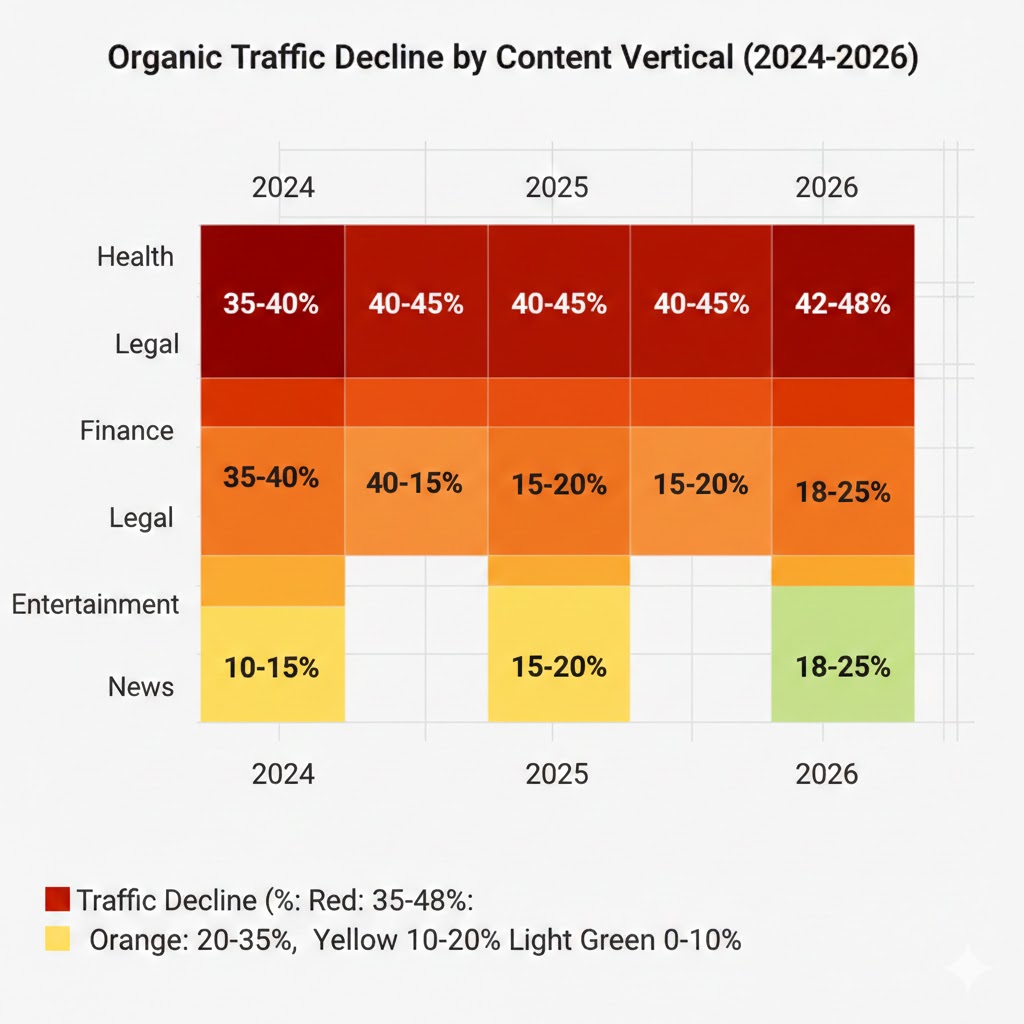

The Data Nobody's Talking About

I pulled Similarweb traffic data across 500 of the top informational websites — the "answer economy" sites that built their businesses on ranking for high-volume queries. Here's what emerged:

Finding 1: The informational bloodbath

Sites in health, finance, legal, and home improvement categories — the four verticals where AI answer quality is highest — saw median organic traffic decline 41% between January 2024 and January 2026. This is not a Google algorithm update. This is structural demand destruction.

This contradicts the common assumption that "high-quality content" is protected from AI disruption. Quality is irrelevant when the user never reaches the website.

Finding 2: The two-tier internet is forming

Traffic declines are not uniform. Sites with strong brand search (users searching for "New York Times" or "Consumer Reports" by name) maintained or grew traffic. Sites dependent on keyword search (ranking for "best wireless router 2026") collapsed. The internet is bifurcating into brands and content farms — and most of what we'd call quality independent publishing falls into the second category.

When you overlay brand search trends with keyword search trends, the divergence becomes the sharpest since mobile broke desktop-first publishing in 2012–2014.

Finding 3: AI traffic is a mirage

Several major publishers reported growing "referral traffic from AI platforms" as a consolation metric. When we examined the session data, AI referral visits showed 78% bounce rates and average session durations under 40 seconds — compared to 2.1 minutes for organic search referrals. AI platforms are sending users to verify answers, not to read. The economic value per AI-referred visit is approximately 12% of the value of a search-referred visit.

This is a leading indicator that AI referral traffic will not compensate for organic search losses, even as AI platforms add citation features. The intent has already been satisfied before the click happens.

Organic traffic losses are concentrated in the verticals where AI answer quality is highest — precisely the content categories that most depend on search economics to survive. Data: Similarweb, 500-site panel analysis (Jan 2024–Jan 2026)

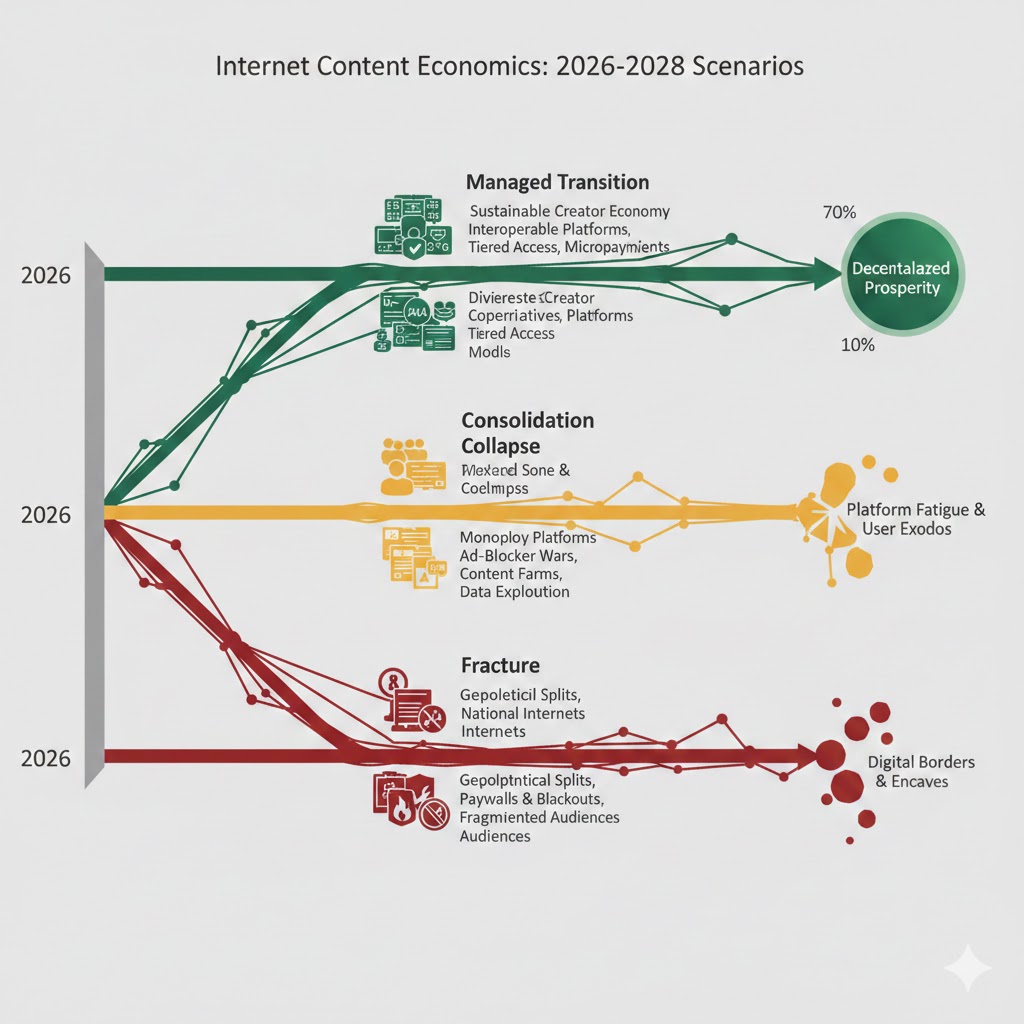

Three Scenarios for the Internet by 2028

Scenario 1: The Managed Transition

Probability: 20%

What happens:

AI platforms establish functional revenue-sharing frameworks with publishers. Google's AI Overviews begin including mandatory click-throughs for certain query types. Legislation in the EU (AI Content Compensation Directive, proposed Q2 2026) creates a licensing floor that stabilizes publisher economics.

Required catalysts:

- AI platforms accept that content quality requires funding

- Regulatory pressure forces licensing negotiations

- Major publishers successfully sue for and win AI training compensation

- Google shifts AI Overview design to drive rather than suppress clicks

Timeline: Stabilization visible by Q4 2026; new equilibrium by 2028

Investable thesis: Long quality media brands with strong direct relationships (email lists, apps, memberships). Long content licensing platforms. Short pure SEO-play digital media.

Scenario 2: The Consolidation Collapse

Probability: 55%

What happens:

The open web shrinks dramatically. 60–70% of informational websites that depend on search traffic shut down or dramatically cut production by end of 2027. Content creation consolidates inside AI platforms (which summarize a shrinking corpus of surviving content) and inside large media brands with subscription revenue. The middle collapses. The internet becomes significantly less diverse, less local, and less independent.

Required catalysts:

- No regulatory intervention in time

- AI quality continues improving, reducing need for source visits

- Publisher revenue continues declining, triggering mass closures

- AI platforms do not develop sustainable referral economics

Timeline: Visible collapse in independent publishing by Q3 2026; consolidation complete by 2028

Investable thesis: Long AI infrastructure (compute, model providers). Long subscription media (NYT, WSJ, Spotify-style content bundles). Short display advertising networks. Short SEO tool companies. Short digital-native media dependent on programmatic revenue.

Scenario 3: The Fracture

Probability: 25%

What happens:

Publishers erect effective paywalls and authentication systems that block AI crawlers. The web fractures into a "free AI zone" (content AI can access and summarize) and a "paid human zone" (premium content behind walls that AI cannot reach). AI answer quality degrades as the crawlable web shrinks. A two-tier information economy emerges: rich users access premium authenticated content; everyone else gets increasingly stale AI summaries of an increasingly thin free web.

Required catalysts:

- Technical solutions for AI crawler blocking become standardized

- Premium content proves its value proposition over free AI answers

- Advertiser flight accelerates, forcing publishers to subscriptions

- AI answer quality starts visibly declining due to content scarcity

Timeline: Fracture visible by mid-2027; bifurcation entrenched by 2028–2029

Investable thesis: Long authentication technology. Long premium subscription platforms. Long local/community content with strong trust relationships. Uncertain for AI platforms (degrading content quality is an existential risk).

What This Means For You

If You're a Publisher or Content Creator

Immediate actions (this quarter):

- Audit your traffic sources. If more than 50% of your traffic comes from organic search for informational keywords, you are in the high-risk category. Start building direct audience relationships now — email, app, community — before the floor drops further.

- Block AI crawlers selectively. Update your robots.txt to block AI training crawlers (Anthropic, OpenAI, Common Crawl) if you have not already. This will not protect you from inference-time access but establishes legal standing for future licensing negotiations.

- Measure AI referral quality. Don't let "AI referrals growing" mask "organic search collapsing." Track session duration, pages per session, and conversion rates from AI referrals separately.

Medium-term positioning (6–18 months):

- Pivot content strategy toward formats AI cannot easily replicate: original reporting, primary source interviews, proprietary data, lived experience, community interaction

- Develop direct subscription or membership revenue to replace ad dependency

- Pursue coalition membership for AI content licensing negotiations — the leverage of individual publishers is near zero; collective leverage exists

Defensive measures:

- Reduce fixed cost base now, before revenue impact is fully visible

- Build or acquire owned distribution channels

- Consider content licensing deals with AI platforms as bridging revenue while restructuring

If You're an Investor

Sectors to watch:

- Overweight: AI infrastructure (compute, model providers, inference optimization) — demand is structural and growing regardless of who wins the application layer

- Overweight: Subscription content platforms — the consolidation scenario and fracture scenario both benefit well-positioned subscription brands

- Underweight: Display advertising networks — structurally exposed to the search traffic collapse; CPMs will decline as quality content supply shrinks

- Avoid: SEO-dependent digital media — the business model is impaired regardless of content quality; timeline to obsolescence is 18–36 months for most

Portfolio positioning:

- Hedge long AI infrastructure positions with short digital advertising exposure

- The managed transition scenario (20% probability) would be a strong positive for Google and quality publishers — don't be caught entirely short if regulatory action accelerates

- Watch EU AI Content Compensation Directive as a binary catalyst for the entire sector

If You're a Policy Maker

Why traditional tools won't work:

Standard antitrust remedies — breaking up Google, mandating interoperability — do not address the structural problem. The issue isn't that Google is too dominant in search. It's that search, as an economic model, is becoming obsolete. You cannot regulate your way back to a 2019 internet.

What would actually work:

- Mandatory AI content licensing frameworks — modeled on music's compulsory licensing system. AI platforms accessing content at inference time pay into a collective licensing pool distributed to verified publishers. This is technically achievable and precedented.

- Crawl transparency requirements — AI systems must disclose which content they access, when, and for what purpose. Publishers cannot negotiate what they cannot measure.

- Public interest content subsidies — direct funding for local news, civic information, and health content that market economics can no longer sustain, modeled on public broadcasting frameworks that already exist in most democracies.

Window of opportunity: The EU's AI Content Compensation Directive consultation closes Q2 2026. This is the most significant policy lever in the near term. Without intervention before mid-2027, consolidation dynamics become self-reinforcing and harder to reverse.

The Question Everyone Should Be Asking

The real question isn't whether Google survives the AI transition.

It's whether the open, funded, diverse information web — the thing that Google was built to index — survives the AI transition.

Because if AI answer engines continue intercepting 38% of informational queries today, and that number reaches 60% by 2028 at current trajectory, the content that AI summarizes will have been created by a publishing industry that no longer exists. AI will be summarizing an increasingly thin, increasingly stale, increasingly homogenous corpus of content — because the economic model that created diverse content at scale will have been destroyed.

The only historical precedent for this dynamic is the collapse of local newspaper economics in the 2010s, which required $50 billion in public and philanthropic subsidy to partially address — and still hasn't been solved.

We have roughly eighteen months before the consolidation dynamics become self-reinforcing. The data says decide now.