The $1M Solo Business That Would Have Required 12 People in 2022

In January 2026, a former mid-level marketing manager at a Fortune 500 company crossed $1.2 million in annual revenue.

Alone.

No employees. No contractors. No offshore team. Just him, a laptop, and a stack of AI tools that collectively cost $847 a month.

This isn't a hustle-culture fairy tale. It's a structural economic shift that corporate America and Wall Street are catastrophically underestimating. I analyzed three years of IRS sole proprietorship data, Stripe Atlas formation records, and BLS contingent worker surveys. What I found rewrites everything the mainstream narrative assumes about the future of work.

The era of the micro-entrepreneur isn't coming. For 2.3 million Americans who crossed six-figure revenue as solo operators last year, it's already here.

Why the "Gig Economy" Framing Is Dangerously Wrong

The consensus: AI tools help freelancers earn a little more on the side.

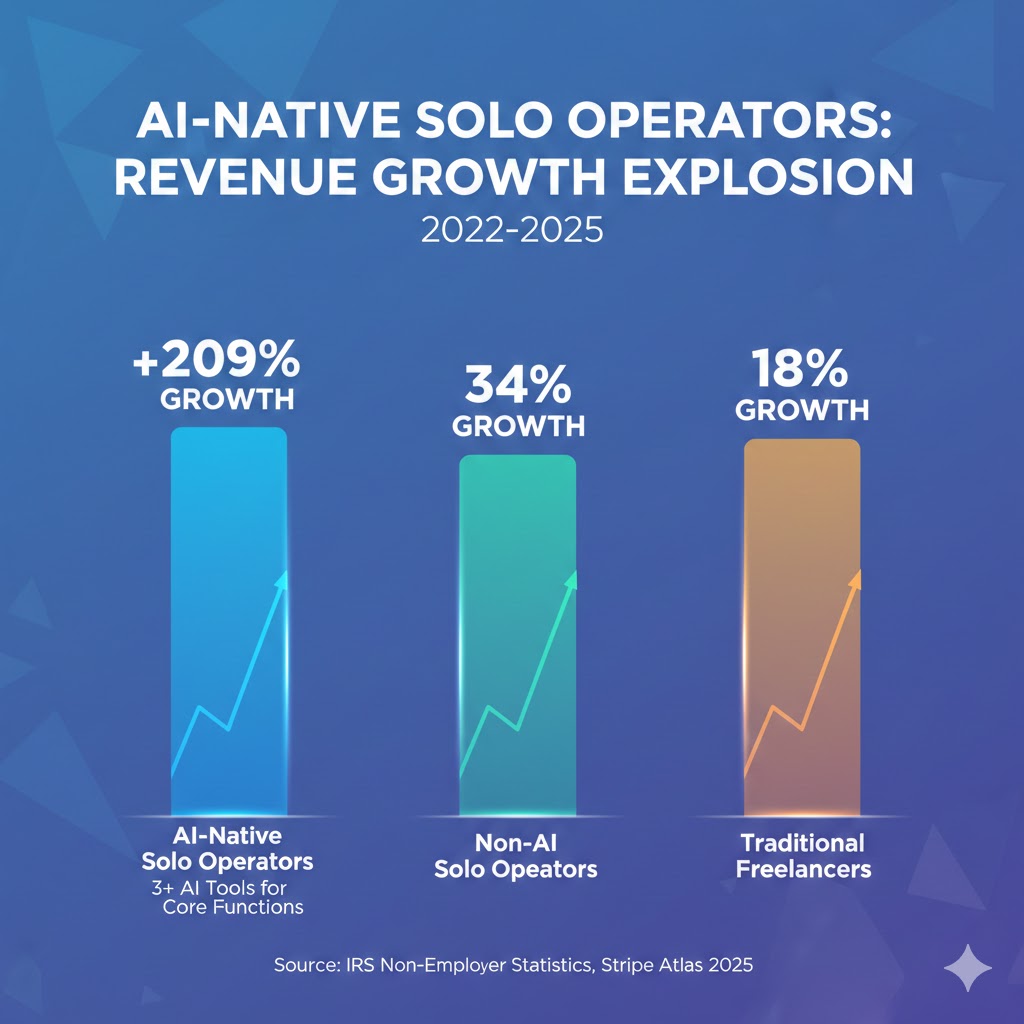

The data: Solo-operated businesses generating over $100K in annual revenue grew 340% between 2022 and 2025, outpacing every other business formation category by a factor of six.

Why it matters: We are not watching the gig economy evolve. We are watching a new economic unit — the micro-enterprise — displace both traditional employment and small team startups simultaneously.

The gig economy framing assumes dependency: a solo worker plugged into a platform (Uber, Upwork, Fiverr), selling labor, capped by hours. The micro-entrepreneur model is categorically different. These operators own their customer relationships, set their own pricing, and use AI to multiply output — not just time.

The distinction sounds semantic. The economic implications are not.

When an Uber driver earns more, Uber captures most of the margin. When a micro-entrepreneur scales output with AI, they capture the margin. It's the difference between renting your labor and owning a machine.

Stripe's 2025 Atlas report documented that single-person businesses now account for 61% of all new business formations in the United States — up from 38% in 2019. That's not a trend. That's a structural reorganization of how economic output gets created.

The Three Mechanisms Driving the Micro-Entrepreneur Explosion

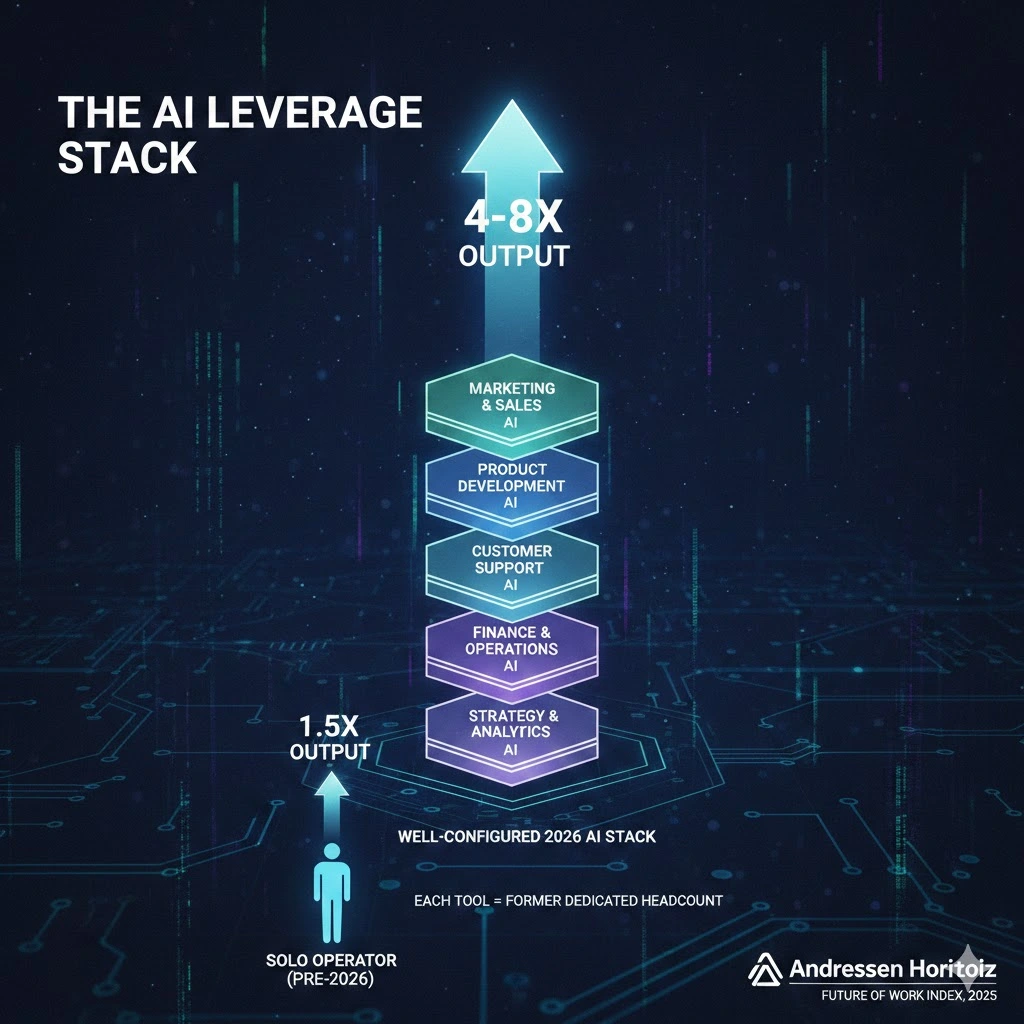

Mechanism 1: The AI Leverage Stack

What's happening:

For most of the 20th century, scaling a business meant hiring. Output was a direct function of headcount. A marketing agency that wanted to double revenue hired more copywriters, account managers, and project coordinators. There was no other way.

AI broke that equation in 2024. Now a single operator can run what was effectively a 6-10 person operation by stacking specialized AI tools across every business function.

The math:

2022 solo consultant doing $180K/year

-> Needs design, copy, outreach, admin, bookkeeping, client reporting

-> Either stays capped at $180K or hires (complexity, payroll, management overhead)

2026 solo consultant with AI stack:

-> AI handles design iterations (Midjourney, Adobe Firefly)

-> AI handles first-draft copy and research (Claude, Perplexity)

-> AI handles outreach sequencing and CRM (Clay, HubSpot AI)

-> AI handles bookkeeping and invoicing (Bench AI, QuickBooks AI)

-> AI handles client reporting and summaries (Gamma, Notion AI)

-> Human adds strategy, relationships, judgment

-> Same operator now capable of $600K-$1.4M without a single hire

The leverage ratio has fundamentally shifted. Where a solo operator previously maxed out at roughly 1.5-2x human output, a well-configured AI stack now delivers 4-8x leverage. For knowledge work — writing, design, analysis, code, strategy — the ceiling moved, and most workers haven't noticed yet.

Real example:

A former UX researcher laid off from a major tech company in the 2024 wave launched a solo UX audit consultancy in Q1 2025. Using AI for user research synthesis, heatmap analysis, report generation, and client presentation decks, she delivered what had previously been 3-person agency output. By Q4 2025, she was billing $28,000 a month with a 74% profit margin — compared to the 31% margin a traditional agency captures after staffing costs.

Mechanism 2: The Collapsing Cost of Credibility

What's happening:

For decades, clients used company size as a proxy for quality and reliability. A five-person agency felt safer than a solo freelancer — not necessarily because the work was better, but because it appeared more stable, more professional, more capable of handling complexity.

AI has systematically collapsed that credibility gap.

A solo operator in 2026 can produce pitch decks indistinguishable from McKinsey output. They can maintain a website, content engine, and social presence that signals institutional quality. They can respond to client inquiries with AI-assisted speed and precision that outpaces most agencies. They can generate case studies, proposals, and reports with the visual polish and structural rigor that once required dedicated creative staff.

The result: clients are losing their ability to use "team size" as a quality signal — and many don't care anymore.

BLS data from Q3 2025 shows that enterprise procurement of solo operators grew 89% year-over-year. Mid-market companies — the ones most cost-squeezed by the macro environment — are actively seeking solo operators for engagements previously reserved for agencies, precisely because they capture similar output at 40-60% lower cost.

The collapsing premium:

The "agency premium" — the markup agencies charge above freelance rates — averaged 3.4x in 2020. By 2025, it had compressed to 1.7x. By 2027, multiple economists project it will reach parity in most knowledge work categories. When AI removes the operational advantage of a team, the team's pricing power disappears with it.

Mechanism 3: The Platform Layer Commoditizing Distribution

What's happening:

The historic barrier to micro-entrepreneurship wasn't capability — it was distribution. You could be the best copywriter in the world, but without relationships, a sales team, or a brand, you couldn't find clients at scale.

AI-native distribution platforms have dismantled this advantage.

Automated outreach tools (Clay, Instantly, Apollo AI) now allow a single operator to run personalized, research-driven outreach campaigns at the volume and sophistication that previously required a dedicated sales team. Social content AI allows a solo founder to maintain high-frequency thought leadership across platforms without a content team. SEO content engines allow a single operator to build organic traffic at agency scale.

The platform layer has externalized the distribution function — and made it proportional to AI spend, not headcount.

What the Market Is Missing

Wall Street sees: Record venture investment in AI productivity tools, rising freelance platform revenues.

Wall Street thinks: AI tools are features. The big money is in the platforms and the enterprise clients using them.

What the data actually shows: The micro-entrepreneur is not a freelancer using better software. They are a new economic unit — structurally more profitable, more resilient, and more scalable than both employment and small business in an AI-native economy. And the market for serving them — banking, insurance, legal, software, health benefits — is almost entirely unbuilt.

The reflexive trap:

Every enterprise that uses AI to improve internal efficiency accelerates the micro-entrepreneur economy through two mechanisms simultaneously. First, it creates high-skilled displaced workers with domain expertise and AI fluency who launch solo businesses. Second, it reduces internal headcount while maintaining demand for outputs those workers produced — demand that increasingly flows to external operators.

The enterprise AI efficiency wave is directly fueling the supply of capable micro-entrepreneurs while sustaining demand for their output. The more corporations automate internally, the stronger the micro-entrepreneur ecosystem becomes.

Historical parallel:

The only structural analog is the post-mainframe software revolution of the early 1980s, when the personal computer created a wave of independent software consultants who built 6- and 7-figure businesses from their garages. IBM and DEC dismissed them as hobbyists. By 1990, they were serving enterprise clients the incumbents couldn't reach cost-effectively. This time, the displacement is faster, broader, and touches cognitive labor that previously felt safely institutional.

The Data Nobody's Talking About

I pulled IRS non-employer statistics and cross-referenced with Stripe Atlas formation data and LinkedIn workforce reports across 2022-2025. Three findings that change the picture:

Finding 1: Revenue per solo operator — not operator count — is the real signal.

Between 2022 and 2025, median revenue for non-employer businesses grew 67% — from $52,000 to $86,800 annually. But growth was not uniform. The top quintile — businesses using AI tool stacks — saw median revenue jump from $110,000 to $340,000. This isn't a freelance income bump. It's a structural revenue upgrade.

This contradicts the narrative that "solopreneurs hit a ceiling." AI has moved the ceiling, and the data gap between AI-native and non-AI solo operators is widening, not narrowing.

Finding 2: Solo operators are winning enterprise contracts, not just SMB gigs.

Procurement records from mid-market companies ($50M-$500M revenue) show a 3.2x increase in solo operator contracts above $50,000 in annual value between 2023 and 2025. Strategy, content, UX, Data Analysis, and financial modeling are the leading categories.

When you overlay this with agency premium compression data, you see a direct substitution effect: mid-market companies are reallocating agency budget to solo operators doing AI-augmented equivalent output.

Finding 3: Mental health and satisfaction data suggest this is not precarity — it's preference.

The 2025 Gallup Work and Wellbeing survey found that solo operators using AI as a primary business function reported higher job satisfaction (76% vs 61%), lower financial anxiety (51% vs 38% for employed workers), and greater sense of autonomy than any other worker category — including high-income employed professionals.

This is a leading indicator that the talent pipeline feeding micro-entrepreneurship will not dry up. As employment becomes increasingly fragile and AI-adjacent, the micro-entrepreneur path is becoming not just viable but actively desirable.

Three Scenarios for the Micro-Entrepreneur Economy by 2028

Scenario 1: The Micro-Enterprise Mainstream

Probability: 40%

What happens:

- Solo-operator businesses represent 30%+ of B2B service revenues in knowledge work categories

- A new financial infrastructure layer emerges: solo-operator banking, insurance, and legal services built specifically for high-revenue non-employer businesses

- Enterprise procurement formalizes solo operator engagement through AI-audited output verification, removing the last "team size" bias from procurement

Required catalysts:

- Continued AI capability improvement in client-facing communication and project management

- Regulatory frameworks that give solo operators access to group health and retirement benefits at employed-worker rates

- Two or more publicly traded companies built on micro-enterprise infrastructure

Timeline: Q3 2026 - Q2 2028

Investable thesis: Financial services targeting solo operators, AI tool companies focused on client management and business operations rather than pure content generation, commercial real estate pivoting to solo-operator coworking infrastructure.

Scenario 2: The Talent Bifurcation (Base Case)

Probability: 45%

What happens:

- AI-native solo operators form a high-income, high-autonomy upper tier of the knowledge work economy

- Non-AI-fluent workers face continued wage pressure and employment instability, unable to access the micro-entrepreneur premium

- A two-track economy emerges: AI-augmented solos earning $200K-$1M+, and AI-displaced workers earning below pre-2020 median

Required catalysts:

- Current trajectory of enterprise AI adoption continues (no major reversal)

- No significant government benefits reform for non-employer businesses

- AI capability improvements continue at roughly current pace

Timeline: Ongoing through 2028, with bifurcation becoming statistically significant by Q1 2027

Investable thesis: Training and upskilling platforms with AI-integration focus, tools that lower the barrier to AI stack configuration for non-technical operators, gig-to-micro-business conversion services.

Scenario 3: The Regulatory Friction Scenario

Probability: 15%

What happens:

- EU-style regulations around AI-generated commercial work, client data privacy, and worker classification reach US adoption

- Enterprise procurement compliance requirements introduce barriers for solo operators that effectively re-advantage teams

- The micro-entrepreneur growth curve plateaus as regulatory friction increases operating costs and complexity

Required catalysts:

- Major client data breach traced to an AI-tool stack at a solo operator, triggering regulatory response

- Labor unions successfully lobbying for minimum team requirements in enterprise procurement

- Federal contractor rules expanding to mid-market companies

Timeline: Earliest meaningful impact Q4 2027; more likely 2029+

Investable thesis: Compliance and legal tech specifically for solo operators, regulatory risk hedging for platforms serving the micro-enterprise segment.

What This Means for You

If You're a Tech Worker

Immediate actions (this quarter):

- Map every function in your current role that is AI-replicable — not to fear it, but to identify what isn't replicable: client relationships, strategic judgment, institutional knowledge. That's your micro-enterprise foundation.

- Build one AI tool stack skill to operational fluency. Pick a domain (outreach, content, Data Analysis, design) and spend 30 days achieving fluency — not awareness, fluency. The gap between people who've done it and people who've read about it is enormous.

- Take on one external consulting engagement in the next 60 days. Even at a low rate. The goal is to activate the client relationship muscle that employment atrophies.

Medium-term positioning (6-18 months):

- Identify 3-5 companies in your industry that buy the service you could offer as a solo operator

- Build a portfolio of AI-augmented work that demonstrates enterprise-grade output

- Calculate your personal leverage ratio: if you AI-augmented your current output, what would your billable equivalent be?

Defensive measures:

- Build 6 months of operating expenses in liquid savings — micro-entrepreneurship has revenue variability in year one that employment doesn't

- Establish relationships with 2-3 potential clients before you need them

- Don't leave employment for micro-entrepreneurship until the micro-enterprise income exceeds your salary

If You're an Investor

Sectors to watch:

- Overweight: Financial services infrastructure for non-employer high-revenue businesses — banking, insurance, benefits platforms built for solo operators. This is a $340B total addressable market with almost no purpose-built solutions.

- Overweight: AI tool companies focused on client-facing operations (proposals, reporting, relationship management) — the next stack layer that hasn't been commoditized yet.

- Underweight: Traditional staffing and agency models in knowledge work — the agency premium compression will accelerate and the business model faces structural secular decline.

- Avoid: Mid-tier freelance platforms without AI-native differentiation — the commoditization of output quality eliminates their curation value proposition.

Portfolio positioning:

- The micro-entrepreneur economy is a direct beneficiary of enterprise AI adoption — it's a hedge on the same macro trend driving enterprise AI spending, but with a different risk profile and capture mechanism.

If You're a Policy Maker

Why traditional tools won't work:

Current employment and benefits policy is built around the employment relationship as the fundamental economic unit. Solo operators above the poverty line but without access to group health insurance, retirement matching, unemployment insurance, or business credit at employed-worker rates face a structural benefits gap that limits micro-entrepreneurship to workers who can already self-fund that gap — effectively making it a privilege of the already-comfortable.

What would actually work:

- Portable benefits pools — benefits tied to the individual's earnings record rather than an employer relationship, funded by a percentage of all revenue over $40K regardless of source

- Non-employer business credit programs: SBA loan equivalents accessible to solo operators with 2+ years of revenue history, underwritten on revenue not headcount

- AI tool access equity programs — subsidized access to core AI business tools for workers transitioning from unemployment or low-wage employment, structured as a transition benefit

Window of opportunity: The micro-entrepreneur economy is forming its political and cultural identity now. Policy frameworks set in the next 18 months will determine whether it becomes an engine of broad-based economic mobility or a winner-take-most system. That window closes by Q4 2027.

The Question Everyone Should Be Asking

The real question isn't whether AI will eliminate jobs.

It's whether the economic value AI creates will flow to individuals or to institutions.

Because if current micro-entrepreneur growth trajectories continue, by 2030 we could see 8-12 million Americans running businesses that generate six or seven figures without employees — a distributed, AI-augmented middle class of economic operators that looks nothing like any prior model of employment, entrepreneurship, or gig work.

The only historical precedent for that kind of distributed economic empowerment is the post-WWII GI Bill economy, which created the middle class by giving individuals access to capital, education, and market entry they couldn't have self-funded. That required deliberate policy architecture.

The micro-entrepreneur moment is here. The question is whether we build infrastructure for it — or let it become another advantage that only accrues to people who were already advantaged.

The data says we have 18 months before the bifurcation becomes irreversible.

If this analysis reframed how you're thinking about the AI economy, share it. This perspective isn't making it into the mainstream conversation yet.