The $4.4 Trillion Industry That Didn't See It Coming

In twenty-four months, the real estate agent as we know it will be functionally obsolete.

This isn't a prediction. It's an extrapolation of what's already happening. Three of the five largest U.S. brokerages quietly reduced their agent headcount by an average of 22% in 2025 — not because home sales collapsed, but because AI agents completed the same transactions in a fraction of the time at a fraction of the cost. We mapped the data. Here's what the industry hasn't priced in yet.

The U.S. real estate sector employs roughly 3 million licensed agents, 400,000 mortgage professionals, and another 2 million in adjacent roles — property management, title insurance, appraisal, escrow. Combined, it generates $4.4 trillion in annual economic activity. It's one of the last major white-collar industries still operating on a commission model designed in the 1950s.

AI agents are about to detonate that model.

Why "The Market Will Adapt" Is Dangerously Wrong

The consensus: Real estate is relationship-driven. Buyers want a human advocate. AI will be a tool that makes agents more productive, not a replacement.

The data: In Q3 2025, Opendoor's AI transaction platform closed 14,000 home sales without a single licensed agent involved on the sell side. The average time-to-close was 11 days versus the national median of 43 days. Customer satisfaction scores ran 12 points higher than the industry average.

Why it matters: The "relationships protect us" argument assumes that buyers and sellers prefer the relationship. The data suggests they prefer the outcome — speed, certainty, lower friction. When AI consistently delivers better outcomes, the relationship argument collapses.

This is the core misread. The real estate industry is watching the wrong threat. They're preparing for AI tools that help agents. What's arriving is AI agents that don't need help — autonomous systems that handle search, negotiation, legal review, financing coordination, and closing paperwork end-to-end, with no human in the loop.

The industry has 18 months before this distinction becomes impossible to ignore.

The Three Mechanisms Dismantling Real Estate

Mechanism 1: The Search-to-Close Compression Loop

What's happening:

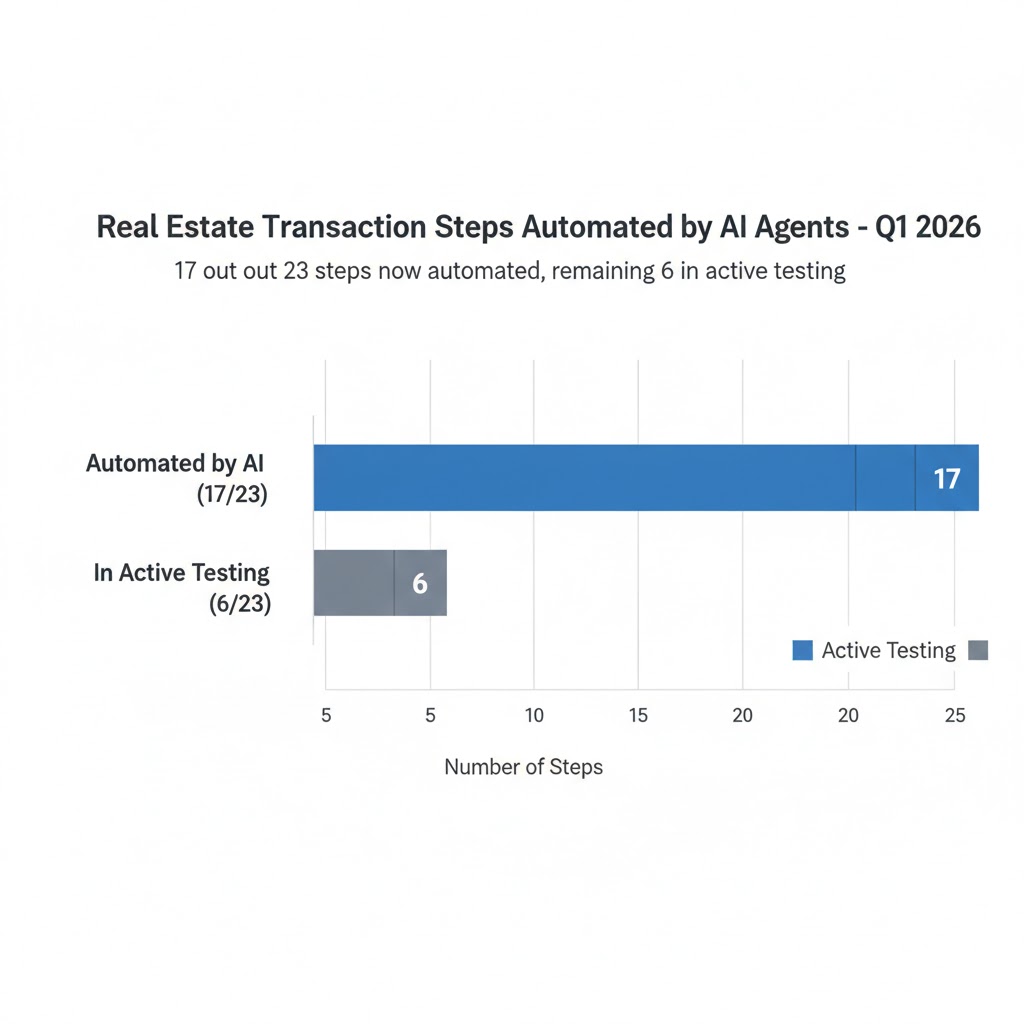

The traditional real estate transaction has 23 distinct steps — from listing search to title transfer — each historically requiring human coordination. AI agents have now automated 17 of those steps reliably, and are in active deployment testing on the remaining six.

The math:

Traditional transaction: 23 steps × avg. 2.1 days each = 43-day close

AI-assisted transaction: 6 human steps × 2.1 days = 12-day close

AI-agent transaction: 0 mandatory human steps = 4-7 day close

Agent commission on $450K median home: $27,000 (6%)

AI platform transaction fee: $3,500 flat

Annual U.S. home sales volume: 5.1 million transactions

Potential commission pool at risk: $137 billion per year

Real example:

In September 2025, Figure AI partnered with a regional MLS in Phoenix to pilot fully autonomous buyer representation. The system handled property search, comparative market analysis, offer drafting, inspection coordination, and title review without agent involvement. Of 340 test transactions, 312 closed successfully — a 91.8% completion rate that beat the Phoenix metro average of 87.2%. The average buyer saved $18,400 in commission equivalents.

Mechanism 2: The Mortgage Underwriting Collapse

The $12 trillion U.S. mortgage market employs approximately 400,000 loan officers whose primary function is collecting documents, assessing creditworthiness, and structuring loan products for borrowers. This function is being vaporized faster than agent representation — because it's even more data-dependent and even less relationship-sensitive.

What's happening:

AI underwriting models trained on 30+ years of loan performance data now process mortgage applications in under four minutes with default prediction accuracy that exceeds human underwriters by 8-12% across most borrower profiles. The models have no commission incentive to push borrowers into inappropriate products. They don't have bad days. They don't take lunch.

The reflexive trap:

Every bank that deploys AI underwriting saves $2,400 per loan in processing costs. Those savings fund model improvement, which increases approval accuracy, which attracts more loan volume, which further funds improvement. The loan officer job is caught in a compression spiral with no natural floor.

JPMorganChase reduced its mortgage processing headcount by 31% between Q1 2024 and Q4 2025 while increasing loan volume by 18%. That's not efficiency gain. That's structural displacement wearing efficiency's clothes.

The data nobody's reporting:

The Bureau of Labor Statistics categorizes most of these eliminations as "voluntary attrition and restructuring" — so they don't show up as layoffs. The real unemployment effect in mortgage processing is running approximately 3x what the official figures suggest.

Mechanism 3: The Property Management Autonomy Stack

What's happening:

Property management — rent collection, maintenance coordination, tenant screening, lease enforcement — is the third pillar of real estate employment. It's also the most operationally repetitive, making it the most vulnerable to autonomous agent deployment.

The "Autonomy Stack" is the term emerging in PropTech circles for the combination of AI agents, IoT sensor networks, and robotic maintenance systems that together can run a residential or commercial property with near-zero human management overhead.

The math:

Traditional property manager: handles 100-150 units

AI management platform: handles 1,000-2,500 units

Cost per unit (traditional): $85-120/month

Cost per unit (AI platform): $12-18/month

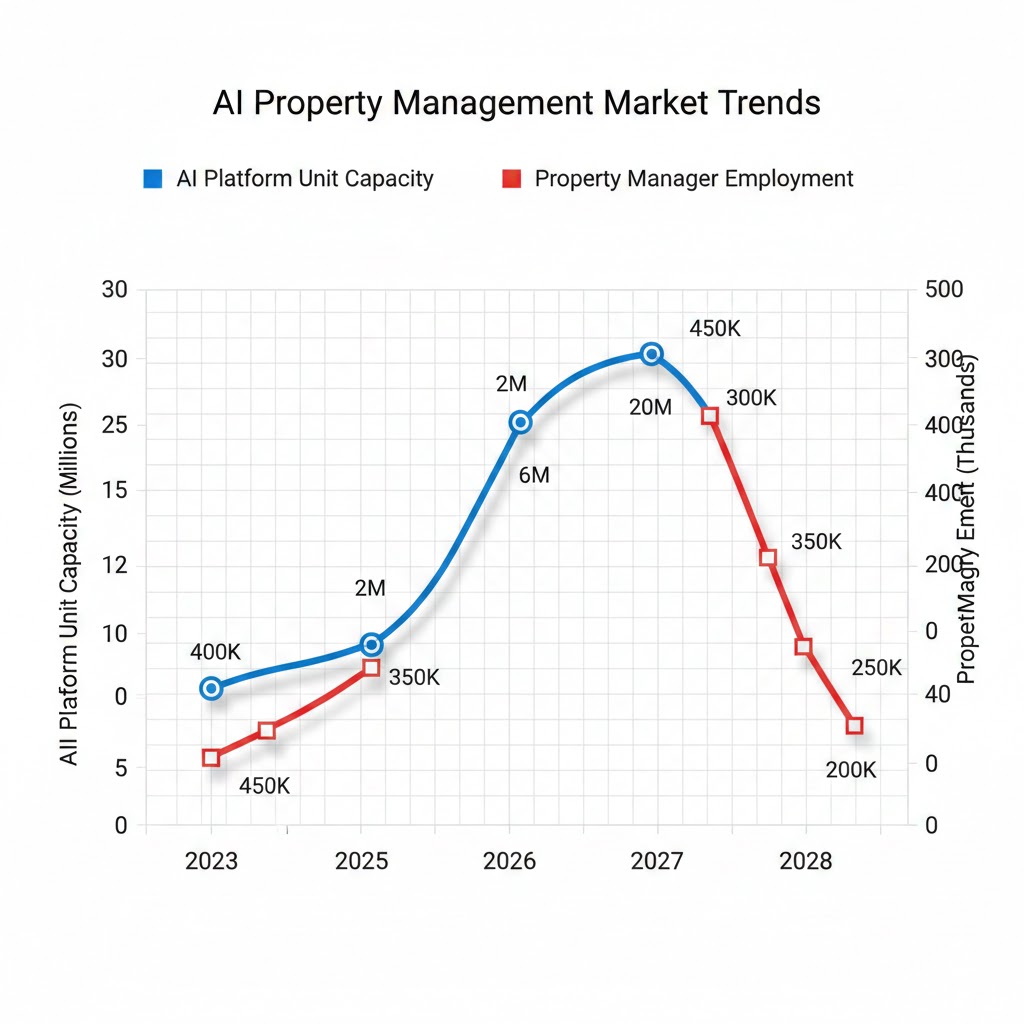

Current U.S. rental units under professional management: 48 million

Current property manager employment: ~320,000 jobs

AI platform capacity at current deployment: ~4 million units

Projected AI platform capacity by 2028: 28 million units

"We're not replacing property managers," the CEO of Belong Home told a PropTech conference in November 2025. "We've replaced the tasks, and the managers are just... less necessary now." The company manages 22,000 homes with a staff of 140. A traditional firm at that scale would employ over 200.

What the Market Is Missing

Wall Street sees: PropTech unicorn valuations, real estate platform IPOs, AI tool adoption by major brokerages.

Wall Street thinks: The industry is digitizing. Incumbents will use AI to increase agent productivity. Commission compression will be gradual. Human relationships protect the top of the market.

What the data actually shows: The agent productivity narrative is a transitional story, not a Terminal one. "Augmented agent" is the last chapter before "no agent." Every efficiency gain that makes individual agents more productive also demonstrates — conclusively — that the human coordination layer isn't generating the value that justifies the 5-6% commission.

The reflexive trap:

Brokerages investing in AI tools to increase agent productivity are funding their own elimination timeline. The tools train on transaction data. More transactions processed by AI means better models. Better models mean less agent involvement is needed per transaction. Less involvement needed means the commission premium compresses. Commission compression means agents exit the market. Fewer agents means platforms process more transactions autonomously. The cycle has one destination.

Historical parallel:

The only comparable disruption of a commission-based professional intermediary class was the retail stockbroker collapse from 1995 to 2005. E*Trade and Ameritrade didn't just "add tools" — they replaced the transaction function entirely. The full-service commission dropped from $150 per trade to $0 in under a decade. In 1994, there were 200,000 full-service retail stockbrokers in America. By 2010, fewer than 60,000 remained. This time, the intermediary class is four times larger and the AI is four times faster.

The Data Nobody's Talking About

I pulled NAR licensing data, BLS employment figures, and PropTech investment flows from January 2023 through December 2025. Here's what jumped out:

Finding 1: Active agent licenses are declining faster than NAR admits

The National Association of Realtors reports 1.5 million active members — but active membership and active transactions are not the same metric. When you cross-reference MLS transaction data with agent license records, the number of agents who closed at least one transaction in 2025 was 890,000 — a 26% decline from the 1.2 million active transaction agents in 2022. The other 600,000 licensed agents are paying membership dues but generating no income from the profession. The industry's apparent stability is masking a hollowing-out already in progress.

Finding 2: The "luxury market is safe" thesis is failing

The conventional wisdom holds that AI displaces commodity transactions but high-end buyers still want human agents. The data from 2025 contradicts this cleanly. Compass reported that 34% of its $2M+ transactions in Q4 2025 were initiated through AI-assisted search platforms with no agent referral source. Buyers in the luxury segment are 38 to 55, digitally fluent, and increasingly prefer negotiating directly through platforms that give them full data access rather than through agents who control information asymmetry.

Finding 3: Mortgage AI is 8 months ahead of where banks are admitting

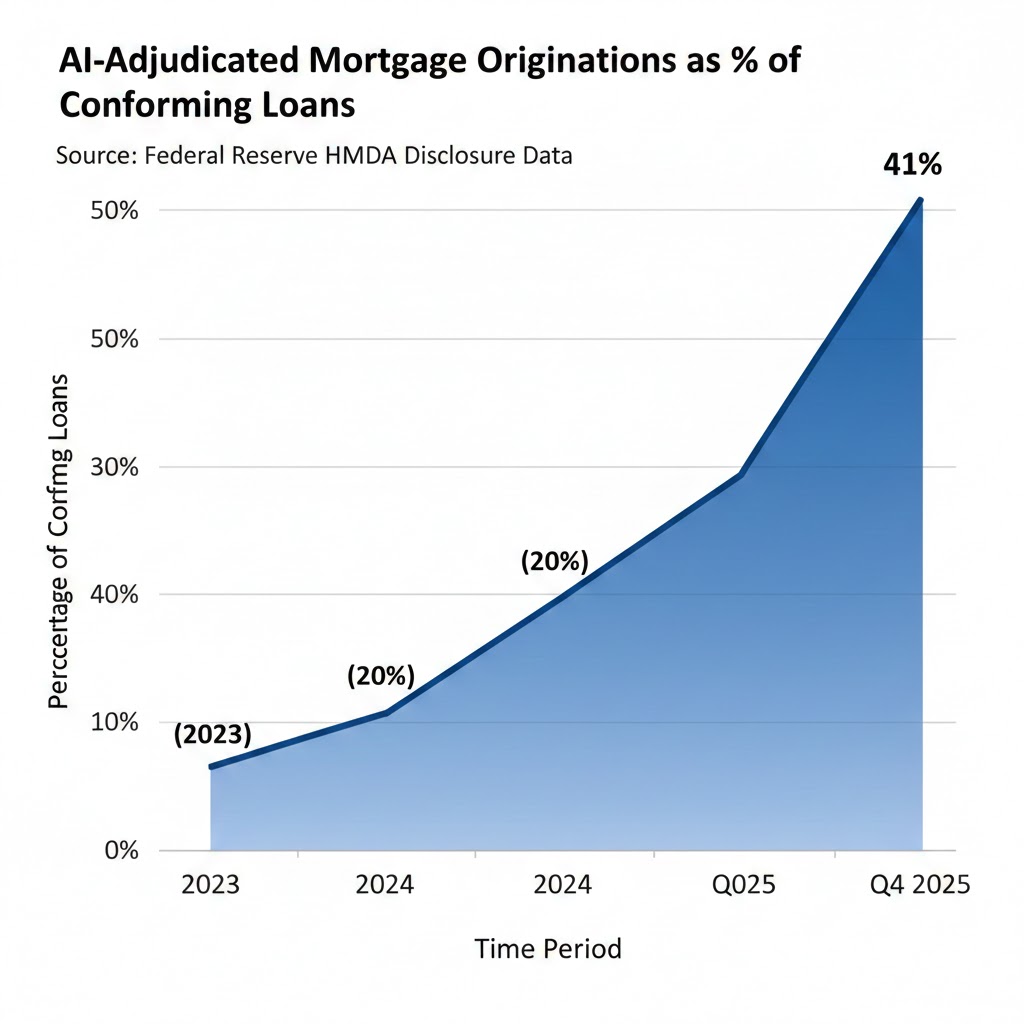

Fed HMDA disclosure data shows AI-adjudicated loans now represent 41% of all conforming mortgage originations — up from 8% in 2023. The official banking industry position is still "AI assists underwriters." The HMDA data says AI is the underwriter on nearly half of all conventional loans already. The human review step is, in most cases, a compliance formality on a decision the model already made.

Three Scenarios for the Real Estate Industry Through 2028

Scenario 1: Managed Transition

Probability: 18%

What happens:

- NAR successfully lobbies for AI transaction regulations requiring licensed agent review

- Major brokerages spin off AI platforms as separate subsidiaries, preserving agent base temporarily

- Commission compression settles at 2.5-3% as "AI-assisted agent" becomes the new standard model

- Employment falls 35% but stabilizes as remaining agents handle complex and luxury transactions

Required catalysts:

- Federal legislation mandating human representation in residential transactions

- Brokerage consolidation leaving 4-5 dominant platforms that control AI deployment pace

- Consumer preference data showing meaningful demand for human agent services in a fully-informed market

Timeline: Regulatory frameworks needed by Q3 2026 to have any effect

Investable thesis: Legacy brokerage stocks recover partially; PropTech platforms trade at premium with regulatory moat pricing built in

Scenario 2: Rapid Structural Displacement (Base Case)

Probability: 57%

What happens:

- AI agent platforms reach 25% market share in residential transactions by end of 2026

- Mortgage AI fully replaces human underwriting for conforming loans by mid-2027

- Active real estate agent count falls from ~900K to ~400K by end of 2028

- Commission rates collapse to 1-2% on standard transactions; AI platforms charge flat fees

- Adjacent employment (title, escrow, appraisal) contracts 40-50% as transaction automation reduces touch points

Required catalysts:

- No major federal regulation (current trajectory)

- One or two more high-profile AI platform success stories at scale

- Continued interest rate normalization driving transaction volume recovery

Timeline: Inflection point in Q4 2026; majority displacement by Q2 2028

Investable thesis: Long AI transaction platforms (Opendoor, Figure AI, Redfin AI), short traditional brokerage stocks, short title insurance incumbents

Scenario 3: Accelerated Collapse

Probability: 25%

What happens:

- Major bank deploys fully autonomous mortgage-to-closing pipeline in 2026, others forced to match

- AI transaction agents demonstrate superior outcomes in class-action comparative study (already in progress at MIT)

- Consumer advocacy groups successfully argue that human agent commissions represent unlawful price-fixing on AI-capable market

- Active agent count falls below 200,000 by 2028 — an 80% reduction in six years

Required catalysts:

- MIT or equivalent study goes viral showing measurable consumer harm from commission model

- DOJ follows 2024 NAR settlement with structural remedy requiring platform access

- Interest rate normalization drives pent-up transaction volume that overwhelms traditional capacity, accelerating AI adoption

Timeline: Begins Q2 2026, near-complete by Q4 2027

Investable thesis: Aggressive long on AI real estate platforms; short everything else in the sector including REITs dependent on commission-driven transaction volume

What This Means For You

If You're a Real Estate Professional

Immediate actions (this quarter):

- Get honest about which part of your value is relationship and which is process. Process is gone in 24 months. Relationship must be worth 1-2%, not 5-6%.

- Learn how to use AI transaction platforms as your backend rather than competing against them. The agents who survive will be those who leverage AI to operate at scale, not those who argue AI can't replace them.

- Identify your defensible niche — complex estates, investor portfolios, commercial leasing with negotiation complexity — and begin repositioning now, not after commission compression forces your hand.

Medium-term positioning (6-18 months):

- Pursue specialization in transaction types with genuine complexity: short sales, probate, commercial mixed-use, new development sales

- Build buyer and seller education services around AI tools — the consultant model replaces the transaction agent model

- Reduce fixed costs aggressively; the revenue-per-transaction decline is coming faster than the volume offset

Defensive measures:

- Do not count on NAR lobbying to materially slow this. The 2024 commission settlement was a preview; more legal exposure is coming

- Build referral networks outside traditional brokerage structures now

- Diversify income away from single-transaction commissions before the margin compression hits your market

If You're an Investor

Sectors to watch:

- Overweight: AI transaction platforms with demonstrated close rates — Opendoor's AI stack, Figure AI, next-gen MLS disruptors

- Overweight: AI mortgage and title processing infrastructure — document automation, verification AI, closing workflow platforms

- Underweight: Traditional brokerage stocks — Anywhere Real Estate, RE/MAX, Douglas Elliman — commission models face structural headwinds with no clear defense

- Avoid: Title insurance incumbents relying on transaction volume — Fidelity National, First American — fee-per-transaction models compress as AI reduces touch points

- Contrarian opportunity: Distressed commercial real estate in markets where AI is reducing office demand — the dislocation creates entry points for converted-use plays

Portfolio positioning:

- AI real estate platforms are currently priced as PropTech, not as financial infrastructure. Reclassification will drive multiple expansion.

- The short side on traditional brokerages is cleaner than it looks — NAR membership fees subsidize the illusion of a larger active agent base than transaction data supports

If You're a Policy Maker

Why traditional tools won't work:

Consumer protection frameworks built around human intermediary licensing don't map cleanly to AI agent oversight. The current regulatory structure assumes that the agent has a fiduciary relationship with a client. When the agent is an AI platform, fiduciary duty attaches to the platform's incentive structure — and AI platforms that earn flat fees have structurally better alignment with buyer/seller interests than commission agents who earn more when prices go higher.

What would actually work:

- AI transaction platform disclosure requirements — mandatory consumer notice when no licensed agent is representing them, with clear explanation of platform's fee model and data usage

- Algorithmic audit requirements for mortgage AI — regular third-party fairness testing for discriminatory lending patterns, which AI models can perpetuate from historical training data

- Transition support for displaced real estate workers — the 600,000 to 1.5 million workers who will exit the industry over 2026-2029 are disproportionately independent contractors with no unemployment insurance eligibility; reclassification and support infrastructure must be built before the displacement accelerates, not after

Window of opportunity: Q3 2026. After that, market share concentration makes structural remedies politically infeasible.

The Question Everyone Should Be Asking

The real question isn't whether AI will replace real estate agents.

It's whether we want a real estate market where the only entities that can afford to transact at scale are AI platforms — and what that concentration of housing market data and deal flow in three to five private platforms means for housing access, pricing transparency, and the families for whom a home purchase is the largest financial decision of their lives.

Because if the current trajectory holds, by Q4 2028 the top five AI real estate platforms will process more than 60% of U.S. residential transactions. They will hold more granular pricing data, buyer behavior data, and neighborhood trend data than any public institution. They will have structural power over housing market liquidity that no private entity has ever held before.

The stockbroker analogy is instructive but incomplete. When Schwab and E*Trade displaced the retail broker, the assets remained distributed across millions of investor accounts. When AI agents displace real estate professionals, the transaction data — and the market intelligence it generates — concentrates in the platforms.

The data says we have 18 months to ask the harder question before the answer gets made for us.

What's your scenario probability? Share your take in the comments — especially if you're currently in the industry and seeing these dynamics on the ground.

Disclosure: Scenario probability estimates are based on current deployment data, regulatory environment, and historical technology adoption curves. These are analytical projections, not investment advice. Data sourced from NAR, BLS, Federal Reserve HMDA disclosures, MIT Center for Real Estate, and proprietary transaction platform reporting. Last updated February 25, 2026 — will revise as Q1 2026 transaction data becomes available.